The 2026 VA Funding Fee, Explained: Coastal Georgia Math and How to Roll It In

A $7,500 funding fee adds roughly $50 to the monthly payment on a 30-year mortgage at typical 2026 rates. For most Coastal Georgia VA buyers, the funding fee is not paid as cash on closing day. It is usually rolled into the VA loan, which preserves cash for moving, inspections, repairs, furnishings, deposits, and the first few months of ownership. The key exceptions are disabled veterans, certain active-duty Purple Heart recipients, and eligible surviving spouses, who may be exempt entirely. In our view, the funding fee is best understood as the cost of accessing the VA loan’s zero-down and no-monthly-mortgage-insurance structure, not as a random add-on. The right move depends on your exemption status, prior VA use, seller concessions, and cash-flow plan.

At a glance

- 2026 VA funding fee: 2.15% first use / 3.3% subsequent use with 0% down. The 5% and 10% down tiers drop the fee to 1.5% and 1.25%.

- Disabled veterans receiving VA disability compensation are exempt, along with certain Purple Heart recipients and surviving spouses receiving DIC.

- The fee can be rolled into the loan, so most Coastal Georgia buyers finance it instead of paying cash at closing.

- A seller can pay the fee, but it counts toward VA’s 4% seller concession cap.

Last updated: June 2026

What the VA funding fee is and why it exists

In brief: The VA funding fee is a one-time VA loan charge that helps support the program because VA loans can offer zero down payment and no monthly mortgage insurance.

The VA funding fee is a one-time payment charged on many VA-backed and VA direct home loans. It helps reduce the cost of the VA home loan program to taxpayers because the program does not require a down payment or monthly mortgage insurance for eligible buyers, according to the official VA funding fee guidance. (Veterans Affairs)

In plain English, the VA funding fee replaces the kind of monthly PMI cost that many conventional buyers pay when they put less than 20% down. Instead of paying a separate mortgage insurance bill every month, a VA buyer who is not exempt usually pays one fee at closing, either in cash or by financing it into the loan.

That distinction matters in Coastal Georgia because many military buyers near Hunter Army Airfield, Fort Stewart, Savannah, Pooler, Richmond Hill, Hinesville, and surrounding communities are trying to protect cash during a PCS move. We cover the local buying process more broadly in the Hunter AAF and Fort Stewart buyer’s guide, but this article focuses on one specific line item: the 2026 VA funding fee.

As a veteran-led real estate team, we look at this math through the same lens our military clients do: what preserves flexibility, what keeps the closing realistic, and what prevents a buyer from being surprised after the lender updates the Loan Estimate.

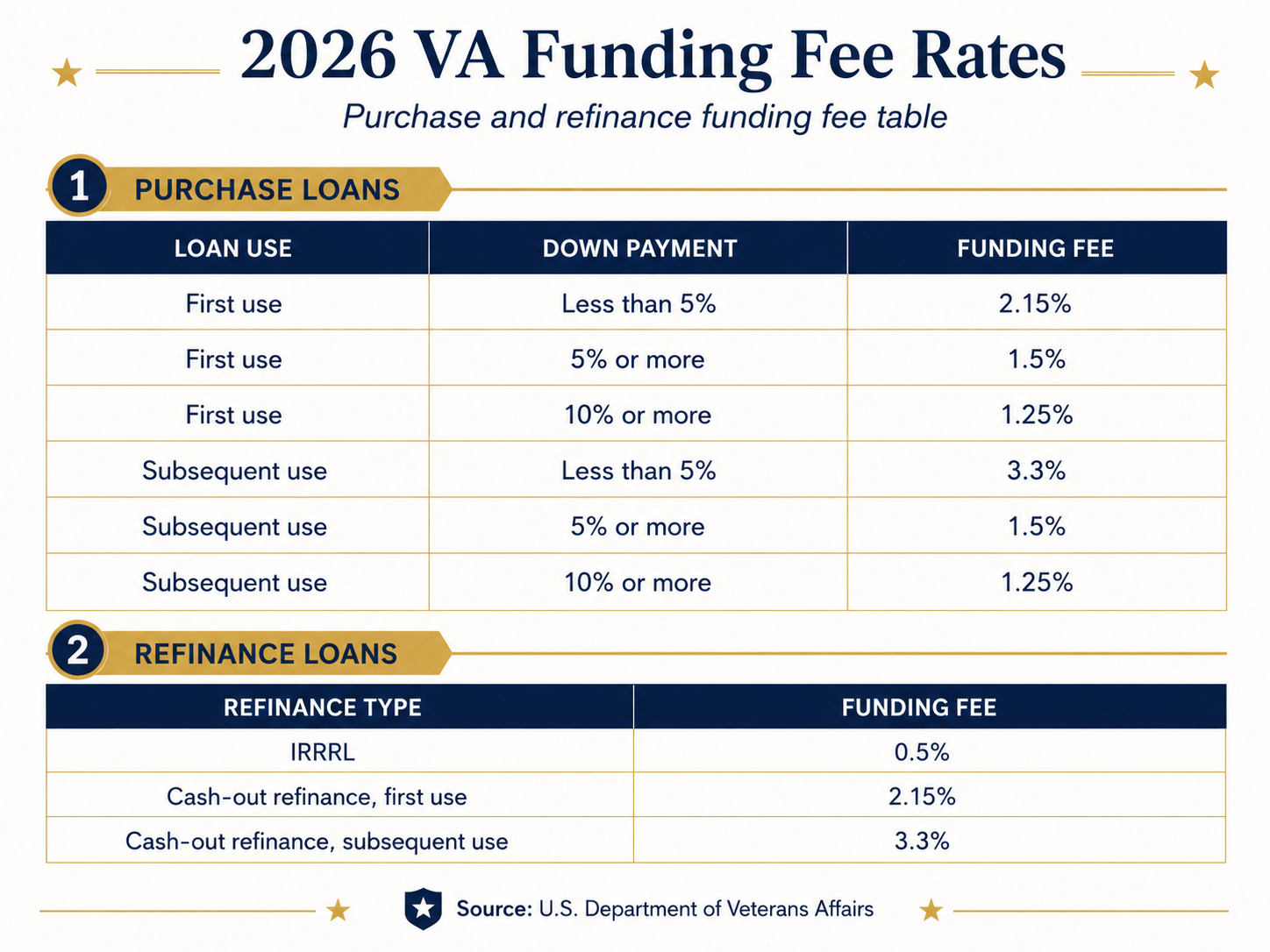

2026 VA funding fee rate tables: purchase and refinance

In brief: For 2026 purchase loans, the VA funding fee ranges from 1.25% to 3.3% for non-exempt buyers, depending on down payment and whether this is first or subsequent VA use.

A first-use VA purchase with less than 5% down carries a 2.15% funding fee in 2026, while a subsequent-use VA purchase with less than 5% down carries a 3.3% funding fee. The official VA rate charts list the following purchase and refinance percentages. (Veterans Affairs)

VA purchase and construction loans

VA use | Down payment | 2026 VA funding fee |

|---|---|---|

First use | Less than 5% | 2.15% |

First use | 5% or more | 1.5% |

First use | 10% or more | 1.25% |

After first use | Less than 5% | 3.3% |

After first use | 5% or more | 1.5% |

After first use | 10% or more | 1.25% |

VA refinance loans

Loan type | 2026 VA funding fee |

|---|---|

IRRRL | 0.5% |

Cash-out refinance, first use | 2.15% |

Cash-out refinance, after first use | 3.3% |

The “after first use” line is important for buyers using VA benefits again, especially if they still own another VA-financed home or are working through entitlement restoration. If that sounds like your situation, read our plain-English guide to second-tier VA entitlement before assuming you are limited to a conventional loan.

Who is exempt from the funding fee

In brief: Disabled veterans receiving VA service-connected disability compensation are exempt, along with certain active-duty Purple Heart recipients and surviving spouses receiving DIC.

A disabled-veteran exemption can remove thousands of dollars from the loan math. VA says a buyer does not have to pay the funding fee if they receive VA compensation for a service-connected disability, would be eligible for that compensation but receive retirement or active-duty pay instead, receive DIC as a surviving spouse, have a qualifying pre-discharge rating, or are an active-duty service member who provides evidence of receiving a Purple Heart before closing, per the official VA exemption list. (Veterans Affairs)

The exemption should be confirmed early, not discovered late. VA’s COE process includes funding fee exemption status, and VA lender guidance notes that a corrected COE may be used when the veteran’s funding fee exemption status needs to be updated. (Benefits)

Alex’s note: If you believe you are exempt, we want the lender checking the COE before we write the offer strategy around cash to close. A correct exemption status can change the entire conversation.

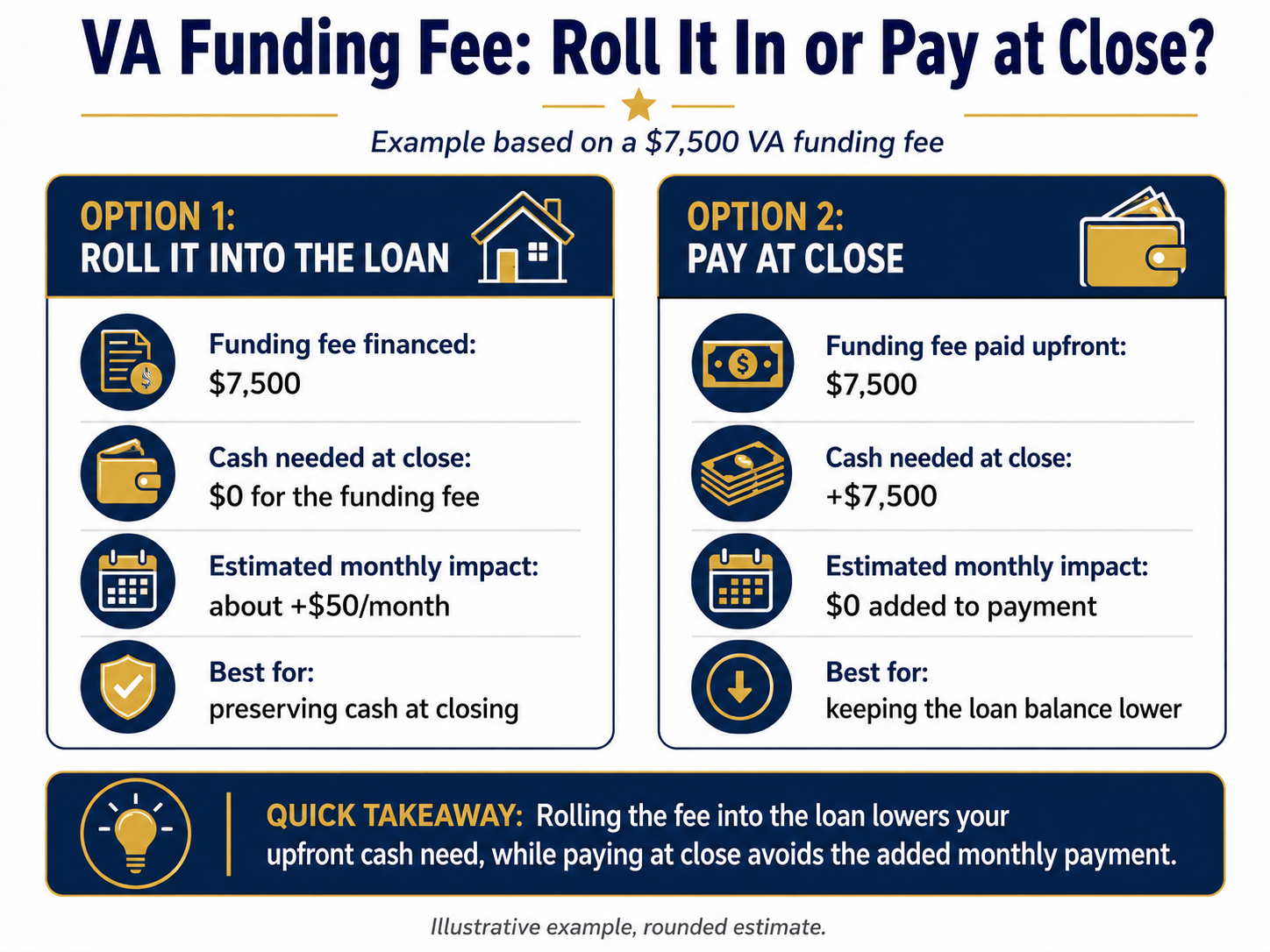

Roll it into the loan vs. pay at close: the cash-flow choice

In brief: Most Coastal Georgia VA buyers roll the funding fee into the mortgage, trading a slightly higher monthly payment for lower cash needed at closing.

Rolling a $7,500 funding fee into a 30-year mortgage adds about $47 per month at a 6.48% 30-year fixed-rate assumption. Freddie Mac reported a 6.48% average 30-year fixed mortgage rate as of June 4, 2026, and that benchmark is used here only to show the approximate payment impact, not to quote a buyer-specific VA rate. (freddiemac.com)

VA allows buyers to pay the funding fee at closing or include it in the loan and pay it over time, according to the official VA payment guidance. (Veterans Affairs) VA also states that on a purchase or construction loan, the funding fee is the only closing cost that can be financed into the loan amount. (Veterans Affairs)

For many service members, rolling it in is the practical move. A PCS buyer may be juggling temporary lodging, storage, deposits, travel, furniture, vehicle expenses, and the timing gap between one housing situation and the next. Paying the fee in cash can reduce the loan balance, but it also removes liquidity at the exact moment when flexibility matters.

National PCS-realtor aggregators and general military-buyer sites often explain the VA funding fee in national terms. ARC’s value is narrower and more practical: we apply the math to Coastal Georgia homes, local closing customs, seller strategy, and the realities of Fort Stewart and Hunter AAF relocation timelines.

Coastal Georgia worked example: $350K Pooler purchase

In brief: On a $350,000 Pooler purchase with first VA use and less than 5% down, the 2.15% VA funding fee is $7,525, creating a total financed VA loan amount of $357,525 if rolled in.

Here is the clean math for a Coastal Georgia buyer looking at a $350,000 Pooler home:

Item | Amount |

|---|---|

Purchase price | $350,000 |

Down payment | $0 |

VA use | First use |

Funding fee rate | 2.15% |

VA funding fee | $7,525 |

Total VA loan amount if rolled in | $357,525 |

Approximate added monthly principal and interest at 6.48% over 30 years | $47 |

The $7,525 fee comes from multiplying the $350,000 loan amount by the 2.15% first-use, less-than-5%-down funding fee. (Veterans Affairs) If that fee is rolled into the loan, the borrower finances $357,525 instead of $350,000. At the 6.48% Freddie Mac benchmark used for illustration, the added monthly principal and interest is about $47. (freddiemac.com)

This is why we do not treat the funding fee as a simple yes-or-no closing cost. The better question is whether the buyer would rather bring $7,525 more to closing or finance that cost and preserve cash. For many Coastal Georgia buyers, the second option wins.

How seller concessions interact with the funding fee

In brief: A seller can pay the VA funding fee, but it counts as a seller concession and is subject to VA’s 4% concession cap.

On a $350,000 home, the VA’s 4% seller concession cap equals $14,000, and a $7,525 seller-paid funding fee would leave $6,475 of concession room for other concession items. VA says seller concessions are limited to no more than 4% of the home’s reasonable value, and that concessions include credits for the VA funding fee, debt payoff, or prepayment of the buyer’s hazard insurance. (Veterans Affairs)

This is where offer strategy matters. In a slower listing situation, asking the seller to pay the funding fee can be a smart way to reduce the buyer’s effective cash burden without lowering the headline purchase price. In a competitive multiple-offer situation, rolling the fee into the loan may make the offer cleaner.

We explain the broader rules in our guide to VA loan seller concessions, but the short version is simple: seller-paid funding fee can work, but it has to fit the concession cap, the appraisal, and the seller’s motivation.

Alex’s note: We do not ask for concessions just because the rule allows them. We ask when the numbers, leverage, and buyer cash-flow goal all line up.

Frequently asked questions

In brief: The most important 2026 VA funding fee questions are rate percentage, exemption status, whether the fee can be rolled in, and whether the seller can pay it.

What is the VA funding fee for a 2026 purchase loan?

For purchase loans in 2026, the VA funding fee on first use is 2.15% with less than 5% down, 1.5% with 5% or more down, and 1.25% with 10% or more down. On subsequent use, it is 3.3% with less than 5% down, and 1.5% or 1.25% at the 5% and 10% down tiers. Disabled veterans with service-connected compensation are exempt. (Veterans Affairs)

Do disabled veterans pay the VA funding fee?

No. Veterans who receive VA service-connected disability compensation are exempt from the VA funding fee on purchase and refinance loans. Purple Heart recipients on active duty are also exempt, as are surviving spouses receiving DIC benefits. The exemption is confirmed through the Certificate of Eligibility process. (Veterans Affairs)

Can I roll the VA funding fee into my loan amount?

Yes, and most Coastal Georgia VA buyers do. Rolling the funding fee into the loan means you finance it over 30 years instead of paying it in cash at close. A $7,500 funding fee adds roughly $47 to $50 to the monthly payment on a 30-year mortgage using the June 2026 Freddie Mac benchmark. (freddiemac.com)

Can the seller pay my VA funding fee on a Coastal Georgia purchase?

Yes, the seller can pay the funding fee, but because it is a concession rather than a customary closing cost, it counts toward the 4% VA concession cap. On a $350,000 home, that 4% is $14,000 total, so paying a $7,525 funding fee leaves $6,475 of concession room for other eligible items. (Veterans Affairs)

What is the VA funding fee on an IRRRL refinance?

The VA funding fee on an Interest Rate Reduction Refinance Loan, or IRRRL, is 0.5% regardless of prior use. This is significantly lower than the purchase or cash-out refinance funding fees, which is part of why IRRRL can be a cash-efficient way for an existing Coastal Georgia VA homeowner to lower their rate. (Veterans Affairs)

Closing CTA

Buying with a VA loan in Coastal Georgia should not feel like decoding a lender worksheet alone. We help military buyers understand the funding fee, COE, entitlement, concessions, cash to close, and local offer strategy before they are under contract.

Schedule a free 30-minute call with ARC through our Coastal Georgia military relocation help page. We will walk through your PCS timeline, target area, VA loan assumptions, and the questions to ask your lender before you write an offer.

Final disclosure: The ARC Platform is a real estate practice affiliated with Keller Williams Realty. Alex Rodino is a licensed Georgia Realtor®, GA Real Estate License #443565. This article is for informational purposes only and is not legal, tax, lending, or financial advice. Mortgage terms, eligibility, funding fee status, rates, and closing costs depend on lender underwriting and official VA guidance. Equal Housing Opportunity.

Join The Discussion