Published: May 28, 2026 · Updated: June 30, 2026 · By: Alex Rodino, US Military Veteran & licensed Georgia REALTOR® (GREC #443565)

At a glance

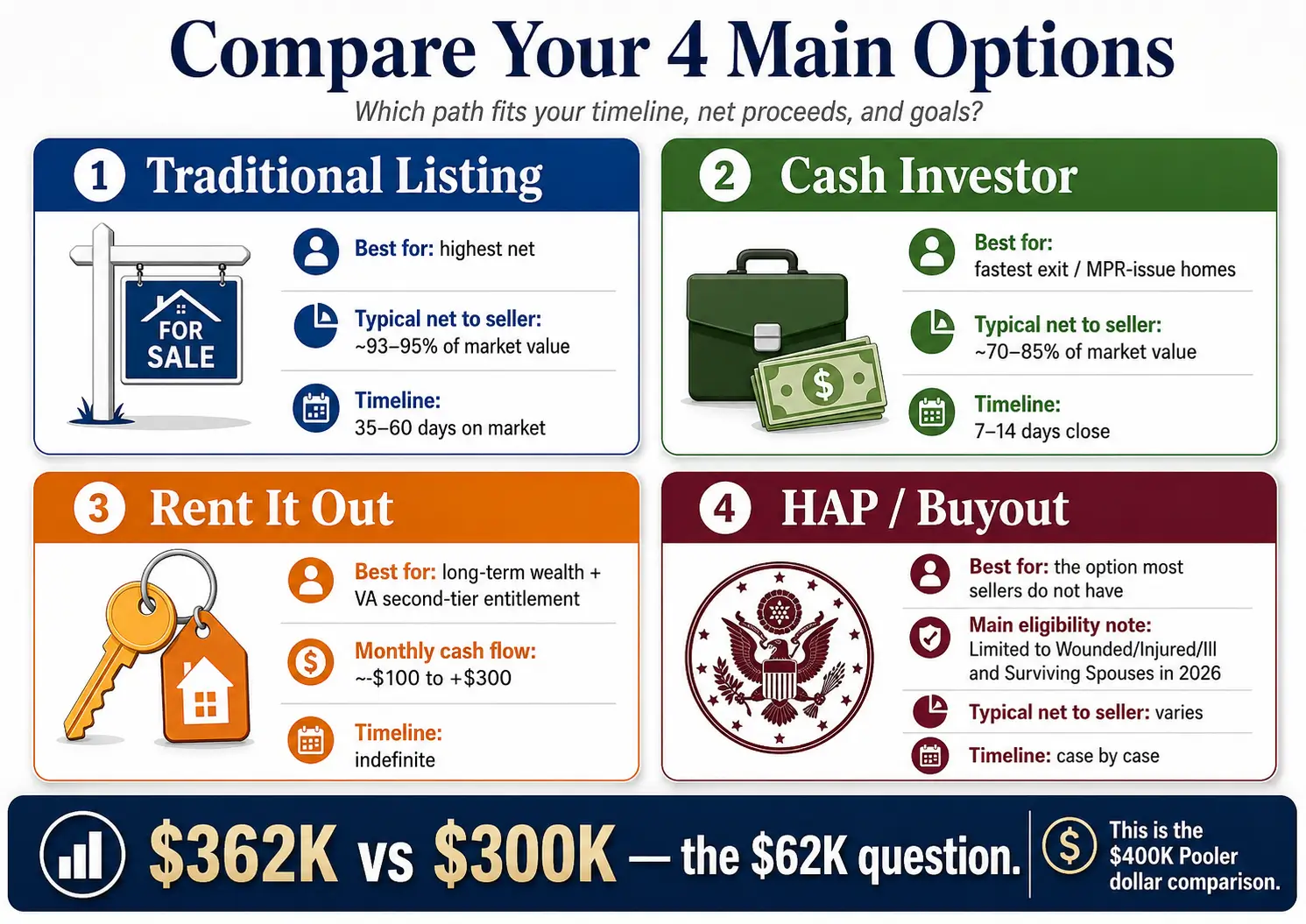

- Military families selling on PCS orders in Coastal Georgia have four real options in 2026: list traditionally, sell to a cash investor, rent the home using VA second-tier entitlement, or pursue the federal HAP buyout.

- A traditional listing nets roughly 93% to 95% of market value over 35 to 60 days, while a cash investor closes in 7 to 14 days at roughly 70% to 85% of value; on a $400,000 home that gap is about $62,000.

- The right choice depends on your report date, VA entitlement, home condition, and risk tolerance, and HAP is limited to Wounded, Injured, or Ill applicants and Surviving Spouses.

On this page

- → At a glance: the PCS seller options

- → The four options PCS sellers actually have

- → The PCS selling timeline

- → Option 1: List traditionally, the math at $400K

- → Option 2: Cash investor, when 70%–85% is the right answer

- → Option 3: Rent it out, the VA entitlement play

- → Option 4: HAP or military buyout

- → The decision framework

- → SCRA and military-specific protections

- → The Coastal Georgia market reality, 2026

- → The 30-minute call, what we cover

- → Frequently asked questions

Military families selling a home on PCS orders in Coastal Georgia have four real options in 2026: (1) list traditionally, 35 to 60 days on market, ~93–95% of market value; (2) sell to a cash investor, 7 to 14 days, ~70–85% of market value; (3) rent the home and use VA second-tier entitlement at the next duty station; or (4) qualify for the federal HAP buyout, which in 2026 is limited to Wounded, Injured, or Ill applicants and Surviving Spouses. The right choice depends on your report date, VA entitlement, home condition, and risk tolerance. This guide shows the math for sellers near Hunter Army Airfield, Fort Stewart, Pooler, Richmond Hill, Hinesville, Wilmington Island, Garden City, and Southside Savannah.

If you are trying to sell house fast on PCS orders in Savannah, the worst move is letting your report date make the decision for you.

“Your report date is not the day to start making real estate decisions.”

At a glance: the PCS seller options

- Best for fastest close: cash investor, 7 to 14 days, roughly 70% to 85% of market value

- Best for highest net: traditional listing, 35 to 60 days on market in Coastal Georgia, roughly 93% to 95% of market value after commission and closing costs

- Best for long-term wealth: rent the home and use VA second-tier entitlement on the next purchase

- Option most sellers do not actually have: HAP or military buyout

- Cost to consult ARC: $0, free 30-minute call

- Service area: Pooler, Richmond Hill, Wilmington Island, Southside Savannah, Garden City, Hinesville, Fort Stewart, and Hunter Army Airfield

If you want a military-specific real estate conversation before the clock gets tight, start with the Hunter AAF & Fort Stewart military relocation guide.

Get all 4 options mapped against your exact timeline

Book My Free 30-Min PCS Call →📞 Call 912-351-8935

No retainer. No quota. Veteran-led agent team.

The four options PCS sellers actually have

Most PCS sellers are told there are only two choices: list the home or take a cash offer.

That is not the whole board.

There are four options. Each can be right. Each can be wrong. The mistake is choosing one before the math is clear.

“Most PCS families I sit down with have been told there are two options, list or cash. There are four. The cost of not knowing the other two is usually tens of thousands of dollars over a five-year horizon.”

| Option | When it makes sense | Typical net to seller | Timeline |

| List traditionally | You have 60+ days, the home is in marketable condition, and the neighborhood supports normal buyer demand. | About 93% to 95% of market value after commission and closing costs | 35 to 60 days on market in Coastal GA planning ranges |

| Cash investor or iBuyer | You have under 30 days, major repair or VA Minimum Property Requirement issues, or no capacity for repairs and showings. | About 70% to 85% of market value | 7 to 14 days in most real closings |

| Rent it out | You can afford the carry, can handle a property manager, and have enough VA entitlement for the next home. | Monthly cash flow may be thin, but long-term return comes from principal paydown and appreciation | Indefinite |

| HAP or military buyout | Applies only in limited federal-program cases, not ordinary PCS moves from Hunter AAF or Fort Stewart in 2026. | Not applicable for most PCS sellers | Not applicable |

The right option is not the one that sounds easiest. It is the one that fits your report date, equity, mortgage payoff, VA loan position, property condition, and next-duty-station plan.

“Options-first, not sales-first.”

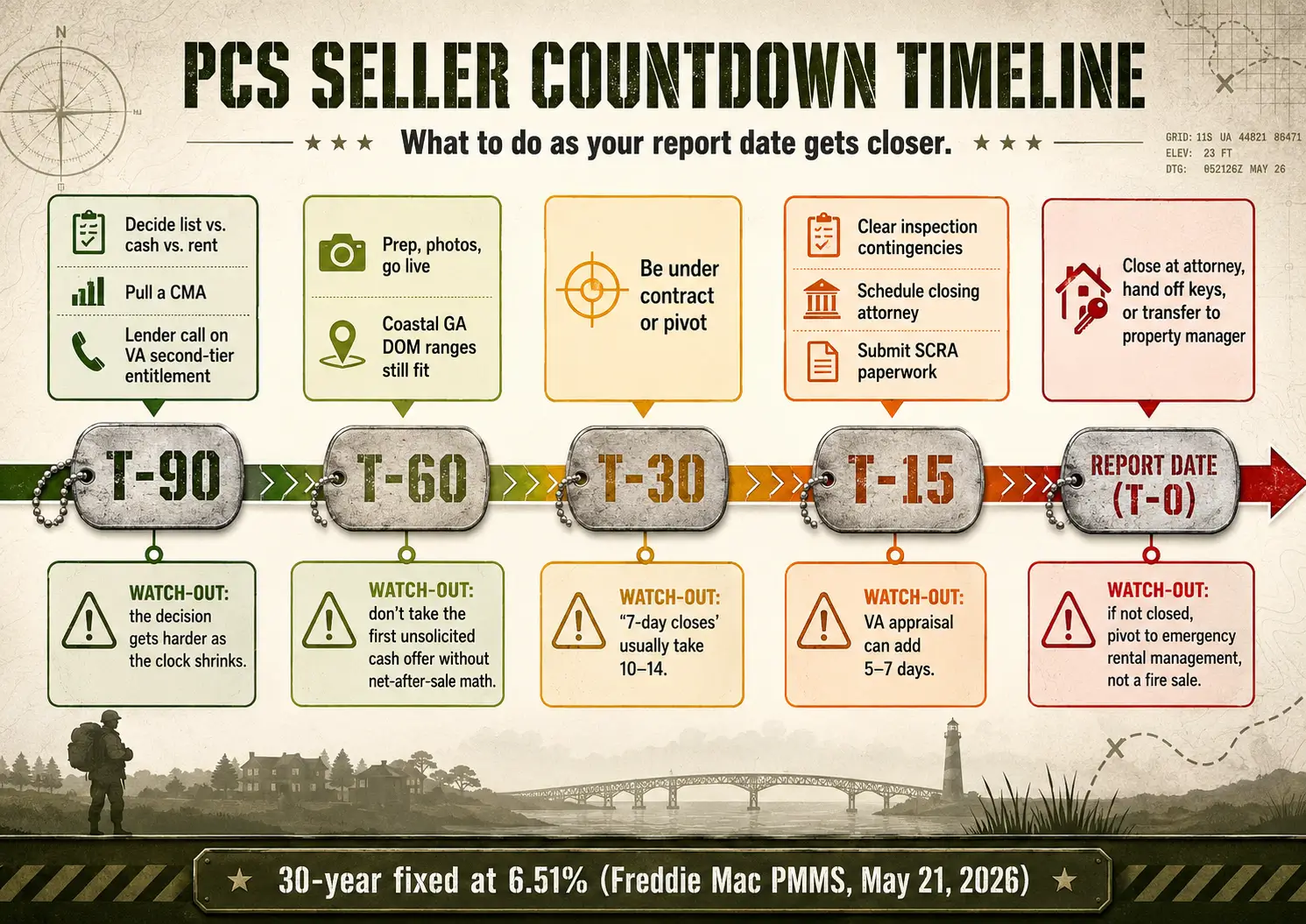

The PCS selling timeline

A PCS home sale is an operations problem before it is a marketing problem. The key date is not closing day. The key date is when the family decides which track to run.

Use this timeline against your report date.

| Milestone | Actions | Watch out for |

|---|---|---|

| T-90 days, orders in hand | Decide list vs cash vs rent. Pull a comparative market analysis, or CMA, with no commitment. If renting, run property-management math. Talk to your lender about VA second-tier entitlement. | The decision gets harder, not easier, as the timeline shrinks. Make it at T-90, not T-30. |

| T-60 days | If listing, complete prep work, schedule photos, and go live. Average days-on-market planning ranges in Coastal GA can still fit this window. | Cash investors may start calling after your listing goes live. Do not take the first one without comparing it to net-after-sale math. |

| T-30 days | Be under contract or decide whether to pivot. If the listing missed, fell through, or never launched, this is the inflection point. | Most “we close in 7 days” offers still take 10 to 14 days because of title work and closing-attorney scheduling. |

| T-15 days | Inspection contingencies should be cleared. Closing attorney should be scheduled. Submit SCRA mortgage relief paperwork if applicable. | A VA appraisal on the buyer’s loan can push closing by 5 to 7 days. Build the buffer. |

| Report date, T-0 | Close at the attorney, complete key handoff, or transfer rental management to the property manager. | If not closed, this should become an emergency rental-management handoff, not a fire sale. |

Freddie Mac’s Primary Mortgage Market Survey reported the 30-year fixed-rate mortgage at 6.51% as of May 21, 2026, which matters because higher rates can slow buyer urgency and make old assumable VA loans more valuable. Savannah-area market timing should also be refreshed at publish using GAMLS market reports or Savannah Area REALTORS data.

Option 1: List traditionally, the math at $400K

In brief: A traditional listing usually nets about 93% to 95% of market value over 35 to 60 days and wins when you have 60+ days and a market-ready home.

Traditional listing usually wins when you have enough time and the home can pass normal buyer financing. That does not mean it is always easy. It means the open market has a chance to compete for the property.

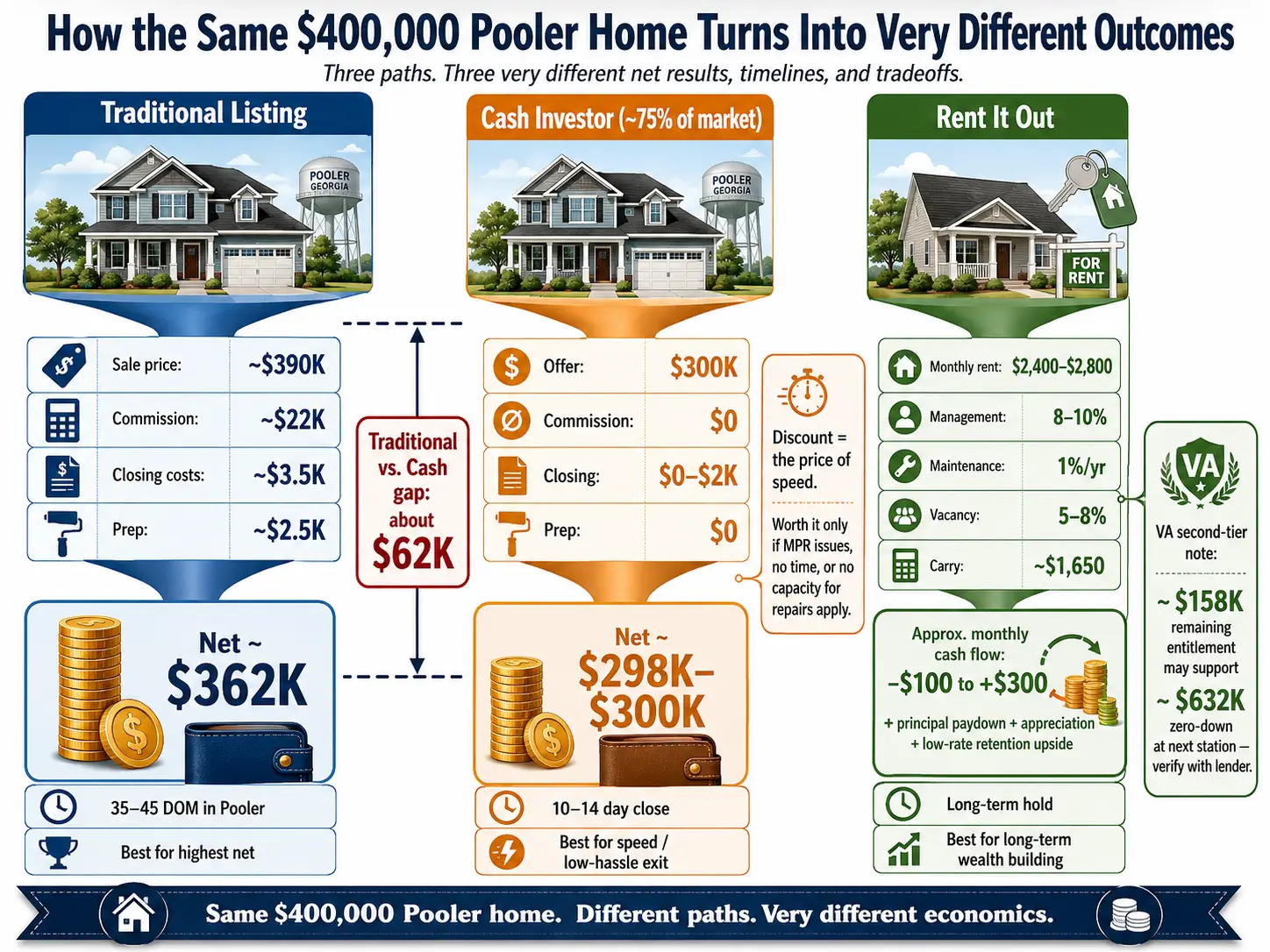

Here is the planning math on a $400,000 home in Pooler listed traditionally in 2026:

| Line item | Planning figure |

|---|---|

| List price | $400,000 |

| Sale price, typical 95% to 98% of list | About $390,000 |

| Commission, 5% to 6% total | About $22,000 |

| Seller-paid closing costs (title, attorney, transfer, Georgia-specific costs) | About $3,500 |

| Prep, minor repairs, staging | About $2,500 |

| Mortgage payoff and payoff fees | Varies |

| Approximate net to seller before mortgage payoff | About $362,000 |

This is not a promise. It is a planning model. Your actual net depends on condition, concessions, mortgage payoff, buyer financing, neighborhood, timing, and contract terms.

For PCS sellers, the timeline matters as much as the number.

Planning ranges for Coastal Georgia in 2026:

| Area | Typical days-on-market planning range |

|---|---|

| Pooler | 35 to 45 days |

| Richmond Hill | 35 to 45 days |

| Savannah Southside | 40 to 50 days |

| Garden City | 45 to 55 days |

| Hinesville | 45 to 60 days |

| Wilmington Island | 50 to 65 days, often due to flood-insurance friction |

This option wins when you have 60+ days, the home shows well, there are no major VA Minimum Property Requirement issues, and the market in your specific neighborhood supports normal buyer demand.

If you have a clean home in Pooler or Richmond Hill and 90 days before report date, selling to a cash investor just to avoid a few weeks of uncertainty may cost you real money.

Want the listing math run on YOUR home? Pooler, Richmond Hill, Hinesville & more

No retainer. No quota. Veteran-led agent team.

Option 2: Cash investor, when 70% to 85% is the right answer

In brief: A cash investor typically pays 70% to 85% of value and closes in 7 to 14 days, making it the right call mainly for tight timelines or homes with major repair issues.

A cash buyer is not automatically wrong.

A cash buyer is also not doing charity work.

They are buying your house at a discount, taking on speed, repairs, holding costs, resale risk, and profit margin. That is the service. The discount is the price.

A typical cash investor offer in Coastal Georgia may land around 70% to 85% of conservative after-repair value, depending on condition, timeline, and the buyer’s plan.

Here is the same $400,000 Pooler example:

| Line item | Planning figure |

|---|---|

| Market value reference | $400,000 |

| Cash offer, typical 75% of market value | $300,000 |

| Seller-paid commission | $0 |

| Seller-paid closing costs | Usually $0 to $2,000 |

| Prep and repairs | $0, sold as-is |

| Approximate net to seller | About $298,000 to $300,000 |

| Close time | Usually 10 to 14 days |

The discount is about $62,000 versus the traditional listing example.

That is the whole point of this section. The number should be clear.

A cash investor may be the right answer if the house has $40,000 in Minimum Property Requirement issues, such as failed roof, failed HVAC, foundation issues, or safety problems that would make a VA-financed buyer unlikely to close. In that case, the cash discount may be the cost of avoiding repairs, delays, failed appraisals, and repeated buyer fallout.

It may not be rational if the house would pass a VA appraisal cleanly and you have 60+ days. In that case, giving up $60,000 to save 30 days only makes sense if the emotional, logistical, or family cost of those 30 days is worth that amount to you.

For more on this cash-buyer math, read ARC’s guide to how much cash home buyers pay in Savannah.

“If the cash offer is genuinely the right call for your situation, I’ll say so and walk away. No retainer to recoup, no quota to hit. That happens about one in six conversations.”

Considering a cash offer? Get a sanity check before you sign

See the 2026 Cash Buyer Math →📞 Call 912-351-8935

No retainer. No quota. Veteran-led agent team.

Option 3: Rent it out, the VA entitlement play

In brief: Renting and reusing VA second-tier entitlement can build long-term wealth when the home breaks even and the next assignment runs 24 to 36 months.

This is the section many real estate sites skip because it does not start with a listing agreement.

But for some military families, renting the home is the best move.

If you bought in Coastal Georgia with a VA loan and still have entitlement available, you may be able to keep your current home as a rental and use VA financing again at the next duty station.

VA explains on its home loan entitlement and limits page that borrowers with full entitlement do not have a VA loan limit, as long as the lender approves the loan and the appraisal supports the price. If you do not have full entitlement because you are keeping a VA loan on the first home, the lender has to run remaining-entitlement math.

Here is the simple version:

- You keep the Pooler home.

- You rent it out.

- You use remaining VA entitlement, sometimes called second-tier entitlement, at the next duty station.

- Your lender calculates how much zero-down VA buying power remains.

For example, if your prior Pooler home used about $50,000 in entitlement and you have about $158,000 remaining, that remaining entitlement may support roughly $632,000 of zero-down VA purchase power at the next station, because VA’s guaranty math generally works around 25% of the loan amount. This is lender math, not a casual estimate, so verify it before making plans.

For the deeper military-buyer math, see ARC’s PCS playbook for service members.

Rental math on the $400K Pooler example

A typical 2026 rental model for a $350,000 to $450,000 Pooler home might look like this:

| Line item | Planning range |

|---|---|

| Monthly rent | $2,400 to $2,800 |

| Property management, 8% to 10% | $200 to $280 |

| Maintenance reserve, 1% of value per year | About $333 |

| Vacancy reserve, 5% to 8% | $130 to $200 |

| Insurance, HOA, taxes, and mortgage carry | Varies; planning assumption around $1,650 if bought at older loan terms |

| Approximate monthly cash flow | About -$100 to +$300 |

That cash flow number may not look exciting. The real return may come from principal paydown, long-term appreciation, keeping a low mortgage rate, and having the option to return to Coastal Georgia later.

But renting is not passive.

If the home does not rent within 30 days of departure, you are carrying it from the next duty station. If the tenant stops paying, you are the landlord from another state. If the HVAC fails in August, the repair call comes to you or your property manager.

Talk to a tax professional before making this decision. Rental depreciation, military residency, capital gains timing, and future sale treatment can change the picture.

This option wins when you qualify for second-tier entitlement, the house cash-flows or breaks even, you can hire a competent property manager, and the next assignment is likely 24 to 36 months.

Find out how much zero-down VA buying power you have left at the next station

Run My VA Second-Tier Entitlement Audit →

No retainer. No quota. Veteran-led agent team.

Option 4: HAP or military buyout, the option you probably do not have

In brief: The HAP buyout applies only to Wounded, Injured, or Ill applicants and Surviving Spouses, so most ordinary PCS sellers cannot use it.

The Homeowners Assistance Program, or HAP, is a federal program administered by the U.S. Army Corps of Engineers. It is not a general PCS seller program.

USACE states on its official Homeowners Assistance Program page that applications are currently being accepted only from Wounded, Injured, or Ill and Surviving Spouse applicants. The USACE HAP overview also says there is currently no HAP approved for BRAC impacted personnel and that applications for permanent reassignment and BRAC 2005 categories can no longer be accepted.

In plain English: if you heard about HAP from a friend at another duty station and assumed it applies to a normal PCS move from Hunter Army Airfield or Fort Stewart in 2026, do not build your plan around it.

It probably does not apply to your sale.

HAP probably doesn’t apply. The other three options still do.

Get the Real Options for My PCS Move →📞 Call 912-351-8935

No retainer. No quota. Veteran-led agent team.

The decision framework, which option fits you?

Use this as the first pass.

- Do you have more than 60 days on your PCS timeline?

- No: cash is on the table. Go to question 2.

- Yes: traditional listing is the default. Renting is the alternative if long-term hold makes sense. Go to question 3.

- If you have less than 60 days, does the home have major VA Minimum Property Requirement issues?

- Yes: cash is probably the right answer.

- No: you can still list, but use aggressive pricing, a shorter contingency window, and a clear backup plan.

- If you have 60+ days, do you have unused VA entitlement and can you afford the carry?

- Yes: renting is worth a serious look.

- No: traditional listing is probably the cleanest option.

- Does HAP apply?

- For ordinary PCS moves from Hunter AAF or Fort Stewart in 2026, assume no unless a military legal or official HAP review tells you otherwise.

Still not sure which option fits? That’s exactly what the 30-min call is for.

Map All 4 Options Against My Timeline →📞 Call 912-351-8935

No retainer. No quota. Veteran-led agent team.

SCRA and other military-specific protections sellers should know about

This section is not legal advice. It is a reminder to ask the right questions before you spend money you did not need to spend.

SCRA mortgage relief

The Servicemembers Civil Relief Act, or SCRA, may cap qualifying pre-service debts at 6% during active-duty service. The Department of Justice explains that servicemembers can request a 6% rate cap on most loans taken out before entering military service, including joint loans with a spouse, by giving written notice and a copy of military orders by the required deadline (DOJ SCRA 6% interest rate cap).

This does not directly sell the house. But it can reduce carrying cost if you are keeping the home as a rental or bridging a timing gap.

PCS lease termination rights

If you are renting at the next duty station before buying, SCRA lease rules may matter. Military OneSource explains that servicemembers who receive qualifying PCS or deployment orders may be able to terminate a residential lease early by giving written notice and a copy of orders (Military OneSource SCRA lease termination guidance).

This helps if you plan to rent first, then buy later.

VA loan assumability

Your existing VA loan may be one of the strongest selling points you own.

VA borrower materials state that for VA loans committed on or after March 1, 1988, you may sell your home to someone who agrees to assume your loan if the loan holder or VA approves the creditworthiness of the purchaser (VA borrower rights and assumable loan notice).

That can matter in a high-rate environment. If your current VA loan rate starts with a 3 or 4, and market rates are in the mid-6s, the rate itself may become part of the value proposition.

Important warning: if a non-veteran assumes your VA loan, your entitlement may remain tied up unless released according to VA rules. Do not market an assumption casually. Talk to your lender, your agent, and a VA-savvy loan officer first.

“In 2026, if your VA loan has a rate that starts with a 3, that loan is one of the best things you own. Don’t hand it back to the lender on a refinance. Sell it with the house.”

Veteran-owned, military-focused, no-pressure conversation

Talk to a Veteran-Led Agent Team →📞 Call 912-351-8935

No retainer. No quota. Veteran-led agent team.

The Coastal Georgia market reality, 2026

PCS sellers need local context, not national housing takes.

In Pooler, new construction is still moving, and builder credits can shape buyer expectations. If your resale home competes directly against a builder offering incentives, your price, condition, and closing-cost strategy need to account for that.

Richmond Hill still pulls families because of schools and access to Fort Stewart, Hunter AAF, Pooler, and Savannah. For many military families, Richmond Hill is not just a home decision. It is a commute, school, and household-stability decision.

Wilmington Island can move more slowly when flood insurance enters the buyer’s payment. If a buyer’s lender requires flood insurance, that payment has to fit underwriting. A home that looks affordable on purchase price may not feel affordable once flood insurance, wind coverage, taxes, and HOA are added. ARC’s guide to Savannah flood zones explains that math in detail.

Hinesville is different. The rental concentration is high. Some buyers like that because rental demand supports long-term hold. Other buyers see more resale competition. If you are selling near Fort Stewart, the strategy needs to account for that supply.

Rates also matter. Freddie Mac’s PMMS showed the 30-year fixed-rate mortgage at 6.51% as of May 21, 2026. In that environment, old VA loans and monthly-payment strategy matter more than they did when rates were lower.

If you are comparing options near Hunter AAF or Fort Stewart, our military relocation service for Coastal Georgia is the central resource.

The 30-minute call, what we cover

This is not a listing pitch.

It is an options call.

In 30 minutes, we cover:

- Your PCS timeline mapped against your report date

- Your home’s current market position

- A rough CMA using your actual neighborhood and condition

- Traditional listing net estimate

- Cash-offer sanity check

- Sell-vs-rent math using your mortgage, taxes, insurance, HOA, and rent range

- Second-tier VA entitlement audit if you are considering keeping the home

- A three-name shortlist of cash buyers I would actually send my own family to, if cash is the right call

- What has to happen this week so you are not forced into a worse decision next month

The goal is not to make the decision for you. The goal is to put the real options on one page.

Free, 30 min, no pressure.

Sell-vs-rent math · Cash-offer sanity check · 3-name cash buyer shortlist

Schedule My Free 30-Minute Options Call →📞 Call 912-351-8935

No retainer. No quota. Veteran-led agent team.

Join The Discussion