TLDR: VA MPRs trip up Coastal Georgia closings every week: termite, moisture, roof, HVAC, septic. VA Minimum Property Requirements are not the same thing as a private home inspection. They are VA-specific livability minimums that focus on safety, sanitation, structural integrity, and basic occupancy. In Coastal Georgia, the same issues show up again and again because of humidity, older wood-frame homes, crawlspaces, flood-zone exposure, and rural properties with private well or septic systems. The goal is not to panic when the VA appraisal flags something. The goal is to know what must be fixed before closing, what can be negotiated, and what documentation keeps the VA loan moving.

A common Coastal Georgia scenario looks like this: a VA buyer is under contract on a 1972 ranch in Garden City. The private inspection already happened. Everyone thinks the hard part is over.

Then the VA appraisal comes back with three MPR call-outs: WDO documentation, crawlspace moisture, and roof condition. The buyer is asking whether the loan is still safe. The seller is asking who has to pay. The lender is waiting on documentation.

That is where local experience matters. If you are PCSing to Hunter Army Airfield or Fort Stewart, start with the Hunter AAF and Fort Stewart military buyer’s guide so the VA loan, commute, neighborhood, and property-condition pieces fit together.

Key Takeaways

- MPRs are not a home inspection. They are the VA’s livability minimums (safety, sanitation, structure, basic systems), confirmed at the VA appraisal.

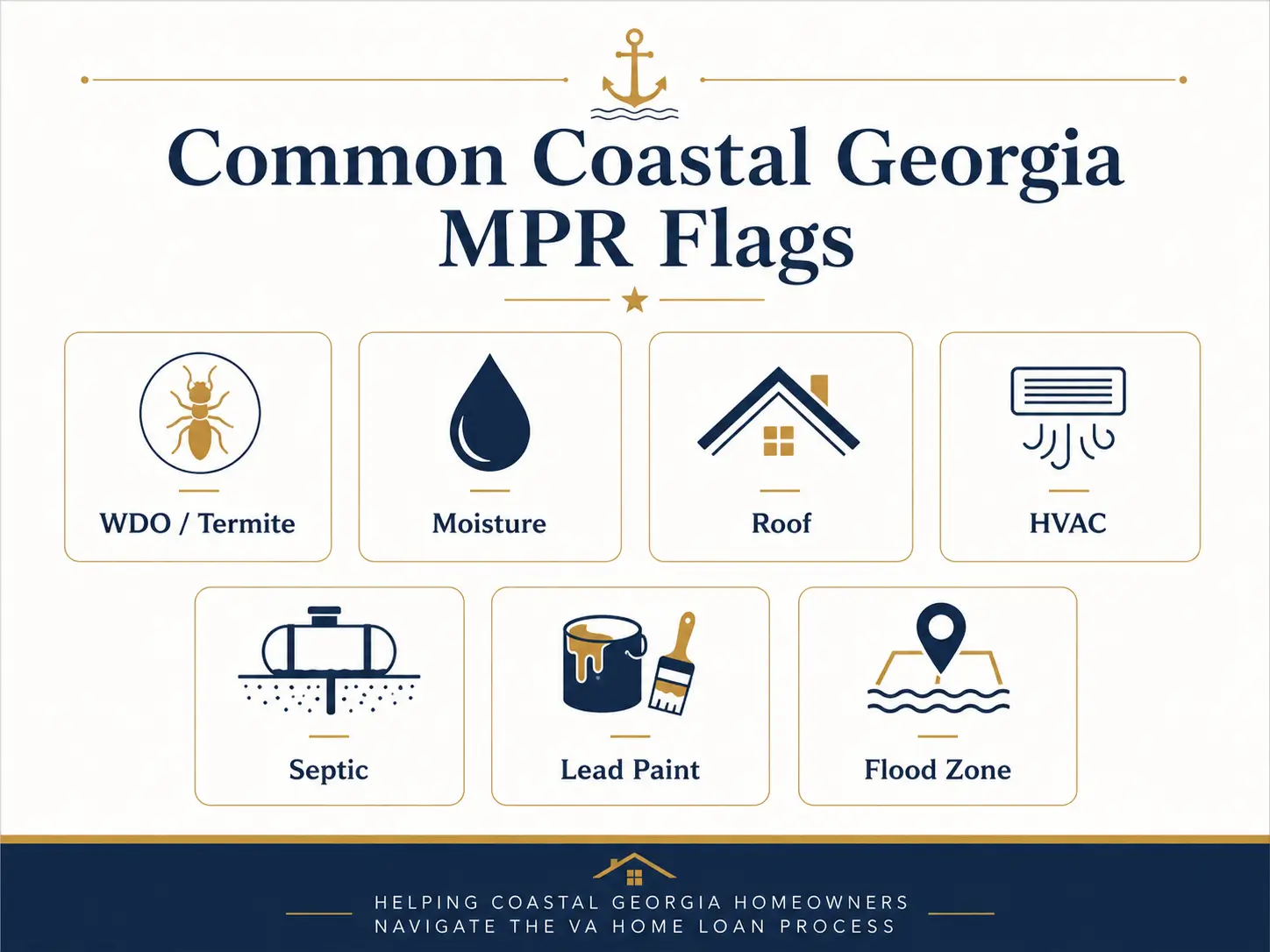

- Coastal Georgia has a predictable pattern of flags: WDO/termite, moisture, roof, HVAC, well/septic, lead paint, and flood zone.

- Georgia is a mandatory-WDO state, so every VA purchase needs a wood-destroying organism inspection.

- Who pays is negotiable, but safety, sanitation, WDO, water, and sewer issues usually must be cleared before closing.

- Plan ahead: sellers should fix obvious triggers before listing; buyers should ask MPR questions before writing the offer.

On This Page

What VA MPRs are (and what they aren’t)

VA minimum property requirements are the Department of Veterans Affairs’ baseline property standards for homes financed with a VA-guaranteed or direct loan. The Federal Register’s VA MPR topic list identifies Chapter 12 topics such as utilities, water supply, sewage disposal, roof covering, crawl spaces, lead-based paint, special flood hazard area, manufactured homes, and wood-destroying insects, fungus, or dry rot. (Federal Register)

MPRs are reviewed through the VA appraisal process. They are not designed to identify every maintenance item a buyer may care about after closing. A home can pass a private inspection and still fail MPRs, and a home can have a long inspection report without creating a VA loan condition.

MPRs vs. inspection findings

An inspector tells you what’s broken. The VA appraiser tells you what falls below VA’s livability minimum: different lists, different consequences.

That distinction matters in negotiation. The private inspection is usually a buyer-protection and negotiation tool. The VA MPR issue is usually a loan-condition problem that must be resolved, documented, or formally accepted where the VA process allows.

Alex’s note: As a veteran who has negotiated VA deals from both sides of the closing table, we try to separate scary from solvable. A flagged item is not always a dead deal. It is usually a timing, documentation, and negotiation problem.

The Coastal Georgia MPR shortlist: what we see flagged most

The VA appraiser confirms MPR scope around safety hazards, sanitation, structural integrity, basic mechanical systems such as heat, plumbing, and electrical, wood-destroying organism inspection in designated regions, water and sewage adequacy, and roof condition. VA’s current public MPR reference point remains the VA Lender’s Handbook, with Chapter 12 addressing minimum property requirements.

MPR issue | Why it shows up in Coastal Georgia | What usually helps |

WDO / termite | Georgia is a mandatory-WDO state for VA loans | Order early, clear active findings, document treatment |

Moisture intrusion | Crawlspaces, humidity, eaves, drainage, older envelopes | Fix leaks, ventilation, drainage, and damaged wood |

Roof remaining life | Older roofs, staining, missing shingles, soft decking | Roofer letter, repair invoice, or replacement if needed |

HVAC + water heater | Basic systems must be safe and functional | Turn utilities on, service systems, document repairs |

Well + septic | Common in unincorporated Bryan, Effingham, and Liberty parcels | Water test, septic records, local compliance |

Lead-based paint | Pre-1978 Savannah and historic-area housing stock | Stabilize peeling or chipping paint before close |

Flood-zone insurance | SFHA exposure near marsh, river, and low-lying areas | Verify map status and insurance early |

WDO / termite (Georgia is a mandatory-WDO state)

WDO/termite inspection is required in the entire state of Georgia for VA loans. Georgia is on VA’s required-WDO-state list, and VA’s local requirements page says wood-destroying insect information is required for the entire state of Georgia. (benefits.va.gov)

Form NPMA-33 is the standard Wood Destroying Insect Inspection Report sample listed by HUD, and the sample form states that it is approved for FHA and VA loans. (hud.gov)

For a VA loan termite Savannah file, order the WDO inspection early. If the report shows active insects, visible damage, inaccessible crawlspace areas, or recommended treatment, the file may need repair documentation, treatment receipts, a clearance letter, or additional review.

Georgia also has state rules around wood infestation inspection reporting. The Georgia administrative rules state that the Official Georgia Wood Infestation Inspection Report is the written instrument for certifying a structure as apparently free from wood-destroying organisms for transfer of real property, and it must be issued by a pest control operator certified in Wood Destroying Organisms. (rules.sos.ga.gov)

Moisture intrusion (crawlspace, eaves, coastal humidity)

Moisture is one of the most common VA loan moisture intrusion Coastal Georgia problems we plan around. VA is not requiring a perfect house, but excessive dampness, visible decay, active leakage, damaged subflooring, rotten eaves, and fungal-looking growth can become MPR concerns if they affect safety, sanitation, or structural integrity.

The source matters. A missing downspout, leaking supply line, poor grading, failed flashing, or unvented crawlspace are not the same repair. We do not guess repair costs in the offer. We get the right contractor or specialist to define the scope.

Roof remaining life

VA loan roof remaining life is case-by-case. VA expects the roof to provide reasonable future utility, durability, and economy of maintenance. Roof covering is one of the VA MPR topics listed in Chapter 12. (Federal Register)

In the field, lenders and appraisers often discuss whether the roof has roughly 2 to 3 years of remaining life, but that is not a hard universal rule.

The practical question is simple: does the roof keep moisture out, and does it look serviceable for reasonable future use? Missing shingles, active leaks, roof tarps, soft decking, or ceiling staining can lead to a repair condition.

HVAC + water heater function

Heating is part of the MPR review. Heating must be able to maintain at least 50°F in every living area. VA’s training page notes that its prior MPR training material was developed before Chapter 12 updates that took effect on May 1, 2026, so the current handbook should be checked at QA. (benefits.va.gov)

The practical advice is still straightforward: do not send the VA appraiser to a property with utilities off unless the lender has given a specific path. If the appraiser cannot confirm basic system function, the appraisal can come back subject to further inspection, repair, or documentation.

Private well + septic (unincorporated Bryan / Effingham / Liberty)

Water and sewage must meet VA standards: a continuous supply of safe, potable water and an acceptable means of sewage disposal. Private wells need bacterial and nitrate testing. Private septic systems must function and meet local standards.

This comes up more often in unincorporated Bryan, Effingham, and Liberty County parcels than in city-service Savannah homes. Before writing the offer, ask whether the property is on public water, public sewer, private well, private septic, or a combination.

Lead-based paint in pre-1978 Savannah historic stock

Lead-based paint is a known issue in older Savannah housing stock. Federal lead disclosure rules apply to most pre-1978 housing, and EPA states that sellers, landlords, property managers, and real estate agents are responsible for compliance with disclosure requirements before sale or lease. (US EPA)

For VA MPR purposes, the concern is not simply that the home is old. The problem is peeling, chipping, or deteriorated paint that creates a health and safety issue. Pre-1978 homes with peeling or chipping paint can be flagged, and remediation may be required before close.

Flood-zone insurance (SFHA-adjacent neighborhoods)

Flood zone is not a strict MPR issue, but VA requires flood insurance if the home is in a Special Flood Hazard Area. VA guidance reminds lenders that flood insurance, if needed, must be obtained and maintained on any building or personal property securing a VA loan. (benefits.va.gov)

That matters across Chatham coastal neighborhoods, river-adjacent parcels, and Effingham floodplain areas. For local context, read Savannah flood zones and insurance before you assume a property’s monthly payment is final.

Not sure which items are dealbreakers in your deal?

Who fixes what: the negotiation playbook

There is no universal rule that says the seller always pays or the buyer always pays. It depends on the contract, repair scope, appraisal wording, lender condition, market temperature, and negotiating power.

Items the SELLER must address (safety / sanitation / WDO)

In practice, seller-completed repairs are most common when the issue affects safety, sanitation, structural integrity, active WDO findings, potable water, sewage disposal, or a lender condition. The buyer may still want the house, but the VA file needs the issue cleared.

Items the BUYER can absorb or escrow (cosmetic, deferred maintenance)

Cosmetic and deferred-maintenance items are different. Worn finishes, dated cabinets, older but functional systems, or minor repairs may matter to the buyer without becoming a VA MPR condition. Escrow options depend on lender approval and the specific repair item.

When concession dollars work better than seller-completed repairs

Sometimes concession dollars work better than rushed seller-completed work, especially when the item is not a mandatory pre-closing MPR repair. The key is knowing which bucket you are in. Before countering, read how VA seller concessions work.

What to do BEFORE you list to a VA buyer (sellers)

If your likely buyer pool includes military families, prepare the property like a VA appraiser may see it. Order a WDO inspection, clear visible moisture issues, repair rotten trim, address peeling paint on older homes, service HVAC, check the water heater, and gather roof, septic, well, and repair documentation.

You do not need to renovate the whole house. You do need to remove the obvious reasons a VA buyer’s lender may pause the file.

Have a VA appraisal condition you’re unsure about?

What to ask BEFORE you make a VA offer (buyers)

Before making a VA offer in Coastal Georgia, ask:

- How old is the roof, and are there any known leaks?

- Is there a recent WDO report or termite bond?

- Has the crawlspace had moisture, fungus, or standing-water issues?

- How old are the HVAC system and water heater?

- Is the home on public water and sewer, private well, septic, or both?

- Was the home built before 1978, and is there peeling or chipping paint?

- Is any part of the property in a Special Flood Hazard Area?

If you are keeping another VA-financed home and buying again in Coastal Georgia, MPRs still apply to the new property. The loan math is a separate issue, so review second-tier VA entitlement as part of your PCS plan.

Join The Discussion