TL;DR: Most inland Savannah neighborhoods (Ardsley Park, Starland, Pooler, Godley Station, Richmond Hill, Rincon) sit in lower-risk Zone X, while Tybee Island and marsh or creek-adjacent parts of Wilmington Island, Skidaway Island, and Isle of Hope fall in high-risk AE or VE zones where flood insurance is usually required. Your exact zone drives your insurance cost and whether your lender mandates coverage, so always confirm the specific address on the FEMA Flood Map Service Center before you make or accept an offer.

By Alex Rodino, US Military Veteran, licensed Georgia REALTOR®, and founder of the Alexander Rodino Collective (ARC Platform) at Keller Williams Coastal Area Partners.

Alex helps buyers and sellers across Savannah, Tybee Island, Wilmington Island, Skidaway Island, Isle of Hope, Pooler, Richmond Hill, Rincon, and the broader Coastal Georgia market. ARC focuses on the carrying-cost math behind flood zones, insurance, and resale risk before any offer goes in.

Last updated: June 30, 2026

Two kinds of people end up Googling Savannah flood zones. The first is a buyer staring at a listing they love, trying to figure out whether the AE designation in the description is a deal-breaker or a footnote. The second is a homeowner who just opened a flood-insurance renewal that does not match the one from last year and is wondering if they are in a different zone than they thought.

Both of you are in the right place. This guide is built by a working Coastal Georgia REALTOR®, for people who need the practical translation of FEMA’s zone codes into things that matter: which neighborhoods sit in which zones, what flood insurance actually costs in 2026 Savannah dollars, when lenders require it, and what to do with the information before you make an offer or accept one.

We will cover the FEMA zone definitions in plain English, walk through a neighborhood-by-neighborhood reference for Chatham, Bryan, and Effingham counties, give you specific premium ranges by zone, and finish with the decision framework every buyer should run before signing an offer on a flood-zoned home.

No insurance sales pitch. No real estate sales pitch. Just the version of the conversation a friend in the business would have with you over coffee.

Quick Answer:

Most of Ardsley Park, Starland, Gordonston, Pooler, Godley Station, Berwick, Richmond Hill, and Rincon sit in low-risk Zone X. Tybee Island and parts of Wilmington Island, Skidaway Island, Isle of Hope, Whitemarsh, and Thunderbolt sit in AE or VE, where flood insurance is lender-required and 2026 premiums commonly range $900 to $8,000+ per year. Always confirm by exact address at the FEMA Flood Map Service Center before making an offer.

If you are already weighing an offer on a flood-zoned property, ARC’s buyer-side representation walks the carrying-cost math with you before any offer goes in.

Why your Savannah flood zone matters more than you think

Your flood zone is not just a map label. It can change your loan requirements, your closing timeline, your monthly payment, your resale value, and your post-storm recovery process.

In Savannah, that matters because flood risk is not limited to beachfront property. Chatham County is flat, low-lying, and exposed to heavy rainfall, storm surge, creeks, marshes, tidal rivers, drainage systems, and coastal storms. The City of Savannah’s flood protection information explains that Chatham County’s coastal geography creates flood risk during heavy rainfall and storm surge events. City of Savannah Flood Protection Information (savannahga.gov)

The lender requirement

If a home is in a Special Flood Hazard Area, usually a FEMA zone that starts with A or V, flood insurance is typically required when the buyer uses a federally backed or federally regulated mortgage. FEMA states that homes and businesses in high-risk flood areas with mortgages from government-backed lenders are required to have flood insurance. FEMA flood insurance overview (FEMA)

That means a property in Zone AE or Zone VE can affect more than insurance. It can affect underwriting, escrow, debt-to-income calculations, and the final monthly payment. If the flood premium is $2,400 per year, that is about $200 per month added to the housing cost. If it is $6,000 per year, that is about $500 per month. That number can change what a buyer can afford.

Some portfolio or non-conforming lenders may make their own decisions, but for most buyers using FHA, VA, USDA, Fannie Mae, Freddie Mac, or a federally regulated lender, the flood determination matters before closing.

The premium math

Flood insurance pricing is no longer based only on the letter zone. FEMA’s Risk Rating 2.0 is now fully implemented, and FEMA explains that NFIP pricing considers more property-specific factors than the old rating system. FEMA Risk Rating 2.0 (FEMA)

That means two homes in the same Savannah neighborhood can have very different premiums. A Wilmington Island home in AE with an elevation certificate and elevated mechanicals may price very differently from another AE home on the same street with a lower first-floor elevation, prior claims, or expensive replacement cost.

Flood maps still matter. Chatham County Engineering explains that Flood Insurance Rate Maps are used by lenders to determine flood insurance requirements and by FEMA to help determine flood insurance rates. Chatham County flood zone definitions (Chatham County Engineering)

But the zone is the starting point, not the final quote.

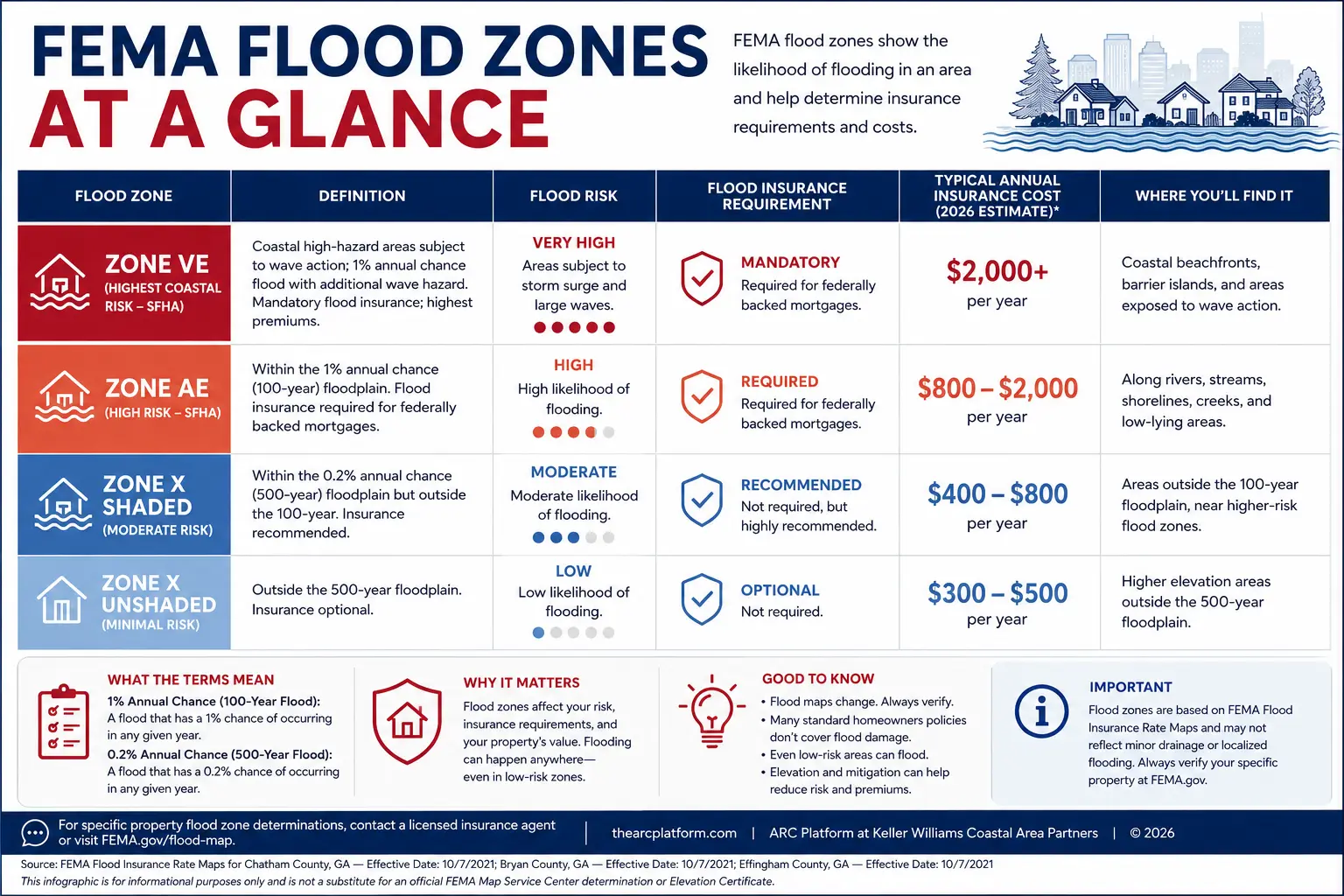

AE, X, VE, and the rest: what each FEMA flood zone means in plain English

The phrase that matters is Special Flood Hazard Area, often shortened to SFHA. FEMA defines SFHA as an area with special flood, mudflow, or flood-related erosion hazards shown on a Flood Hazard Boundary Map or Flood Insurance Rate Map. FEMA SFHA definition (FEMA)

In plain English: if your zone starts with A or V, the property is usually in a high-risk FEMA flood area. If your zone is X, flood insurance is usually not lender-required, but that does not mean the risk is zero.

Zone | Risk level | Insurance required by lenders? | What it means |

|---|---|---|---|

Zone X, unshaded | Minimal | No | Outside the 500-year floodplain. Most of inland Savannah and many western suburbs sit here. Flood insurance is optional, but still worth pricing because Coastal Georgia storms can create flood damage outside mapped high-risk zones. |

Zone X, shaded or X500 | Moderate | No | Inside the 500-year floodplain but outside the 100-year floodplain. Often borders SFHA zones. Premiums are usually lower than AE or VE and may be a smart risk-management move. |

Zone A | High, SFHA | Yes | 100-year floodplain, but no base flood elevation has been determined. Less common in Chatham County than AE. |

Zone AE | High, SFHA | Yes | 100-year floodplain with base flood elevation determined. This is one of the most common high-risk zones in Coastal Georgia. Premiums are elevation-sensitive under Risk Rating 2.0. |

Zone AH / AO | High, SFHA | Yes | Shallow flooding, usually ponding or sheet flow. Less common locally, but still lender-required if mapped as SFHA. |

Zone VE | High coastal, SFHA | Yes | Coastal floodplain with additional wave-action hazard. Tybee Island and parts of Skidaway Island can include VE zones. Premiums are usually much higher than AE because wave action increases risk. |

Zone D | Undetermined | Lender discretion | Areas with possible but undetermined risk. Rare in Chatham County. A lender may still require coverage. |

FEMA’s own flood-zone glossary explains that Special Flood Hazard Areas are tied to the 1-percent-annual-chance flood event, often called the 100-year floodplain. FEMA flood zones glossary (FEMA)

The simple rule: if the zone starts with A or V, expect flood insurance to be required on most financed purchases. If it is X, insurance is usually optional, but the decision should still be made with a quote, not a guess.

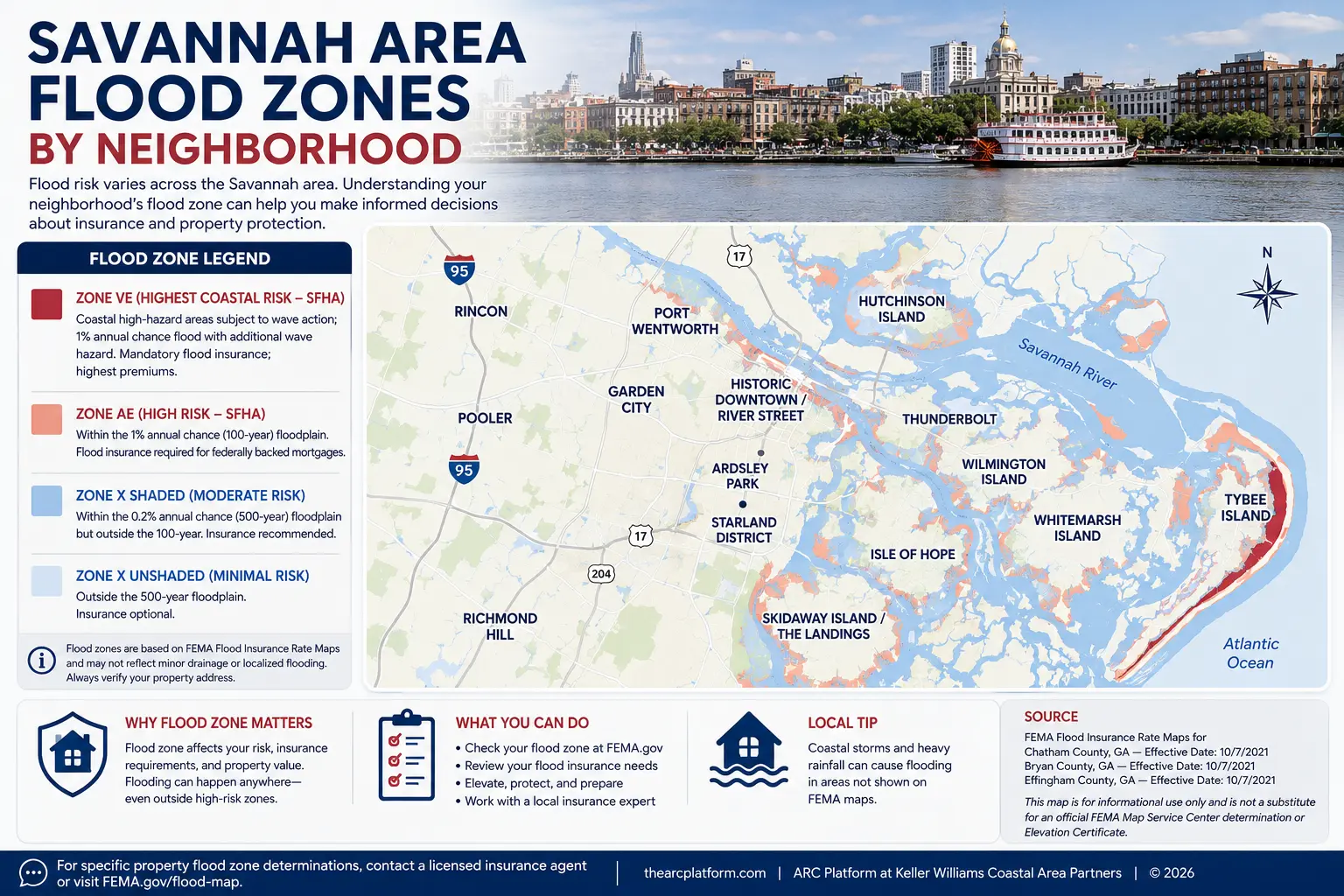

Which Savannah neighborhoods are in which flood zones?

Flood zones are determined parcel by parcel, not neighborhood by neighborhood. A single neighborhood can contain homes in two or three zones depending on elevation, drainage, proximity to marsh, proximity to a creek, and FEMA map revisions.

The table below is a practical neighborhood reference, not a legal flood determination. It describes the dominant zone for the bulk of homes in each area. Before making an offer, always look up the specific property address through the FEMA Flood Map Service Center, the Georgia Flood Map Viewer, or SAGIS for Chatham County parcel-level context. FEMA describes the Flood Map Service Center as the official public source for flood hazard information produced in support of the National Flood Insurance Program. (FEMA Flood Map Service Center) The Georgia Flood Map Viewer displays effective DFIRM flood zones statewide. (Georgia Dfirm Map) SAGIS provides standardized geospatial data for the greater Savannah and Chatham County area. (MPC)

Neighborhood / Area | Dominant zone(s) | Key risk notes |

|---|---|---|

Ardsley Park / Chatham Crescent | X, unshaded | Most of the neighborhood sits in low-risk X. Some parcels near drainage corridors or Daffin Park-adjacent areas may show shaded X. |

Historic Downtown / Landmark District | X with AE pockets | River-adjacent and low-lying parcels can show AE. Older homes may have existing elevation or grandfathered insurance history, but buyers should still quote the current risk. |

Starland District / Thomas Square | X, unshaded | Mostly outside the SFHA. Drainage and heavy-rain issues can still matter even when mapped flood risk is lower. |

Gordonston | X, unshaded | Mostly low-risk X, but buyers should still check the exact address. |

Wilmington Island | Mixed X, AE, VE | Significant parcel-by-parcel variation. Marsh-side and creek-side homes can sit in AE or VE. Interior subdivision lots are often X. |

Whitemarsh Island | Mixed X and AE | Similar pattern to Wilmington Island. Marsh-adjacent parcels are more likely to show AE. |

Isle of Hope | Mixed X, AE, VE | Riverfront and marshfront parcels can fall in AE or VE. Interior parcels are often X. |

Tybee Island | AE and VE | Substantially in SFHA. Beach-facing parcels are often VE. Flood insurance is effectively part of the ownership math. |

Skidaway Island / The Landings | Mixed X and AE | Many interior lots are X. Marsh, lagoon, and water-adjacent lots can show AE, and some premium water-exposure parcels may involve VE. |

Thunderbolt | Mixed X and AE | Marsh-side and low-lying homes are more likely to sit in AE. |

Pooler | Mostly X | Much of West Chatham’s newer suburban inventory is in X. Creek-side parcels can still show AE. |

Godley Station | X | Master-planned community inventory is largely outside the SFHA, but address-level lookup is still required. |

Berwick | X | Mostly X. Buyers should still quote optional flood insurance because premiums may be reasonable. |

Garden City | Mixed X and AE | Older parcels, canal-adjacent parcels, and low-lying areas can show AE. |

Port Wentworth | Mixed X and AE | River and creek proximity drive AE designations. |

Richmond Hill / Bryan County | Mostly X with creek-adjacent AE | Many subdivisions are X. Ogeechee River and creek-front properties can show AE or VE. |

Rincon / Effingham County | Mostly X | Most Rincon parcels are outside the SFHA, but buyers should still check the exact address. |

For buyers, the table gives you a first pass. For lenders, insurers, and closing attorneys, the address-level flood determination is what counts.

If you are comparing areas like Tybee, Wilmington, Skidaway, and Isle of Hope, do not compare only the purchase price. Compare the monthly carrying cost after taxes, insurance, flood premium, HOA fees, maintenance, and any mitigation work.

How much does flood insurance actually cost in Savannah?

Flood insurance is property-specific, so no table can replace a quote. Still, planning ranges help buyers understand the stakes before they fall in love with a house.

Use the ranges below as Savannah-area planning numbers for 2026. A licensed flood insurance agent should quote the actual property before you make an offer or price a listing.

Zone / property type | Typical Coastal Georgia annual premium range | Notes |

|---|---|---|

X, unshaded | $400 to $700, optional | Often a Preferred Risk Policy or lower-risk standard policy. Worth pricing even when not required. |

X, shaded / X500 | $500 to $900, optional | Often one of the smartest flood insurance buys: moderate mapped risk, usually lower premium than AE. |

AE, elevated at or above BFE | $900 to $2,200 | Elevation, distance to water, replacement cost, foundation type, and mitigation features matter. |

AE, below BFE or unfavorable structure factors | $2,500 to $6,000+ | Premiums can become painful if the home sits low, has prior claims, or lacks useful elevation documentation. |

VE, coastal wave hazard | $2,500 to $8,000+ | Tybee Island ocean-facing and high-exposure properties can reach the upper end or beyond. |

Source: Premium ranges are 2026 Coastal Georgia planning estimates synthesized from FEMA NFIP rate guidance under Risk Rating 2.0 and quotes from local licensed flood insurance agents. Always obtain a property-specific quote before relying on these numbers for an offer or budget.

Want the real number for your specific Savannah address?

A planning range is not a quote. ARC will connect you with a licensed Coastal Georgia flood insurance agent and walk the carrying-cost math with you before you write an offer.

FEMA’s Risk Rating 2.0 approach considers property-specific flood risk, not just the zone letter. FEMA notes that the pricing approach is now fully implemented, and NFIP materials explain that rating can account for factors such as distance to flood source, rebuilding cost, coverage choices, and property-specific characteristics. FEMA Risk Rating 2.0 (FEMA)

Why two homes on the same street can have very different premiums

Two homes on the same Wilmington Island street may both say AE, but one premium might be around $1,400 per year while another might be over $4,000.

Why?

Because the quote can change based on:

- First-floor elevation

- Distance to marsh, creek, river, or ocean

- Replacement cost

- Foundation type

- Prior flood claims

- Elevation Certificate availability

- Mechanical systems elevation

- Coverage amount and deductible

- NFIP vs private flood market

- Local CRS discount eligibility

That is why buyers should ask for the current flood policy, prior quotes, any Elevation Certificate, and any FEMA letter such as a LOMA or LOMR-F before making the final call.

CRS discounts in Savannah, Tybee, and Chatham County

The Community Rating System, or CRS, rewards communities that go beyond minimum NFIP floodplain-management standards. FEMA says CRS premium discounts range from 5% to 45% in 5% increments, depending on a community’s CRS class. FEMA Community Rating System (FEMA)

Savannah publicly states that its flood mitigation work helps reduce flood insurance premiums by 25% for property owners participating in the NFIP. City of Savannah Flood Protection Information (savannahga.gov) Tybee Island states that it is a Class 5 ISO-rated community and that property owners receive a 25% discount on flood insurance policies. Tybee Island CRS information (cityoftybee.org)

For unincorporated Chatham County, verify the current CRS class and discount with the county or your insurance agent before publishing a fixed discount number, because public-facing local references can vary by jurisdiction and update cycle. Chatham County Engineering explains that CRS classifications can result in discounted flood insurance premiums for residents. Chatham County CRS overview (Chatham County Engineering)

Two homes on the same street can cost $3,000 a year apart.

If you are weighing two flood-zone properties, ARC will price out both addresses side by side, including premium, elevation, and likely 30-year carrying cost, before either offer goes in.

I’m buying a home in a flood zone in Savannah. What should I do?

Being in a flood zone is not automatically a deal-breaker. Many of Coastal Georgia’s most desirable neighborhoods, including Tybee, Wilmington Island, Skidaway Island, Isle of Hope, Whitemarsh, and Thunderbolt, have meaningful flood exposure.

The question is not “flood zone yes or no?”

The better question is: are the carrying costs priced into what I am paying?

Here is the buyer-side framework.

1. Look up the actual flood zone

Do not rely only on the listing description. Pull the property through the FEMA Flood Map Service Center, the Georgia Flood Map Viewer, or SAGIS if the property is in Chatham County.

Listings can be wrong. Seller memory can be wrong. Old insurance documents can be outdated. The address-level map is the starting point.

2. Get a flood insurance quote before making the offer

A flood quote can take 24 to 48 hours, sometimes longer if the file is incomplete. Do this before the offer whenever possible, not halfway through due diligence.

A $700 optional Zone X policy is one conversation. A $5,200 annual AE or VE policy is another. The difference can affect your monthly payment, your loan approval, and your offer price.

3. Ask for the Elevation Certificate

An Elevation Certificate is one of the most useful documents in a flood-zone purchase. It helps clarify the relationship between the structure and the mapped flood elevation.

Many island, marsh-adjacent, and older elevated homes may already have one. If the seller has it, get it early. If they do not, ask whether the cost and timing of ordering one should be part of your offer strategy.

4. If the home is in AE or VE, negotiate

Flood insurance is not just a one-year cost. It is a long-term carrying cost.

If a property carries a $3,000 annual flood premium, that is $90,000 over a 30-year mortgage before increases, deductibles, and coverage changes. A seller may not agree to discount dollar for dollar, but the number belongs in the negotiation.

5. Ask about prior claims

Known flood damage matters. Ask direct questions. Ask for insurance history where available. Ask about repairs, drainage work, foundation work, water intrusion, and any storm-related claims.

6. Check the local CRS context

Savannah and Tybee have published CRS-related discounts. Other jurisdictions may differ. The discount can reduce NFIP premiums, but it does not eliminate risk.

Ready to run the buyer-side math on a specific home?

Send us the address. ARC will pull the FEMA zone, request an Elevation Certificate where available, get a current insurance quote, and put the full carrying-cost picture in front of you, usually within 48 hours.

ARC’s note for buyers in flood zones

Being in a flood zone is not a deal-breaker. Many of Coastal Georgia’s most desirable neighborhoods have flood exposure. The question is not whether the map shows risk. The question is whether the risk, insurance, elevation, mitigation, and resale impact are already reflected in the price.

That is the conversation ARC’s buyer-side representation walks through line by line before any offer goes in.

I’m selling a home in a Savannah flood zone. Does it hurt my sale price?

A flood zone can affect perceived value, but it does not always destroy value.

Buyers who shop on Tybee Island, Wilmington Island, Skidaway Island, Isle of Hope, or Thunderbolt often expect some flood exposure. They are not shocked by the existence of flood insurance. They are shocked by uncertainty.

That is the seller’s opportunity.

If you want to sell your home in a Coastal Georgia flood zone, your job is to make the flood question easy to understand before buyers turn it into a reason to walk away.

What helps sellers in flood-zoned properties

Have a current Elevation Certificate ready.

This reduces buyer uncertainty immediately. It also helps insurance agents quote more accurately.

Pull a flood insurance quote yourself.

If you can show a realistic quote, buyers do not have to imagine the worst-case number.

Document mitigation.

Elevated mechanicals, proper grading, French drains, flood vents, storm shutters, roof condition, drainage improvements, and prior elevation work all help buyers understand risk.

Check whether a LOMA or LOMR-F is possible.

If the property appears to sit high relative to the mapped flood elevation, it may qualify for a Letter of Map Amendment or Letter of Map Revision Based on Fill. FEMA explains that the National Flood Hazard Layer and flood map data are updated as effective data and Letters of Map Revision become valid for regulatory use. NOAA Digital Coast NFHL overview (NOAA Coastal Management)

Price the carrying cost in.

Buyers will calculate the difference between a Zone X home with a $600 optional policy and a VE home with a $5,000 required policy. Pricing realistically at the beginning usually works better than pricing aspirationally and adjusting after weeks of buyer objections.

Selling a flood-zoned home in Coastal Georgia?

ARC helps sellers prepare the Elevation Certificate, flood quote, and mitigation documentation buyers ask for, and prices the listing so the carrying cost is already baked in. That is how flood-zoned homes still sell at strong numbers.

Frequently asked questions

Which Savannah neighborhoods are in a flood zone?

Tybee Island, parts of Wilmington Island, parts of Skidaway Island, parts of Isle of Hope, marsh-adjacent parcels in Whitemarsh and Thunderbolt, and creek-adjacent parcels in Garden City and Port Wentworth sit in FEMA Special Flood Hazard Areas, most commonly AE or VE. Most of Ardsley Park, Starland, Gordonston, Pooler, Godley Station, Berwick, Richmond Hill, and Rincon sit in Zone X. Always look up the specific parcel on the FEMA Flood Map Service Center because zones can change parcel by parcel.

What is the difference between AE, X, and VE flood zones?

Zone X is minimal to moderate flood risk and does not usually require flood insurance for a federally backed loan. Zone AE is high risk, inside the 1-percent-annual-chance floodplain, with base flood elevation determined. Zone VE is high coastal risk with added wave-action hazard. AE and VE are Special Flood Hazard Areas, so flood insurance is typically required for federally backed or federally regulated mortgages.

Is flood insurance required in Savannah?

It depends on the flood zone and the loan. FEMA states that homes and businesses in high-risk flood areas with mortgages from government-backed lenders are required to have flood insurance. FEMA flood insurance overview Zone X properties generally do not have a federal flood insurance requirement, but insurance may still be recommended.

How much does flood insurance cost on Tybee Island?

Tybee Island flood insurance premiums vary by zone and Risk Rating 2.0 property factors. Typical 2026 planning ranges run from approximately $900 to $2,200 per year for elevated AE-zone homes to $2,500 to $8,000+ per year for VE-zone ocean-facing properties. Tybee Island states that it is a Class 5 ISO-rated CRS community, which qualifies property owners for a 25% flood insurance premium discount on NFIP policies. Tybee Island NFIP information (cityoftybee.org)

Should I buy flood insurance in Zone X in Savannah?

Yes, it is worth pricing. It is usually not required by the lender, but it may be inexpensive compared with the financial risk of flood damage. FEMA’s Flood Map Service Center notes that even if a home is not in a high-risk zone, homeowners may still need flood insurance because most homeowners insurance does not cover flood damage. FEMA Flood Map Service Center (FEMA Flood Map Service Center)

Can I get a property removed from a flood zone in Savannah?

Sometimes. If a property is on naturally high ground but mapped into a Special Flood Hazard Area, a Letter of Map Amendment may remove the SFHA designation. A Letter of Map Revision Based on Fill may apply after certain fill or elevation work. Both usually require elevation or engineering documentation. The process can take months, so it should be started early if it matters to a sale or refinance.

Closing thoughts and next steps

Flood zones are not what they used to be. Risk Rating 2.0 made every premium property-specific. Climate-adjusted risk models sometimes disagree with the official FEMA maps. The Community Rating System rewards municipalities, and indirectly homeowners, that go beyond the federal minimum. FEMA maps themselves are revised periodically. What was Zone X years ago may sit near a revised AE boundary today.

What that means in practice is simple: the zone code is the starting point, not the answer.

Two homes in the same Wilmington Island AE pocket can have radically different insurance bills. A Tybee VE-zoned home with the right elevation documentation may carry better than a marsh-side AE home without one. A creek-adjacent Garden City parcel may quietly be Zone X. The map will not tell you all of that. The quote will.

When you are ready for that conversation, whether you are buying, selling, or just trying to make sense of a renewal, ARC is here. If you are a service member or veteran, see our Coastal Georgia military relocation help for PCS timing, VA loan, and flood-zone guidance.

The math comes before the decision. The decision comes before the offer. That order matters, and we will walk it with you.

Looking at a flood-zoned home? Selling one?

Either way, the math should come before the decision. ARC will walk the flood zone, insurance quote, elevation documents, resale impact, and offer strategy with you, line by line, before anything is signed.

Buying in Coastal Georgia?

We work zone, insurance, and carrying cost into your offer strategy before you commit.

Start with buyer-side rep →Selling a flood-zoned home?

We prepare the flood paperwork buyers want, then price the carrying cost in so the listing actually closes.

Get a home valuation →Distressed sale or short timeline? Ask about ARC’s Private Options, a confidential alternative when a traditional listing is not the right fit.

Talk with ARC today · Phone: +1-912-351-8935 · Email: info@thearcplatform.com · Start here

Join The Discussion