Reviewed by Alex Rodino

If you’re wondering how to choose VA loan lender military buyers can actually trust, the answer is usually not the lender with the flashiest advertisement or the lowest headline rate. In our experience helping service members and veterans across Coastal Georgia, the lenders that consistently create smoother transactions are the ones with strong VA execution, in-house appraisal authority, and genuine military expertise. Buyers relocating through our Coastal Georgia military relocation help program often discover that lender quality affects timelines, appraisal outcomes, and even whether a contract survives a competitive market.

For buyers starting their search, we also recommend reviewing the Hunter AAF and Fort Stewart buyer’s guide to understand the local housing landscape before choosing financing partners.

Why advertised VA rates are misleading, and what to actually compare

In brief: Most major VA lenders are usually very close on rate. Execution quality, fees, and military-specific expertise create the biggest differences.

Many military buyers begin by comparing advertised rates. The problem is that advertised rates rarely tell the whole story. Rates change frequently, and lenders often structure pricing differently through discount points, lender credits, and closing costs.

A VA loan lender is a financial institution approved to originate and process loans backed by the U.S. Department of Veterans Affairs. While the loan guarantee is provided through the VA, the actual lending experience varies significantly by lender.

In many cases, competing VA lenders are separated by only a fraction of a percentage point. What creates major differences is how efficiently they process files, handle appraisals, communicate during PCS moves, and structure fees.

Alex’s note: As a veteran and Realtor working with military families throughout Coastal Georgia, we’ve seen buyers lose homes while chasing slightly lower rates that ultimately produced slower closings and more underwriting friction.

National military-homebuyer websites often focus on lender rankings. We believe local execution matters more. A lender that understands Coastal Georgia inventory, VA appraisals, and military timelines can create a much smoother experience than a national lead-generation platform.

The same-day Loan Estimate test (run this with 3 lenders)

In brief: Request three Loan Estimates on the same day and compare fees, not marketing claims.

The fastest way to compare lenders is to obtain Loan Estimates from at least three lenders on the same day.

Same-day quotes eliminate market movement and create a true apples-to-apples comparison.

Review these items carefully:

- Interest rate

• Discount points

• Section A Origination Charges

• Total lender fees

• Estimated cash to close

If you’re still early in the process, review our guide to the VA loan pre-approval process before requesting quotes.

Comparison Item | Why It Matters |

Interest Rate | Affects monthly payment |

Discount Points | May reduce rate but increase upfront costs |

Origination Charges | Direct lender fees |

Processing Fees | Potential area for fee inflation |

Underwriting Fees | Compare across lenders |

The lender with the best combination of pricing, responsiveness, and VA expertise often provides the strongest overall value.

SAR appraisal authority, the speed test most buyers miss

In brief: SAR authority can eliminate weeks of delay during the VA appraisal process.

A Staff Appraisal Reviewer (SAR) is an individual authorized to review and approve VA appraisal reports on behalf of the VA.

For military buyers facing PCS deadlines, this matters enormously.

Lenders with SAR authority can often move appraisal files through the system more efficiently than lenders relying entirely on outside review channels.

Ask every lender:

“Do you have in-house SAR authority for VA loans?”

Many buyers never ask this question. Yet it may have a bigger impact on your timeline than a tiny difference in interest rate.

When homes are moving quickly in Pooler, Richmond Hill, Savannah, and surrounding communities, losing two or three weeks can create serious challenges.

How they handle the Tidewater Initiative

In brief: An experienced lender should have a clear Tidewater response process before issues arise.

The VA Tidewater Initiative gives parties an opportunity to provide additional comparable sales when an appraiser believes a property may not support the contract value.

This is one of the most misunderstood aspects of VA financing.

When a lender and agent understand Tidewater procedures, they can coordinate quickly, gather stronger comparable sales, and potentially prevent a low appraisal from derailing the transaction.

In markets where inventory shifts rapidly, comparable sales data may not always tell the complete story. That’s especially true in growing areas where newer homes are entering the market.

Ask lenders:

- What is your Tidewater process?

• Who communicates with the agent?

• How quickly do you respond when Tidewater is triggered?

• How many VA loans do you close annually?

The answers reveal whether VA lending is a core competency or simply an occasional product.

The 1% Origination Cap, and how to spot disguised fees

In brief: Compare total lender fees, not just advertised rates.

The VA limits lender origination charges to 1% of the loan amount under VA fee rules.

However, buyers should still carefully review fee structures.

Common fee categories include:

- Origination fee

• Processing fee

• Underwriting fee

• Administrative fee

• Document preparation fee

The key question is not whether a fee exists. The key question is whether total charges remain reasonable when viewed together.

When reviewing costs, also understand how the funding fee affects overall financing. Our VA funding fee walkthrough explains current rules and exemptions.

Alex’s note: We encourage buyers to compare total lender costs on the same day rather than focusing on one line item in isolation.

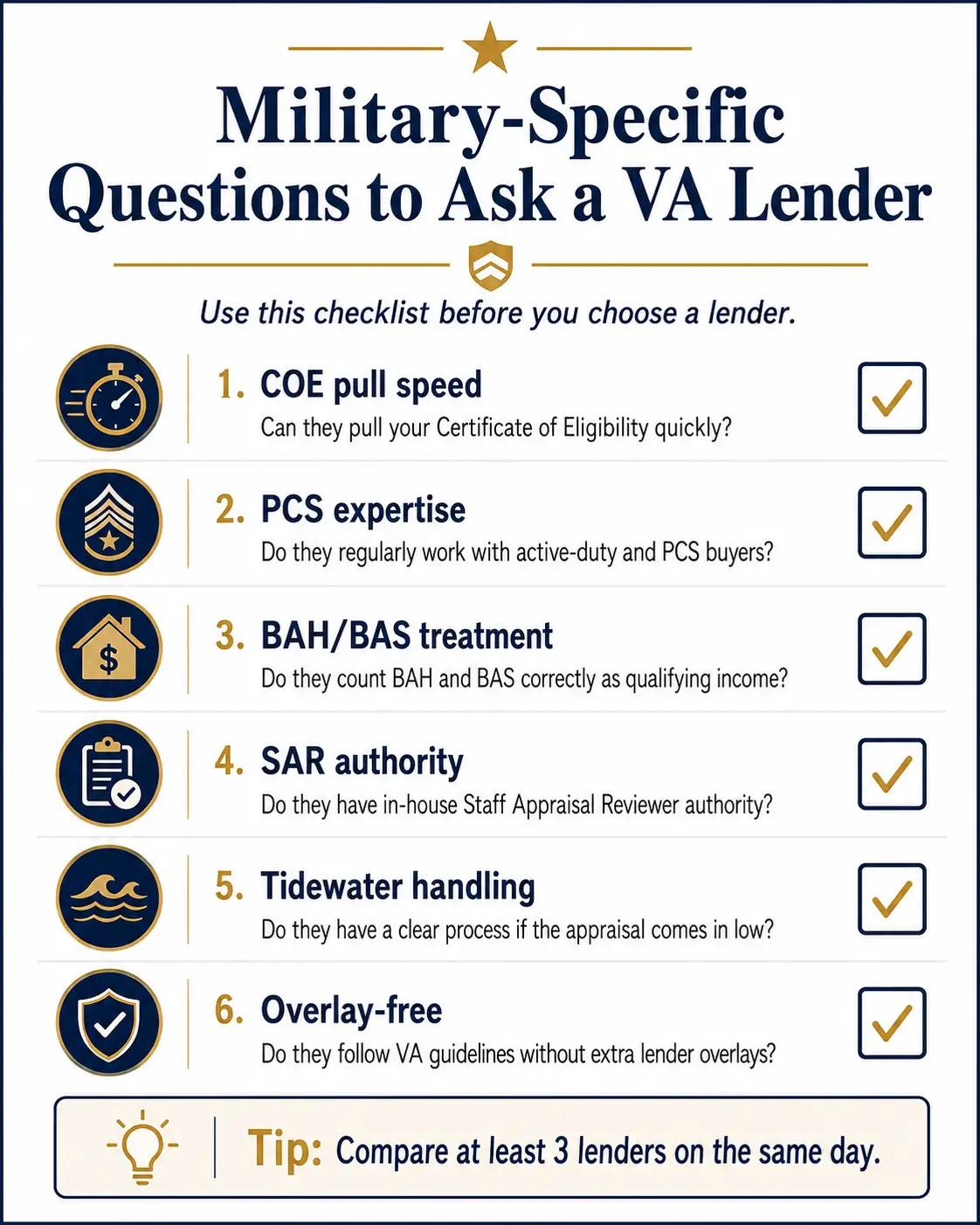

Military-specific questions every Coastal GA buyer should ask

In brief: Ask about COE speed, military income treatment, deployment experience, and VA contract protections.

Here are the questions we recommend every military buyer ask.

How fast can you pull my COE?

Experienced VA lenders can often obtain eligibility verification rapidly through approved systems.

If you need help understanding eligibility documentation, review our VA Certificate of Eligibility walkthrough.

Do you have a dedicated military or PCS team?

Military buyers face unique timing, deployment, and relocation issues. A lender that routinely works with service members generally understands those challenges better.

How do you treat BAH and BAS?

Basic Allowance for Housing and Basic Allowance for Subsistence are important components of military compensation.

A lender experienced with military borrowers should clearly explain how these allowances are incorporated into qualifying income.

Buyers relocating to Coastal Georgia should also review current housing allowances in our guide to 2026 BAH at Hunter AAF and Fort Stewart.

Do you ensure the VA escape clause is included?

The VA escape clause provides important protections for eligible buyers. Your lender and agent should be familiar with the requirement and coordinate appropriately.

Avoid lender overlays, they limit who qualifies

In brief: Some lenders add stricter requirements than the VA itself requires.

A lender overlay is an internal guideline imposed by the lender beyond standard VA requirements.

One common example involves minimum credit-score requirements.

While lenders establish their own underwriting standards, some are significantly more restrictive than others.

Ask directly:

“Do you follow standard VA guidelines, or do you have overlays?”

This simple question can save time, frustration, and unnecessary loan denials.

If one lender says no, another lender with fewer overlays may still approve the same borrower.

Frequently Asked Questions

What's the most important thing to look for in a VA loan lender?

SAR (Staff Appraisal Reviewer) authority is the single most under-appreciated criterion. Lenders with SAR authority can approve VA appraisals in-house, avoiding delays that can jeopardize PCS timelines and competitive offers. Before discussing rates, ask whether the lender has SAR authority and how frequently they close VA loans.

Why should I get Loan Estimates from multiple VA lenders on the same day?

VA loan rates can change from day to day. Obtaining Loan Estimates on the same day allows you to isolate lender fees, discount points, and origination charges without market movement distorting the comparison. This creates a much more accurate evaluation of lender value.

What is the Tidewater Initiative on a VA appraisal?

The Tidewater Initiative allows an appraiser to indicate that a property may not support the contract value before the final appraisal is issued. This creates an opportunity to submit additional comparable sales and supporting market information before the valuation becomes final.

What is a VA lender overlay and why does it matter?

A lender overlay is an internal lending requirement that exceeds standard VA guidelines. Examples include higher credit-score thresholds or stricter debt-to-income requirements. These overlays can prevent otherwise eligible military borrowers from qualifying with a particular lender.

Does it matter whether my VA lender treats BAH and BAS as income?

Yes. BAH and BAS are significant components of military compensation. The way a lender evaluates those allowances can affect qualifying income, purchasing power, and ultimately the range of homes available to you in Coastal Georgia.

Ready to Talk Through Your Options?

Choosing the right VA lender is only one part of a successful military move. We help service members and veterans evaluate neighborhoods, timelines, financing strategies, and relocation logistics throughout Coastal Georgia.

If you’re preparing for a PCS move, separation from service, retirement, or your first VA home purchase, our team is happy to help.

Schedule a free 30-minute consultation through our Coastal Georgia military relocation help page. We’ll walk through your timeline, answer questions, and help you build a smart plan before you commit to a lender or a home.

Keller Williams Realty Coastal Area Partners. This article is provided for informational purposes only and should not be considered legal, tax, lending, or financial advice. Buyers should verify all financing terms directly with qualified lenders and advisors. Equal Housing Opportunity.

Join The Discussion