- Why VA almost always wins for eligible military buyers

- Side-by-side comparison: VA vs. FHA vs. Conventional

- When FHA actually makes sense

- When conventional actually makes sense

- The hidden cost most calculators miss: VA appraisal strictness

- Coastal GA worked example: $350K Pooler purchase compared

- Frequently asked questions

- Ready to compare your VA, FHA & conventional options?

- For most eligible Coastal Georgia military buyers, VA wins: 0% down, no monthly PMI, and a funding fee waived for many service-connected-disability veterans.

- FHA is the backup when VA entitlement is tied up or a non-spouse co-borrower is needed.

- Conventional can win with strong credit, 20% down, or a seller who values appraisal certainty.

- On a $350K Pooler example, VA preserves the most cash in the first five years.

By: Alex Rodino | U.S. Army Captain (vet.) | GA Real Estate License #443565 | 7-minute read | Updated June 2026 | Reviewed by Alex Rodino

For Coastal Georgia military buyers, VA almost always wins on paper (0% down, no PMI, lowest typical rates). The real decision is not just VA loan vs FHA vs conventional military financing in general. It is whether VA wins for this home, this seller, this appraisal risk, and this timeline. VA usually gives eligible buyers the strongest cash-to-close advantage, especially around Fort Stewart, Hunter AAF, Pooler, Richmond Hill, Hinesville, and Savannah. But FHA or conventional can make sense when entitlement is tied up, a non-spouse co-borrower is needed, or a seller is nervous about VA appraisal repairs. We start with VA, then test the exceptions.

If you are still early in the PCS process, pair this comparison with the Hunter AAF and Fort Stewart buyer’s guide before choosing a loan lane.

Why VA almost always wins for eligible military buyers

In brief: VA usually wins because it combines 0% down, no monthly PMI, competitive terms, and a funding-fee waiver for many service-connected-disability veterans.

On a $350,000 Coastal Georgia purchase, a VA buyer using first-time entitlement can bring $0 down, while FHA requires $12,250 down and a 5% conventional loan requires $17,500 down.

VA-backed purchase loans are designed for eligible service members, veterans, and certain surviving spouses. VA does not lend the money in most purchase transactions. It guarantees part of the loan, which lowers lender risk and can create better borrower terms through the official VA-backed loan structure.

The biggest VA advantages are simple:

- 0% down for many eligible borrowers

- No monthly private mortgage insurance

- Competitive interest-rate pricing

- Limited allowable fees

- Lifetime benefit that can be used more than once

- Funding fee waived for qualifying service-connected-disability veterans

The funding fee matters, but it is often less expensive than years of FHA MIP or conventional PMI. VA.gov confirms the purchase funding fee for first use with less than 5% down is 2.15% of the loan amount, and that qualifying disability compensation status can remove the fee entirely. For a deeper breakdown, see our VA funding fee walkthrough.

Alex’s note: As a veteran-led real estate team, we do not treat VA financing as a generic checkbox. We look at the mission, the market, the seller, and the property condition before telling a military buyer which loan actually wins.

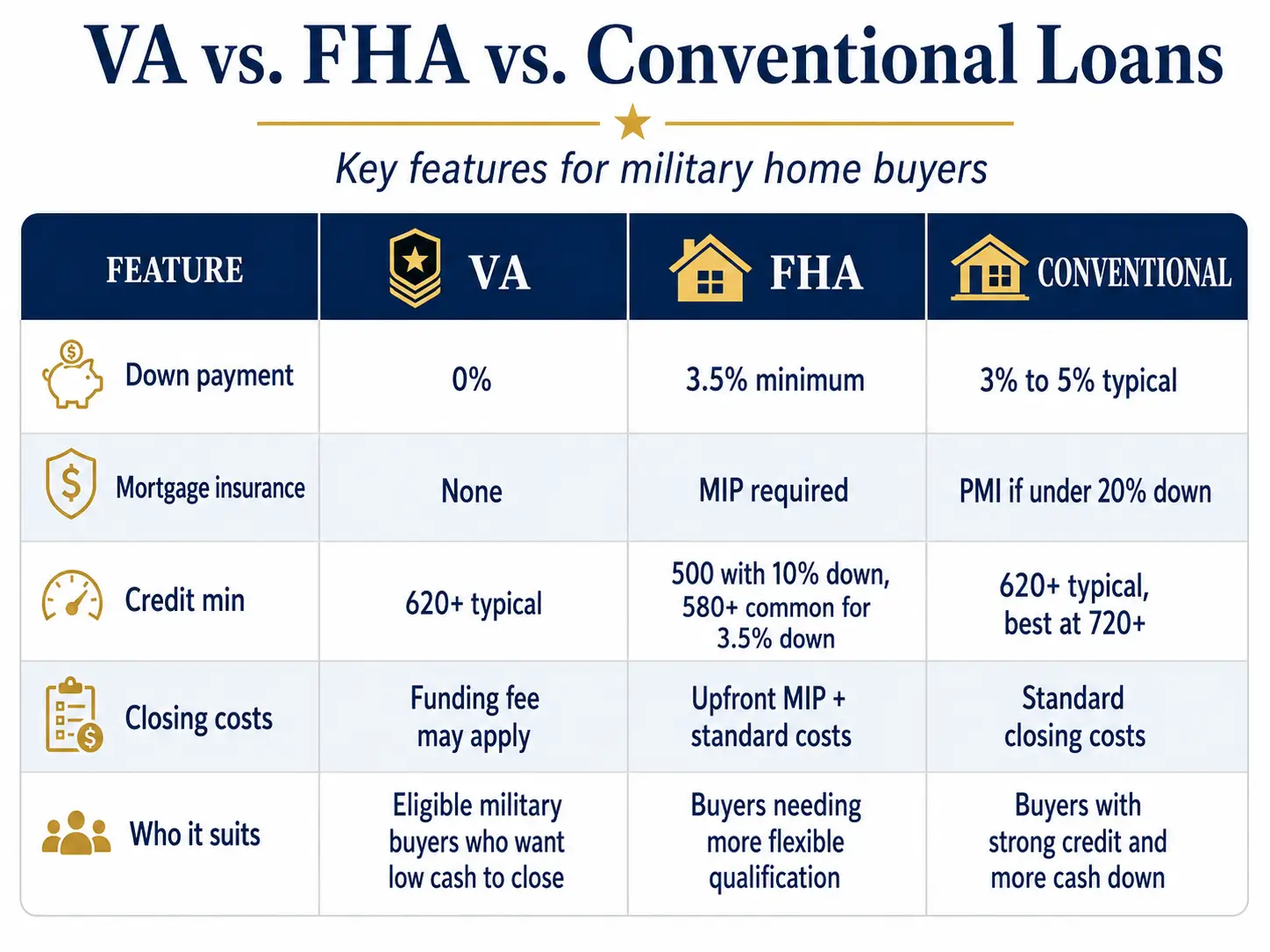

Side-by-side comparison: VA vs. FHA vs. Conventional

In brief: VA is strongest for eligible military buyers with limited cash to close. FHA is a backup tool for specific borrower situations, while conventional is strongest for buyers with excellent credit, larger down payments, or sellers who want appraisal simplicity.

Feature | VA | FHA | Conventional |

Minimum down payment | 0% for many eligible buyers through VA-backed purchase loans | As low as 3.5% through HUD, with higher down required for lower credit tiers | As low as 3% for eligible programs such as Fannie Mae 97% LTV options or Freddie Mac Home Possible, often 5% otherwise |

Mortgage insurance | No monthly PMI, funding fee may apply | Upfront MIP plus annual MIP; HUD’s current schedule shows 1.75% upfront MIP and 55 bps annual MIP for many low-down-payment 30-year loans | PMI usually applies below 20% down; CFPB confirms 20% down avoids PMI on conventional loans |

Credit profile | No single VA-set credit score, lender overlays apply | More flexible for thin or recovering credit, but lender overlays still apply | Often stronger with higher credit, lower debt ratios, and more cash reserves |

Closing costs | VA funding fee may be financed, but most other closing costs cannot be rolled into a purchase loan | Upfront MIP can often be financed | Standard lender, title, escrow, prepaid, and PMI costs if applicable |

Best fit | Eligible military buyer who wants to preserve cash | Buyer who needs FHA flexibility or has a VA-specific obstacle | Buyer with strong credit, 20% down, or a seller situation where conventional terms improve competitiveness |

When FHA actually makes sense

In brief: FHA is not usually the first choice for a VA-eligible military buyer, but it can solve problems VA does not solve cleanly.

FHA’s 3.5% minimum down payment can beat conventional cash-to-close, but it usually cannot beat VA’s 0% down for an eligible buyer.

The first FHA scenario is a co-borrower issue. VA joint loans work best with a spouse or another eligible veteran. If the buyer needs a non-spouse, non-veteran co-borrower to qualify, FHA may be simpler.

The second scenario is entitlement. A buyer who still owns another VA-financed property, or who has partial entitlement tied up, may need money down to use VA again. Sometimes FHA becomes easier than forcing a VA structure that does not fit the current entitlement picture.

The third scenario is lender fit. FHA can be more forgiving where credit is thinner or still recovering. HUD’s own FHA materials position the program around low down payments, low closing costs, and easier credit qualifying. That does not mean every buyer qualifies, and it does not mean FHA is cheaper. It means FHA belongs in the toolbox when the VA lane is blocked.

When conventional actually makes sense

In brief: Conventional can win when the buyer has strong credit, a real 20% down payment, and a seller who values appraisal certainty over the buyer’s VA advantages.

A 20% down conventional buyer can avoid PMI entirely, which CFPB confirms is a key difference from low-down-payment conventional loans.

Conventional is strongest when the military buyer has enough cash that preserving down payment is not the priority. If you can put 20% down, avoid PMI, avoid the VA funding fee, and still keep emergency reserves, conventional may be competitive.

Conventional can also matter in a hot seller situation. In Pooler, Richmond Hill, and parts of Savannah where clean homes move quickly, some sellers believe conventional appraisals create fewer repair surprises than VA appraisals. That seller belief is not always fair, but it affects negotiation.

This is where ARC differs from national PCS Realtor aggregators or broad military-buyer sites. Those platforms may match you with someone in a database. We are veteran-led and Coastal Georgia-specific, so we can help structure the actual offer around the seller, the appraisal risk, the commute, and the local resale picture.

The hidden cost most calculators miss: VA appraisal strictness

In brief: A VA loan can be cheaper on paper but still lose the deal if the property has repair issues that trigger seller resistance.

One required VA repair can matter more than a lower monthly payment if it causes the seller to choose another offer.

VA appraisals do more than confirm value. They also review Minimum Property Requirements, or MPRs. The Federal Register summarizes VA’s MPR framework and lists property topics such as access, utilities, water supply, sanitary facilities, hazards, defective conditions, roof covering, crawl spaces, and wood-destroying insects or fungus in VA’s minimum property requirements.

In Coastal Georgia, this matters because moisture, crawl spaces, roof age, prior termite treatment, wood rot, and older systems are common in parts of the housing stock. A VA-savvy agent should spot obvious issues before the offer is written, not after the appraisal comes back.

That is why we review VA MPR issues on Coastal Georgia homes with buyers before they fall in love with a house. The solution is not to avoid VA. The solution is to write a VA offer that is clean, specific, and credible.

Strong VA offer language can include proof of funds for closing costs, clear appraisal timing, a practical repair negotiation plan, and seller education that separates myth from actual VA requirements.

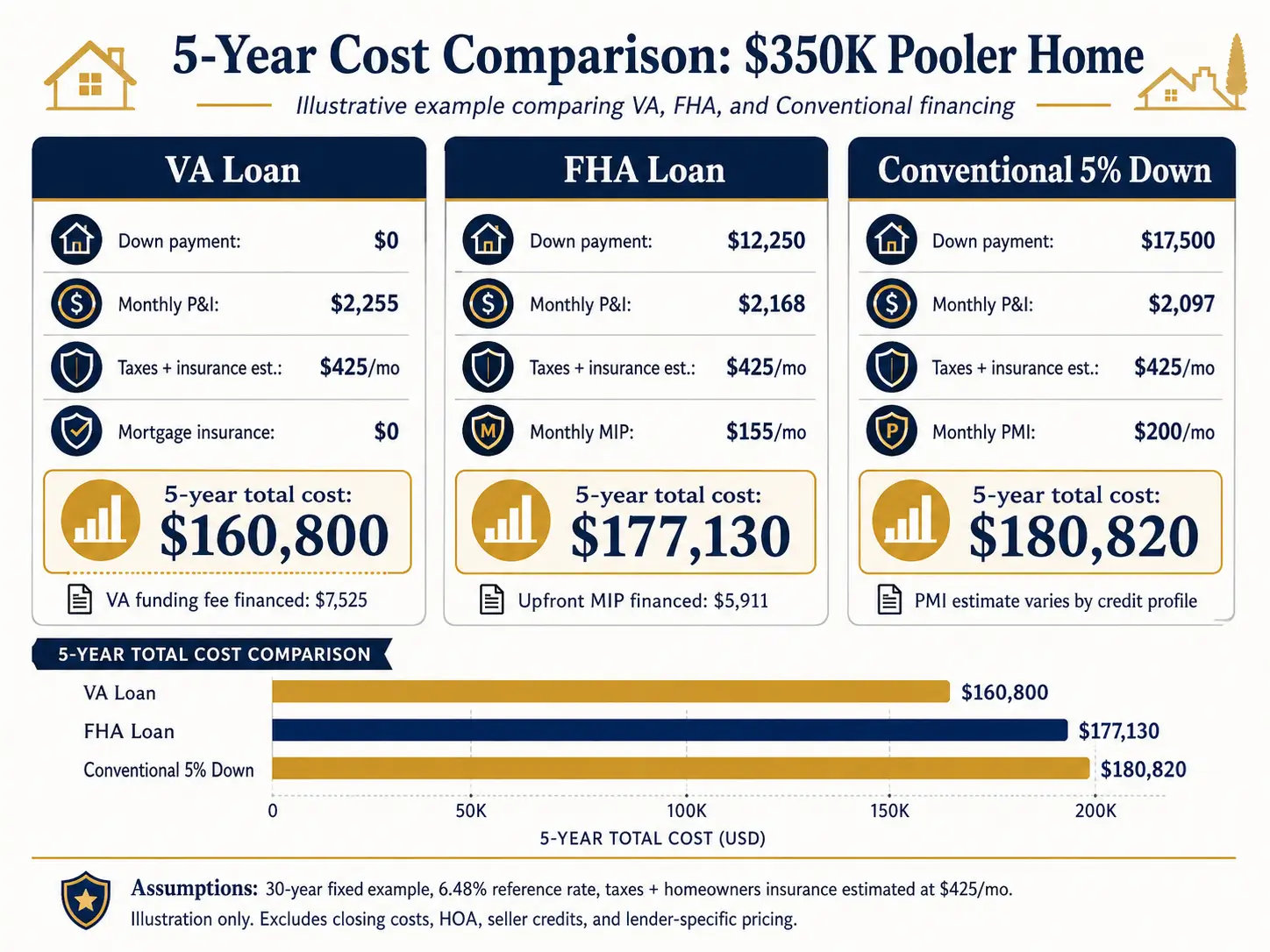

Coastal GA worked example: $350K Pooler purchase compared

In brief: On this $350,000 Pooler example, VA has the lowest cash-to-close profile, while FHA and conventional require more upfront cash and monthly mortgage-insurance assumptions.

A first-use VA funding fee on a $350,000 purchase with 0% down is $7,525, because VA’s current chart shows a 2.15% fee for first use with less than 5% down.

Assumptions for illustration only: $350,000 purchase price, 30-year fixed loan, Freddie Mac’s 6.48% national 30-year average as a reference point, and no tax, insurance, HOA, rate-lock, lender-credit, discount-point, or seller-credit adjustment. This is not a Loan Estimate.

Loan option | Upfront cash for down payment | Financed fee or insurance | Starting monthly principal, interest, and MI estimate | 5-year cash flow estimate |

VA first use, 0% down | $0 | $7,525 VA funding fee financed | About $2,255 principal and interest, before taxes and insurance | About $135,306 |

FHA, 3.5% down | $12,250 | About $5,911 upfront MIP financed | About $2,323 including estimated starting annual MIP | About $151,600 |

Conventional, 5% down | $17,500 | PMI varies by credit, insurer, and lender | About $2,297 using a $200 PMI illustration | About $155,335 |

The lesson is not that every VA loan is automatically cheaper in every case. The lesson is that VA often preserves the most cash in the first five years, especially when the buyer would otherwise pay monthly FHA MIP or conventional PMI.

For the VA buyer, the funding fee adds roughly $47 per month to the loan payment at the illustrated rate. That is usually less painful than a $150 to $250 monthly PMI range, but PMI is lender-specific and should be quoted directly. Seller-paid costs can also change the math, so review VA loan seller concessions before comparing final offers.

Frequently asked questions

In brief: VA is usually the best starting point for eligible Coastal Georgia military buyers, but FHA and conventional deserve a deal-specific check before you commit.

Is a VA loan always better than FHA or conventional for military buyers?

For most Coastal Georgia military buyers, yes. VA wins on 0% down, no PMI, competitive rates, and a funding fee waived for many service-connected-disability veterans. But in three specific scenarios, entitlement maxed, non-spouse co-borrower needed, or a hot Pooler or Richmond Hill listing where sellers prefer conventional offers, FHA or conventional may actually win. Run the deal-specific math before assuming VA is best.

When should a military buyer choose an FHA loan over a VA loan?

FHA fits when you have already tied up your VA entitlement, typically because you own another VA-financed home, or when you need a non-spouse co-borrower on the loan. FHA’s 3.5% minimum down payment and flexible credit framework can also help buyers whose credit profile a VA lender will not accept. That is not the common path, but it is possible.

When should a military buyer choose a conventional loan over a VA loan?

Conventional wins when you have strong credit, a 20% down payment available, and want to avoid the VA funding fee entirely. In a hot Coastal Georgia market, especially Pooler or Richmond Hill, sellers occasionally favor conventional offers because conventional appraisals do not enforce VA Minimum Property Requirements. Conventional can also feel simpler to sellers who have outdated assumptions about VA financing.

Do VA appraisals affect my offer's competitiveness in a hot Coastal Georgia market?

Sometimes. VA appraisals enforce Minimum Property Requirements tied to safety, sanitation, structural soundness, and property acceptability. On a hot Pooler or Richmond Hill listing, sellers may prefer conventional offers because of appraisal certainty. A VA-savvy Coastal Georgia agent can often reduce this bias with clean terms, education, and a repair strategy before the offer is presented.

Does the VA funding fee make conventional cheaper overall?

Not usually. Even with the funding fee rolled in, VA often beats conventional on early cash flow because VA has no monthly PMI. On the $350,000 example above, the first-use VA funding fee adds about $47 per month at the illustrated rate. Conventional may win when the buyer has 20% down and can avoid PMI and the VA funding fee while still keeping reserves.

Ready to compare your actual VA, FHA, and conventional options?

The right loan is the one that wins both the math and the negotiation for your specific Coastal Georgia home.

Before you choose VA, FHA, or conventional, we can help you pressure-test the loan against the actual property, commute, seller, and appraisal risk. The goal is not to force every military buyer into VA — it is to protect your cash, your timeline, and your ability to win the right home.

Schedule a free 30-minute call with ARC. We will walk through your PCS timeline, target area, likely loan structure, and offer strategy before you spend money on inspections or lock into the wrong financing path.

ARC is led by Alex Rodino, U.S. Army Captain (veteran) and licensed Georgia Realtor®, License #443565. The ARC Platform is affiliated with Keller Williams Coastal Area Partners. This article is for informational purposes only and is not mortgage, legal, tax, or financial advice. Loan terms, rates, eligibility, seller concessions, and approval outcomes vary by borrower, lender, property, and market conditions. Equal Housing Opportunity.

Join The Discussion