Published: June 3, 2026 · Updated: June 3, 2026 · By: Alex Rodino, U.S. Army veteran (Captain) & licensed Georgia REALTOR® (GREC #443565)

VA Second-Tier Entitlement, Explained: How Military Buyers in Coastal Georgia Use VA Twice

Your VA entitlement isn’t a one-shot. If your first VA loan didn’t use the full guaranty cap for your county, the remainder, your second-tier entitlement, can finance another VA purchase. That is the key idea most PCS buyers miss. A service member may be able to keep a first VA-financed home, rent it out, and use VA financing again for a new primary residence near Hunter Army Airfield, Fort Stewart, Richmond Hill, Pooler, Savannah, or another Coastal Georgia market. The math depends on the county loan limit, the entitlement already charged to the first VA loan, and the new loan amount. The strategy is powerful, but it still has rules: the second home must be your new primary residence, lender overlays matter, and funding-fee rules still apply.

A common Fort Stewart scenario looks like this: a Sergeant bought a Pooler home with a VA loan, then received PCS orders and wants to keep that home as a rental instead of selling into a tight timeline. The question is simple: can they buy again with VA?

Often, yes. The answer is not automatic, and it is not a loophole. It is the way VA entitlement works when part of your benefit is still available.

Key takeaways

- Your VA entitlement is reusable: if your first VA loan did not use the full county guaranty, the remainder is your second-tier (bonus) entitlement.

- You can often keep your first VA-financed home as a rental and buy again with VA, as long as the new home becomes your primary residence (generally within 60 days of closing).

- Using the 2026 baseline limit of $832,750, a buyer who used $81,250 of entitlement on a Pooler home has about $126,937.50 left, supporting roughly a $507,750 second purchase with $0 down.

- Second-tier entitlement does not cover vacation or investment-only homes, does not waive occupancy rules, and does not eliminate the VA funding fee for non-exempt buyers.

- Start with an updated COE, have a VA-friendly lender run the second-tier math, then build your PCS timeline around keeping or selling the first home.

In this guide

- What VA entitlement actually is

- When second-tier entitlement comes into play

- The math: a Coastal Georgia worked example

- What second-tier does NOT do

- Practical steps for Coastal GA military buyers

- Frequently asked questions

What VA entitlement actually is (in plain English)

In brief: VA entitlement is the amount of guaranty VA provides to the lender, not the amount you can borrow. Second-tier entitlement is the remaining guaranty available after a prior VA loan has already used part of it.

VA entitlement is the federal guaranty behind a VA-backed home loan. It protects the lender if the borrower defaults, which is one reason VA loans can often be made with no down payment. VA.gov explains that the Certificate of Eligibility, or COE, shows the amount of entitlement available for the loan guaranty. (Veterans Affairs)

Basic entitlement is commonly listed as $36,000 on a COE. That number is legacy language for loans of $144,000 or less; for larger loans, VA says it generally guarantees up to 25 percent of the loan amount when entitlement is available. (Veterans Affairs)

Basic vs. bonus (second-tier) entitlement

Second-tier entitlement, also called bonus entitlement or tier 2 entitlement, is the entitlement that remains after a first VA loan has charged part of the guaranty. VA states that if you do not have full entitlement, your remaining bonus entitlement is based on the county loan limit where you plan to buy, minus the entitlement you already used. (Veterans Affairs)

Think of it like this:

| Term | Plain-English meaning | Why it matters |

| Basic entitlement | The legacy first-tier amount often shown as $36,000 | It does not tell the whole story on modern home prices |

| Bonus or second-tier entitlement | Extra guaranty tied to the county conforming loan limit | This is what can let you use VA again |

| Entitlement charged | The amount already used by a prior VA loan | This reduces what remains for the next VA purchase |

| Remaining entitlement | The guaranty still available after prior use | This drives whether the next VA loan can be $0 down |

Alex’s note: As a veteran who has watched this come up across orders, the confusion usually starts because buyers think VA is either used or unused. In reality, the better question is: how much entitlement is still available?

When second-tier entitlement comes into play

In brief: VA second tier entitlement matters when you have already used VA, but you want to buy another primary residence before selling or restoring entitlement from the first home.

VA also states that you do not have to be a first-time buyer to use the VA home loan benefit, and there is no limit to the number of times you can use the benefit. For buyers with an active VA loan, the question becomes remaining entitlement and lender qualification. (benefits.va.gov)

PCS scenarios (keep the first home as a rental)

This is the big Coastal Georgia use case. A buyer may leave Fort Stewart, Hunter AAF, or Savannah on orders and decide not to sell the first home. Maybe the mortgage payment is manageable. Maybe the home has a strong rental outlook. Maybe selling on short PCS timing would force a discount.

The first home can often be retained and rented out, subject to lender rules, but the new VA-financed home must be the buyer’s new primary residence. VA guidance requires the borrower to make the home their residence when using remaining entitlement, and VA occupancy training materials say occupancy is generally within 60 days of closing, with certain military-related exceptions. (benefits.va.gov)

Buying up in price after the first VA loan

Second-tier entitlement also comes up when the first VA purchase was smaller than the next one. A service member may have bought a starter home near Pooler, Hinesville, or Georgetown, then later need more space in Richmond Hill, Savannah, or Bryan County.

That does not automatically kill VA financing. It just means the lender has to calculate whether the remaining guaranty plus any down payment equals the guaranty coverage they require. If your first purchase was a smaller starter home, our guide to the real cost of buying your first home in Savannah walks through the budgeting side before you trade up.

After a prior VA short sale or foreclosure

This is where we slow down. VA second tier entitlement may still exist after a prior loss, but the math, waiting period, credit profile, restoration status, and lender overlays become case-specific. We do not treat foreclosure or short-sale scenarios like a quick calculator problem.

If this is your situation, start with an updated COE and a VA-friendly lender before you make offers. Then coordinate the real estate side around what the lender can actually approve.

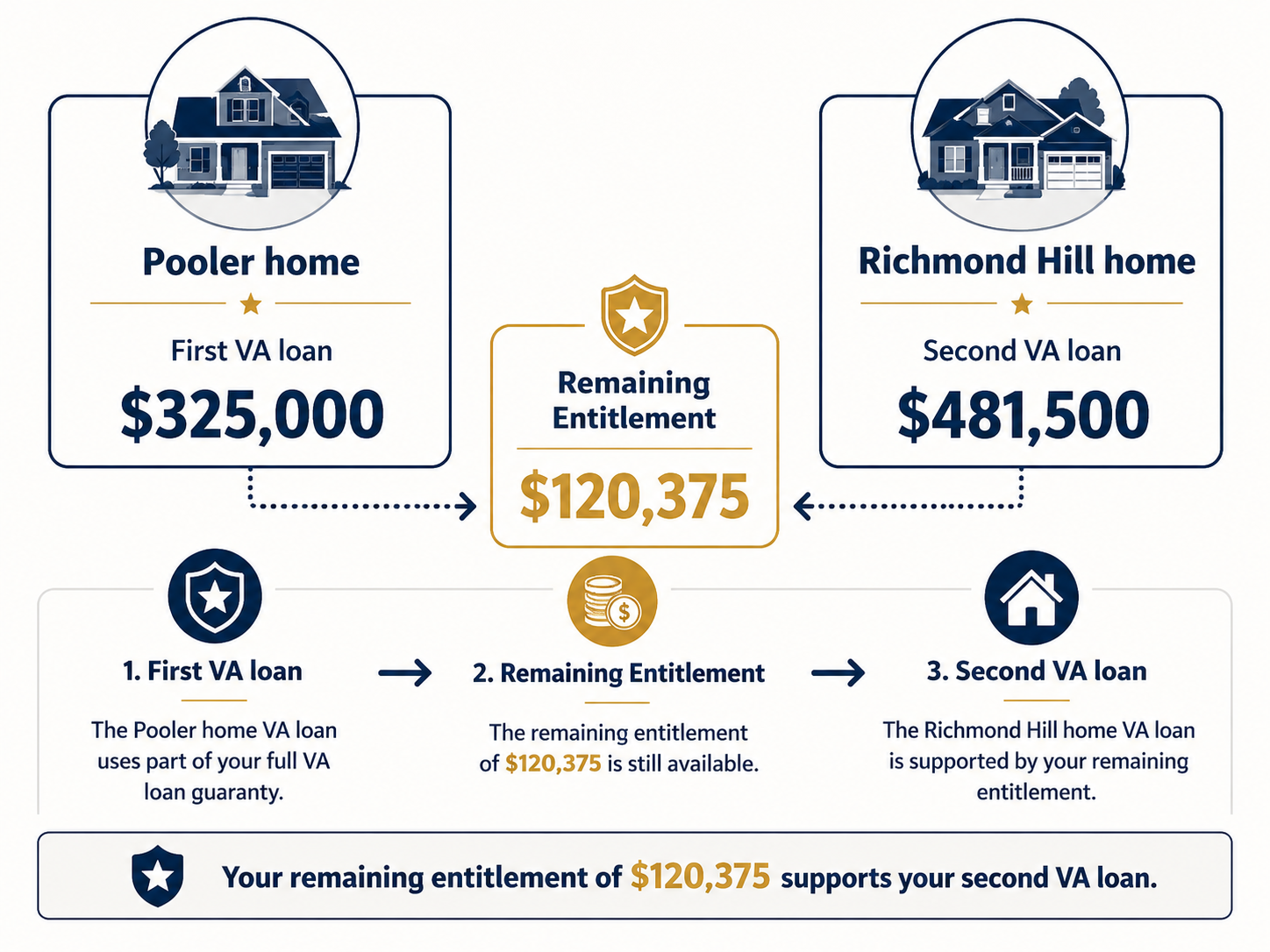

The math: a Coastal Georgia worked example (Pooler to Richmond Hill)

In brief: Using the official 2026 baseline conforming loan limit of $832,750, 25 percent total guaranty is $208,187.50 before prior entitlement is subtracted.

For 2026, FHFA announced a baseline one-unit conforming loan limit of $832,750 in most of the United States. VA says its home loan limits are the same as FHFA conforming loan limits, and VA tells buyers to use the one-unit limit when calculating remaining bonus entitlement. (FHFA.gov)

Here is the worked example using updated 2026 math:

| Step | Calculation | Result |

| 2026 baseline one-unit limit | Official FHFA baseline | $832,750 |

| Maximum VA guaranty at 25 percent | $832,750 x 25 percent | $208,187.50 |

| First VA loan on Pooler home | $325,000 x 25 percent | $81,250 used |

| Remaining second-tier entitlement | $208,187.50 minus $81,250 | $126,937.50 |

| Estimated $0 down second VA capacity | $126,937.50 x 4 | About $507,750 |

In this example, the buyer’s first VA loan on a Pooler home charged $81,250 of entitlement. After subtracting that from the 2026 guaranty cap, the buyer has about $126,937.50 of second-tier entitlement left. Since most lenders want entitlement, down payment, or both to cover at least 25 percent of the new loan amount, that remaining entitlement can support a second VA purchase around $507,750 with $0 down, assuming the borrower qualifies. VA.gov explains that a lender may require a down payment if the borrower does not have enough remaining bonus entitlement to cover the 25 percent guaranty standard. (Veterans Affairs)

If the Richmond Hill purchase goes above that rough $507,750 support point, a down payment may be required to cover the gap. That does not mean VA is unavailable. It means the file has moved from “enough remaining entitlement for $0 down” to “partial entitlement plus down payment.”

2026 VA loan limits for Coastal Georgia counties

Because VA uses the FHFA conforming loan limits, the counties around Fort Stewart, Hunter Army Airfield, and Savannah all follow the 2026 baseline one-unit limit. None of these are designated high-cost areas, so the same figure applies when you calculate remaining second-tier entitlement:

| County | Markets it covers | 2026 one-unit VA loan limit |

|---|---|---|

| Chatham | Savannah, Pooler, Hunter AAF | $832,750 |

| Bryan | Richmond Hill, Pembroke | $832,750 |

| Liberty | Hinesville, Fort Stewart | $832,750 |

| Effingham | Rincon, Springfield | $832,750 |

Always confirm the current figure for your specific county and loan with your VA-approved lender before writing an offer.

What second-tier does NOT do

In brief: Second-tier entitlement does not turn VA into an investment-property loan, remove occupancy rules, or erase funding-fee rules for non-exempt buyers.

Second-tier is useful, but it is not a workaround for every situation.

It does not let you use VA on a vacation home or pure investment property. VA home loan benefits are for homes used as the borrower’s residence. If you are buying only to rent the property from day one, that is not the same as buying your next primary residence and retaining the prior home.

It does not avoid occupancy rules. The new home needs to be your primary residence, generally within the VA occupancy timeline or an approved exception. This matters for active-duty buyers whose orders, deployment, training pipeline, or family movement affect timing.

It does not eliminate the VA funding fee for non-exempt buyers. VA says the funding fee is generally required unless the borrower qualifies for an exemption, such as receiving VA compensation for a service-connected disability. VA’s purchase funding-fee chart also separates first use from later use, with after-first-use rates depending on down payment. (Veterans Affairs)

It does not replace lender underwriting. Debt-to-income ratio, residual income, rental-income treatment, lease documentation, reserves, credit, appraisal, and property eligibility can all affect the approval.

Practical steps for Coastal GA military buyers

In brief: Start with the COE, run the second-tier math with a VA-friendly lender, then coordinate the real estate plan around PCS timing and the first home’s sale or rental strategy.

Start by requesting or updating your Certificate of Eligibility. VA.gov says the COE shows your lender that you qualify based on service history and duty status, and VA’s entitlement page explains that prior loans charged to entitlement are shown on the COE. (Veterans Affairs)

How to read your COE: Look for the entitlement code and the “Entitlement charged to previous VA loans” line. If a prior loan charged part of your guaranty, that amount is subtracted from your county limit to find what remains. A $0 charged line generally means full entitlement; a positive number points you to the second-tier math above.

Then, get a lender to calculate the second-tier capacity before you shop aggressively. We want the lender to answer four questions:

- How much entitlement is currently charged to the first VA loan?

- What county loan limit applies to the new property?

- What second purchase price can be supported with $0 down?

- If the price is higher, how much down payment is needed?

Next, coordinate the first home. If you are keeping it, the lender may ask for a lease, rental-income documentation, reserve funds, or proof that the departing residence is manageable. If you are selling, build the timing around orders, repairs, showings, appraisal risk, and closing dates. Our guide to selling on PCS orders can help you think through that side of the move.

This is also where local representation matters. National PCS-realtor aggregators and generic military-buyer sites can explain the broad VA concept, but they usually do not know the difference between a Pooler rental strategy, a Richmond Hill commute, a Hinesville timeline, and a Savannah-area PCS closing window. ARC’s advantage is veteran-led, Coastal Georgia-specific execution.

For broader local context, read the full Hunter AAF and Fort Stewart buyer’s guide. If you are also trying to reduce cash to close, pair this article with our guide to negotiating VA loan seller concessions.

For one-on-one planning, start with Coastal Georgia military relocation help.

Not sure how to structure your VA offer in the Savannah market?

We’ll map your concessions, closing costs, and PCS timeline before you write the offer.

Frequently asked questions

In brief: The most common second-tier questions come down to whether you can keep the first home, whether the next loan needs a down payment, and whether the new home must be your primary residence.

Ready to use VA again in Coastal Georgia?

About the author

Alex Rodino is a U.S. Army veteran (Captain) and a licensed Georgia REALTOR® (GREC #443565) with Keller Williams, leading the Alexander Rodino Collective (ARC) in Coastal Georgia. He works hands-on with military buyers and sellers navigating PCS moves and VA loan strategy near Fort Stewart, Hunter Army Airfield, and Savannah. The figures in this guide are drawn from official 2026 VA and FHFA sources; entitlement, funding-fee, and occupancy details should always be confirmed with a VA-approved lender.

In brief: If you are trying to keep one VA-financed home and buy another, the right sequence is entitlement math first, then property strategy.

A second VA purchase can be one of the best tools a military buyer has, especially during a PCS. It can also go sideways if the lender, agent, and timing plan are not aligned from the start.

ARC helps military buyers map the entitlement math, the local commute reality, the rental-or-sale decision, and the contract strategy before the offer is written. Schedule a free 30-minute call through Coastal Georgia military relocation help and we will help you understand the next move before you are under pressure.

Final disclosure: Alex Rodino is a U.S. Army veteran (Captain) and licensed Georgia REALTOR® (GREC #443565). The ARC Platform is affiliated with Keller Williams. This article is for informational purposes only and is not mortgage, legal, tax, or financial advice. VA loan approval, entitlement calculations, funding fees, occupancy exceptions, and rental-income treatment must be confirmed with a qualified VA lender. Equal Housing Opportunity.

Talk to a Veteran-Led VA Buyer’s Agent →

Free strategy call • No pressure • We work around your PCS orders

Join The Discussion