How to Get Your VA Loan Certificate of Eligibility (COE): A Step-by-Step Guide for Coastal Georgia Buyers

If you are still mapping the overall homebuying process around PCS timing, BAH, commute, and neighborhood fit, start with the Hunter AAF and Fort Stewart buyer’s guide before you tour homes.

What the COE is and why you need it

In brief: A COE is the VA document that proves your basic eligibility for a VA-backed home loan. It does not approve the loan by itself, but a lender needs it before a VA purchase loan can close.

A VA loan certificate of eligibility is the Department of Veterans Affairs document that tells a lender you qualify for the VA home loan benefit based on your service history or eligible surviving-spouse status. It is not a mortgage approval, appraisal approval, or guarantee that a specific home will qualify. It is the eligibility key that lets the lender move your file into VA underwriting.

The COE typically shows entitlement information, prior VA loan use, and an entitlement code. If you have never used your VA loan benefit, the file is usually straightforward. If you have a current VA loan, kept a former home after a PCS, or had a previous VA loan that was not fully restored, the COE becomes more important because it helps the lender calculate remaining entitlement.

VA.gov says a COE is used to show your lender that you qualify for a VA-backed home loan, and it lists the required service documents by borrower type in its official COE instructions. (Veterans Affairs)

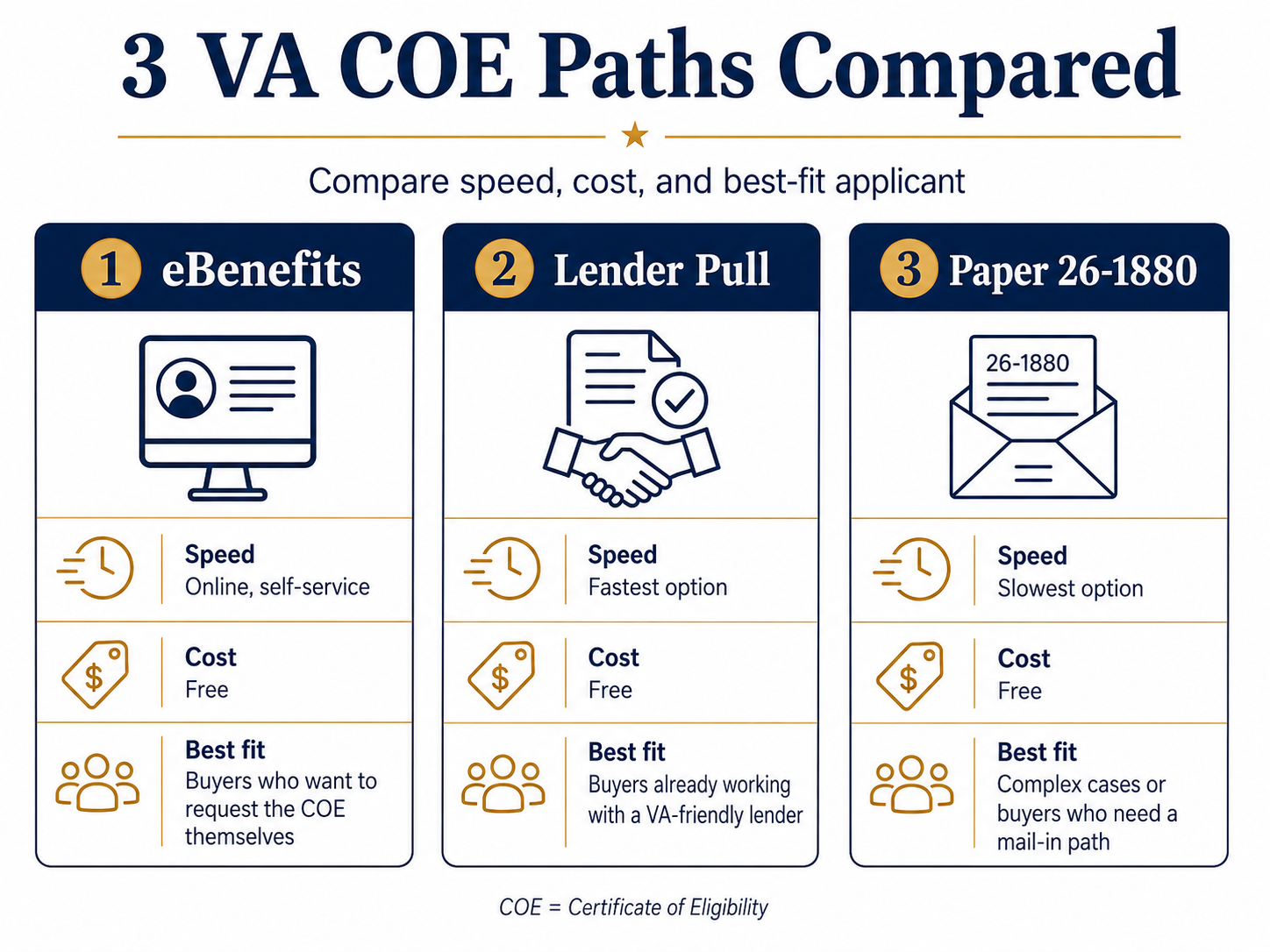

Three ways to get a COE: speed and friction compared

In brief: There are three practical paths: lender pull, VA.gov self-service, and paper mail. Most Coastal Georgia buyers should try the lender pull or VA.gov first because paper is the slowest option.

The difference between the fastest and slowest COE path can be the difference between same-day pre-approval and weeks of delay.

VA’s home loan site says lenders may use Web LGY, an internet-based application that can issue an online COE in a matter of seconds when VA has enough records. The same VA guidance lists mail as an option through VA Form 26-1880, while noting that mail requests take longer than online or lender requests through Web LGY and VA mail options. (VA Benefits)

Path 1: Lender pull via Web LGY / ACE (fastest)

In brief: If you are serious about buying, the lender pull is usually the cleanest path. A VA-friendly lender can often retrieve the COE before you finish the pre-approval conversation.

The fastest path is to let a VA-friendly Coastal Georgia lender pull your COE through the VA’s Web LGY system. In many clean files, the lender enters the required identifying and service information, the automated system checks VA records, and the COE is returned immediately.

Bring or upload the right document before the call:

VA.gov confirms that Veterans need DD214 paperwork, active-duty members need a Statement of Service, and Guard or Reserve members may need activation documents or points records depending on their status in the service-document checklist. (Veterans Affairs)

Alex’s note: As a veteran who has run the COE workflow myself, we want buyers to avoid creating delay where none is needed. If the lender can pull the COE while you are already starting pre-approval, that is usually better than mailing paperwork and waiting.

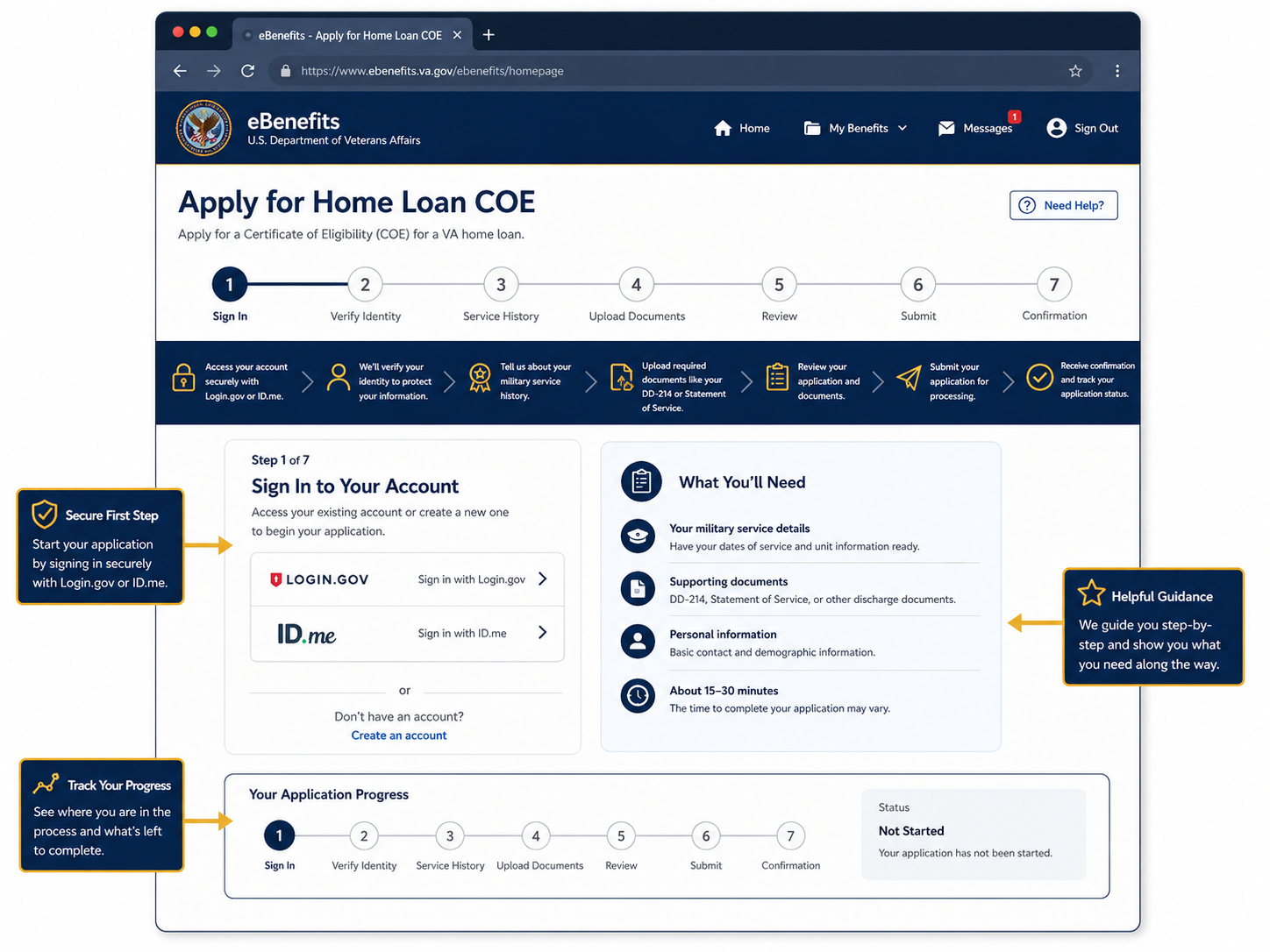

Path 2: VA.gov COE Portal (self-service)

In brief: VA.gov is the right self-service path if you want to request, download, or check your COE yourself. Use a verified Login.gov or ID.me account and have your service documents ready.

VA.gov lets you request a COE, check status, and download an approved COE through the official online workflow. The VA sign-in page lists Login.gov and ID.me as supported sign-in options, and the COE request page directs users to sign in to request, get, or check a COE through VA.gov sign-in. (Veterans Affairs)

Use this path when you want to control the request yourself or when you are not ready to speak with a lender yet. The basic flow is simple:

Automatic approval is more likely when VA already has clean, matching service records. Manual review is more likely when the record is incomplete, the borrower has Guard or Reserve service, there is prior VA loan use, or the buyer is applying as a surviving spouse.

Path 3: VA Form 26-1880 by mail (last resort)

In brief: Use the mail path only when lender pull and VA.gov do not solve the issue. It works, but it is slower and more document-sensitive.

VA Form 26-1880 is the paper request for a VA home loan Certificate of Eligibility. VA’s current form page identifies it as the “Request for a Certificate of Eligibility,” with a December 2025 revision date, and notes that the COE must be brought to the lender to prove VA home loan eligibility through VA Form 26-1880. (Veterans Affairs)

Use paper when your service history is complicated, records are missing, digital verification fails, or the lender asks you to submit a manual package. Mail the completed form to the Regional Loan Center address listed on the form. Include supporting service documents so the request does not stall.

If it stalls, use VA’s online COE status tool or call the VA home loan representative line. VA.gov says borrowers can check status, review letters, upload support documents, and download an approved COE through the COE status tool. (Veterans Affairs)

Special situations: surviving spouse, National Guard, Reservist, prior service

In brief: Not every borrower should use the same document package. Surviving spouses, Guard members, Reservists, and buyers with prior VA loan use should expect extra verification.

Surviving spouses use a different path. VA.gov says an eligible surviving spouse needs a COE to show the lender they qualify, and if they receive Dependency and Indemnity Compensation, they use VA Form 26-1817 with the Veteran’s DD214 if available through the surviving-spouse COE process. (Veterans Affairs)

National Guard and Reserve documentation depends on activation history. Activated Guard members may need a DD214 or other discharge documents; certain Guard members with qualifying active-duty service may need documents showing activation dates, annual point statements, DD220, or orders. Guard members who were never activated may need NGB Form 22 and NGB Form 23.

Prior service and prior VA use matter because the COE helps the lender see whether entitlement was used, restored, or remains available. If you kept a previous VA-financed home after a PCS, the next purchase may involve second-tier VA entitlement. That does not automatically block the purchase, but it does make the COE review more important.

After you have your COE: what comes next in a Coastal GA purchase

In brief: The COE starts the lending process, but the next step is turning it into a real pre-approval and a Coastal Georgia search plan. Do not stop at “eligible”; move to “ready to write.”

Once you have the COE, send it to a VA-friendly Coastal Georgia lender for pre-approval. The lender still needs to review credit, income, assets, debt-to-income ratio, residual income, and the future property. VA.gov also notes that after COE request, the lender reviews appraisal, credit, and income information before deciding whether to accept the application through VA loan next steps. (Veterans Affairs)

Then build your home search around real numbers, not guesses. For many Hunter AAF and Fort Stewart buyers, that means aligning the pre-approval with BAH, commute, school preferences, flood-zone comfort, insurance expectations, and PCS timing.

National PCS-realtor aggregators can introduce you to someone broadly. Our difference is local: ARC is veteran-led, Coastal Georgia-specific, and built around the actual decisions military buyers face between Savannah, Pooler, Richmond Hill, Hinesville, Georgetown, island communities, and the Fort Stewart and Hunter AAF commute patterns.

This is also the point to understand offer structure. In some cases, VA loan seller concessions can help a buyer manage closing costs, but the strategy has to fit the property, seller, and local market. If you want veteran-led guidance before you start writing offers, ARC offers Coastal Georgia military relocation help.

Alex’s note: We do not want military buyers guessing their way through the first step. Get the COE, get a lender who understands VA, and then let’s match the approval to the right Coastal Georgia search strategy.

Frequently asked questions

In brief: Most COE questions come down to timing, documents, fees, and repeat use. The safest answer is to start with VA.gov or a VA-friendly lender, then escalate only if the case is complicated.

Join The Discussion