Published: June 2, 2026 · Updated: June 3, 2026 · By: Alex Rodino, US Military Veteran & licensed Georgia REALTOR® (GREC #443565)

In brief: On a VA loan, seller concessions are capped at 4% of the home’s VA reasonable value, while customary closing costs like origination, appraisal, title, and recording fees have no VA dollar cap. In Coastal Georgia, treating these as two separate buckets lets military buyers maximize seller-paid help without breaking VA rules.

You are on PCS orders. Your report date is getting closer. You are comparing homes near Hunter Army Airfield, Fort Stewart, Richmond Hill, Pooler, Hinesville, and the greater Savannah area, and one practical question keeps coming up: how much can the seller actually pay for you on a VA loan?

That is where VA loan seller concessions get misunderstood. Many military buyers hear “4% limit” and assume the seller can only pay 4% total toward their closing costs. That is not how the VA rule works.

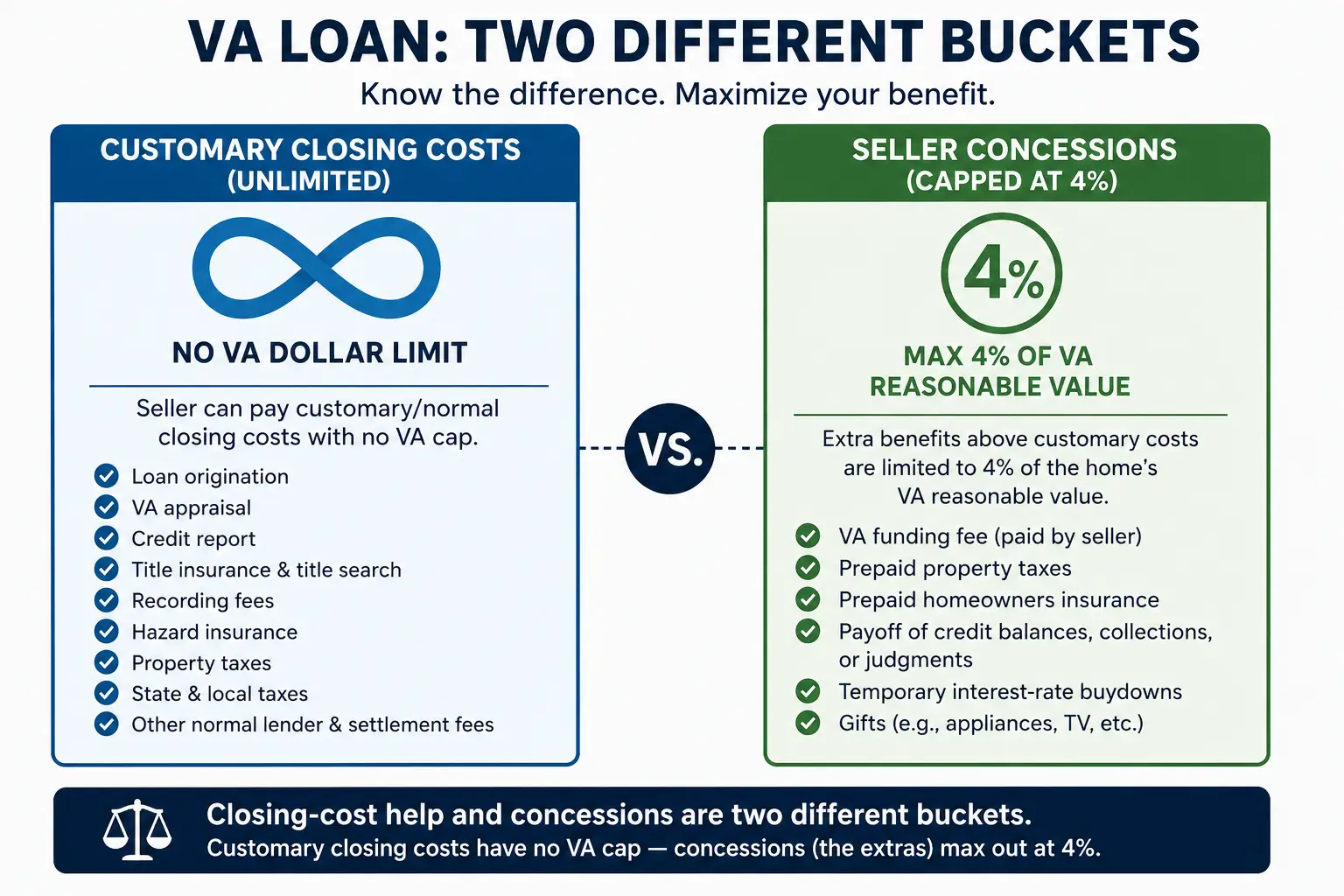

Closing-cost help and concessions are two different buckets. Customary closing costs have no VA cap. Concessions (the extras) max out at 4%.

At ARC, we help military buyers separate those two buckets before they write the offer. That matters because the right structure can reduce your cash due at closing, protect your PCS timeline, and keep your offer competitive in the Coastal Georgia market.

Quick answer: On a VA loan, seller concessions are capped at 4% of the home’s VA reasonable value, while customary closing costs (origination, appraisal, title, recording fees) have no VA dollar cap and are negotiated separately. Treating these as two distinct “buckets” lets military buyers in Coastal Georgia maximize seller-paid help without breaking VA rules.

On this page

- What “seller concessions” actually mean on a VA loan

- What the 4% concession cap covers

- Closing costs a seller can pay with no limit

- A real Coastal Georgia example: $350K worked numbers

- How to negotiate concessions in the Savannah / Hunter AAF / Fort Stewart market

- Frequently asked questions

- Planning a VA purchase in Coastal Georgia?

What “seller concessions” actually mean on a VA loan

On a VA loan, the seller can help a buyer in two broad ways. First, the seller can pay normal, customary closing costs. Second, the seller can offer additional benefits that VA treats as concessions.

The official VA rule is that seller concessions are limited to 4% of the home’s reasonable value. VA also states that seller or builder credits for closing costs are not limited the same way, which is the key distinction most buyers miss. (Veterans Affairs)

The home’s reasonable value is generally tied to the VA appraisal and Notice of Value. That means the concession limit is not just a random number in the contract. It is connected to the value VA uses for the loan.

Concessions vs. customary closing costs: the 4% cap only touches concessions

Think of the rule as two separate buckets:

| Category | What it means | VA cap? |

| Customary closing costs | Normal transaction costs such as origination, VA appraisal, title insurance, recording fees, hazard insurance, real estate taxes, and similar settlement charges | No VA dollar cap |

| Seller concessions | Extra value beyond normal closing costs, such as funding fee payment, prepaids, debt payoff, temporary buydowns, or gifts | Capped at 4% of reasonable value |

This distinction is where military buyers can gain real negotiating power. A seller might agree to pay a meaningful portion of your customary closing costs and still have room to offer concessions, as long as the concession bucket stays within the VA limit.

As a veteran who’s negotiated these on both sides of the closing table, Alex has seen how often buyers leave money unasked for because they think the 4% cap is stricter than it really is.

What the 4% concession cap covers

In brief: The 4% cap applies only to concessions, the extras beyond normal closing costs, such as the VA funding fee, prepaid taxes and insurance, debt payoff, temporary buydowns, and gifts.

The 4% concession cap covers items that give the buyer additional value beyond ordinary closing-cost help. These concessions can be especially useful for active-duty families trying to preserve cash before a move, shipment delay, lease overlap, temporary lodging expense, or household setup in a new duty station.

VA guidance identifies concession examples such as payment of the Veteran buyer’s funding fee, prepaids for real estate taxes and hazard insurance, gifts, temporary buydown points, and payoff of credit balances or judgments. (Home Loans)

VA funding fee

The VA funding fee is one of the most common concession items. A seller can pay it for the buyer, but because the funding fee is considered a concession, it counts toward the 4% cap.

For 2026 VA purchase loans, the funding fee schedule is:

| VA loan use | Less than 5% down | 5% or more down | 10% or more down |

| First use | 2.15% | 1.5% | 1.25% |

| After first use | 3.3% | 1.5% | 1.25% |

These VA funding fee rates are published by VA.gov and remain tied to loan type, prior use, and down payment amount. (Veterans Affairs)

Many disabled veterans are exempt from the VA funding fee. VA states that Veterans receiving VA compensation for a service-connected disability, certain Veterans who would be entitled to receive that compensation, and qualifying surviving spouses do not have to pay the fee. (Benefits)

That exemption matters during negotiation. If you are exempt, the concession room that might have gone toward the funding fee can potentially be used for other buyer benefits instead.

Prepaid taxes and insurance, debt payoff, buydowns, and gifts

Other common seller concessions include:

- Prepaid property taxes and homeowners insurance: These can reduce the cash a buyer needs to bring to closing.

- Debt payoff: In some cases, concessions can be used to pay off buyer credit balances, collections, or judgments.

- Temporary interest-rate buydowns: VA states that temporary buydowns can be funded by the seller, lender, builder, or Veteran, and seller-funded temporary buydowns are treated as concessions capped at 4% of reasonable value. (Benefits)

- Gifts or personal property: Appliances or other items included at no additional cost may be treated as concessions.

The best use depends on the buyer’s main objective. A PCS buyer who is tight on cash may care most about reducing out-of-pocket funds at closing. A buyer focused on monthly budget may prefer a rate buydown. A buyer using the VA benefit for the first time may want the funding fee covered.

Closing costs a seller can pay with NO limit

In brief: Customary closing costs like origination, appraisal, title, and recording fees have no VA dollar cap and are negotiated separately from the 4% concession bucket.

This is the part that deserves emphasis: customary seller-paid closing costs have no VA dollar limit.

That does not mean every seller will agree to pay everything. It means VA does not impose the same 4% cap on normal closing-cost credits. These costs are negotiated in the purchase contract and reviewed through the lender and closing process.

Customary closing costs may include:

- Loan origination charges

- VA appraisal fee

- Credit report fee

- Title search and title insurance charges

- Recording fees

- State and local taxes tied to the transaction

- Hazard insurance charges

- Real estate taxes due at closing

- Normal lender, title, and settlement fees

VA.gov lists several negotiable closing-cost categories, including loan origination, discount points or temporary buydown funds, credit report, credit balances or judgments, VA appraisal fee, hazard insurance, real estate taxes, state and local taxes, title insurance, and recording fees. (Veterans Affairs)

This is why an offer can be structured more intelligently than simply asking for “4% seller help.” A stronger approach may be to ask the seller to pay customary closing costs separately, then use the concession bucket for items that produce the most benefit.

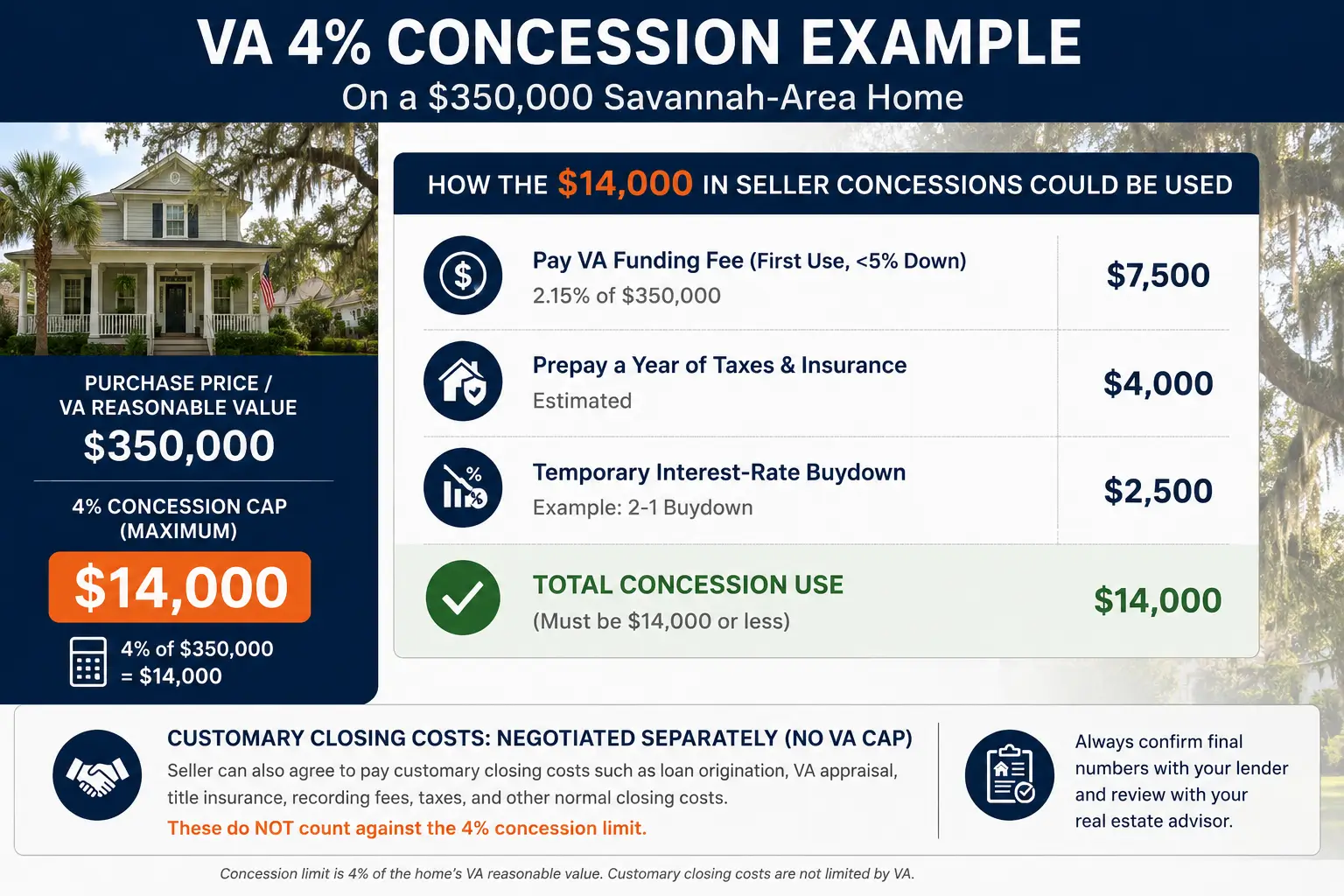

A real Coastal Georgia example: $350K worked numbers

Let’s say a military buyer is purchasing a $350,000 home in Coastal Georgia with a VA loan.

The 4% concession cap is calculated like this:

| Item | Amount |

| Purchase price / VA reasonable value | $350,000 |

| 4% concession cap | $14,000 |

That gives the buyer up to $14,000 in concession room, separate from customary closing-cost help.

A sample concession allocation could look like this:

| Concession item | Estimated amount | Counts toward 4% cap? |

| Seller pays first-use VA funding fee at 2.15% | About $7,500 | Yes |

| Seller prepays a year of taxes and insurance | Example: $3,500 to $4,500 | Yes |

| Seller contributes to a small temporary rate buydown | Example: $2,000 to $3,000 | Yes |

| Total concession use | Up to $14,000 | Yes |

Now here is the important part. The buyer could still negotiate separately for the seller to pay customary closing costs, such as title fees, recording fees, loan origination, the VA appraisal, and other normal settlement costs. Those customary closing costs do not eat into the $14,000 concession room.

That is the practical value of understanding the two-bucket rule before you submit an offer.

How to negotiate concessions in the Savannah / Hunter AAF / Fort Stewart market

Concessions are not just a loan-rule issue. They are a market strategy issue.

In the Savannah, Hunter Army Airfield, Fort Stewart, Richmond Hill, Pooler, and Hinesville corridor, leverage depends on the listing, the seller’s motivation, property condition, days on market, competing offers, and your closing timeline. A move-in-ready home in a high-demand pocket may require a cleaner offer. A home that has been sitting, needs repairs, or has a seller with a deadline may create room for seller-paid costs and concessions.

This is where local guidance matters. Through our military relocation services in Savannah, we help VA buyers decide whether to ask for closing-cost help, concessions, a price adjustment, repair credits, or a combination that fits the property and the market.

Not sure how to structure your VA offer in the Savannah market?

We’ll map your concessions, closing costs, and PCS timeline before you write the offer.

Get My VA Offer Strategy →If you are still comparing locations, our guide to buying a home near Fort Stewart or Hunter Army Airfield can help you understand how commute, lifestyle, base access, and neighborhood selection affect the search.

When to ask for concessions vs. a price cut vs. a rate buydown

A seller concession is not always better than a price cut. A price cut is not always better than a concession. The right request depends on your objective.

Ask for customary closing-cost help when your main goal is reducing cash due at closing and the seller may resist extras.

Ask for concessions when you want help with the VA funding fee, prepaid taxes and insurance, a temporary buydown, or other extra costs.

Ask for a price reduction when the home is overpriced, condition issues are obvious, or appraisal risk is a concern.

Ask for a rate buydown when monthly payment relief matters more than reducing the purchase price slightly.

For many PCS buyers, cash flow is the deciding factor. You may be paying for temporary lodging, storage, a lease break, utility deposits, travel, or overlapping housing expenses. In that situation, a seller credit that lowers cash to close may be more valuable than a small price reduction spread over 30 years.

PCS-timeline tactics: you may be negotiating remotely on orders

PCS buyers often negotiate under pressure. You may be touring homes by video, signing documents from another state, coordinating leave, or trying to close before household goods arrive.

That changes the strategy. We usually want to clarify the concession plan early, before emotions and deadlines tighten. A clean offer should spell out what the seller is being asked to pay and why the structure works under VA rules.

Practical PCS tactics include:

- Get lender numbers before writing. Do not guess at closing costs, funding fee status, or cash-to-close needs.

- Separate customary costs from concessions in the offer strategy. This prevents confusion over the 4% cap.

- Use seller motivation. A vacant home, relocation sale, stale listing, or inspection issue may create room for credits.

- Protect the timeline. Avoid asking for concessions in a way that creates underwriting confusion late in the process.

- Think beyond the contract price. The best offer is the one that gets you into the right home with the right cash position and the least avoidable risk.

If you are also dealing with a home sale at your current duty station or here in Coastal Georgia, our guide to selling your current home on PCS orders can help you think through timing, listing prep, and transition risk.

Frequently asked questions

Planning a VA purchase in Coastal Georgia?

VA loan rules are powerful when they are used correctly. The mistake is treating every seller credit the same. Customary closing costs and concessions are different tools, and a well-structured offer can use both without violating VA limits.

At ARC, we help military buyers negotiate clearly, protect their PCS timeline, and make confident decisions near Savannah, Hunter Army Airfield, Fort Stewart, Richmond Hill, Pooler, Hinesville, and surrounding Coastal Georgia communities.

Whether you are house-hunting, weighing an offer, or coordinating a sale at your current duty station, we help you structure a VA offer that protects your cash and your timeline. Start with our military relocation services in Savannah.

Talk to a Veteran-Led VA Buyer’s Agent →

Free strategy call • No pressure • We work around your PCS orders

Join The Discussion