VA Loan Pre-Approval for Coastal Georgia Military Buyers: Documents, Timeline, and the VA Escape Clause

VA pre-approval isn’t just a paperwork formality, it’s when the VA Escape Clause gets baked into your contract, the clause that lets you walk away with your earnest money refunded if the VA appraisal comes in below price. For Coastal Georgia military buyers, especially those shopping near Hunter Army Airfield, Fort Stewart, Pooler, Richmond Hill, Hinesville, and Savannah, the right pre-approval letter can strengthen your offer before you tour the first home. The goal is simple: verify eligibility, document income, confirm buying power, and make sure your protection language is ready before you write. As a veteran-led real estate practice, we want military buyers to understand the paperwork before the pressure starts.

If you are still mapping duty-station logistics, start with the Hunter AAF and Fort Stewart buyer’s guide, then use this pre-approval checklist before submitting offers.

What VA pre-approval actually does for your offer

In brief: VA pre-approval tells a seller that your lender has reviewed your basic eligibility, finances, and loan readiness. It is stronger than a casual estimate, but it is still not a final loan approval.

VA loan pre-approval is a lender’s preliminary review of whether a military borrower appears qualified to use VA financing for a home purchase. In plain English, it connects your service eligibility, income, credit, debts, and available cash into one offer-ready letter. The CFPB explains that a preapproval letter tells sellers you are likely to obtain financing, while also noting it is not a guaranteed loan offer.

In Coastal Georgia, that distinction matters. Sellers in Pooler, Richmond Hill, Savannah, and Hinesville see plenty of VA-financed offers. A clean pre-approval letter from a VA-savvy lender can help show that your file has been reviewed, not guessed.

Pre-qualification is lighter. The CFPB notes that some lenders issue prequalification based on unverified information while others reserve preapproval for verified information. For a competitive listing, we want the stronger version.

National PCS-realtor aggregators can match you with a name in a database. Our advantage is different: veteran-led, Coastal Georgia-specific guidance that connects your VA financing, PCS timing, neighborhood search, and contract protections in one local plan.

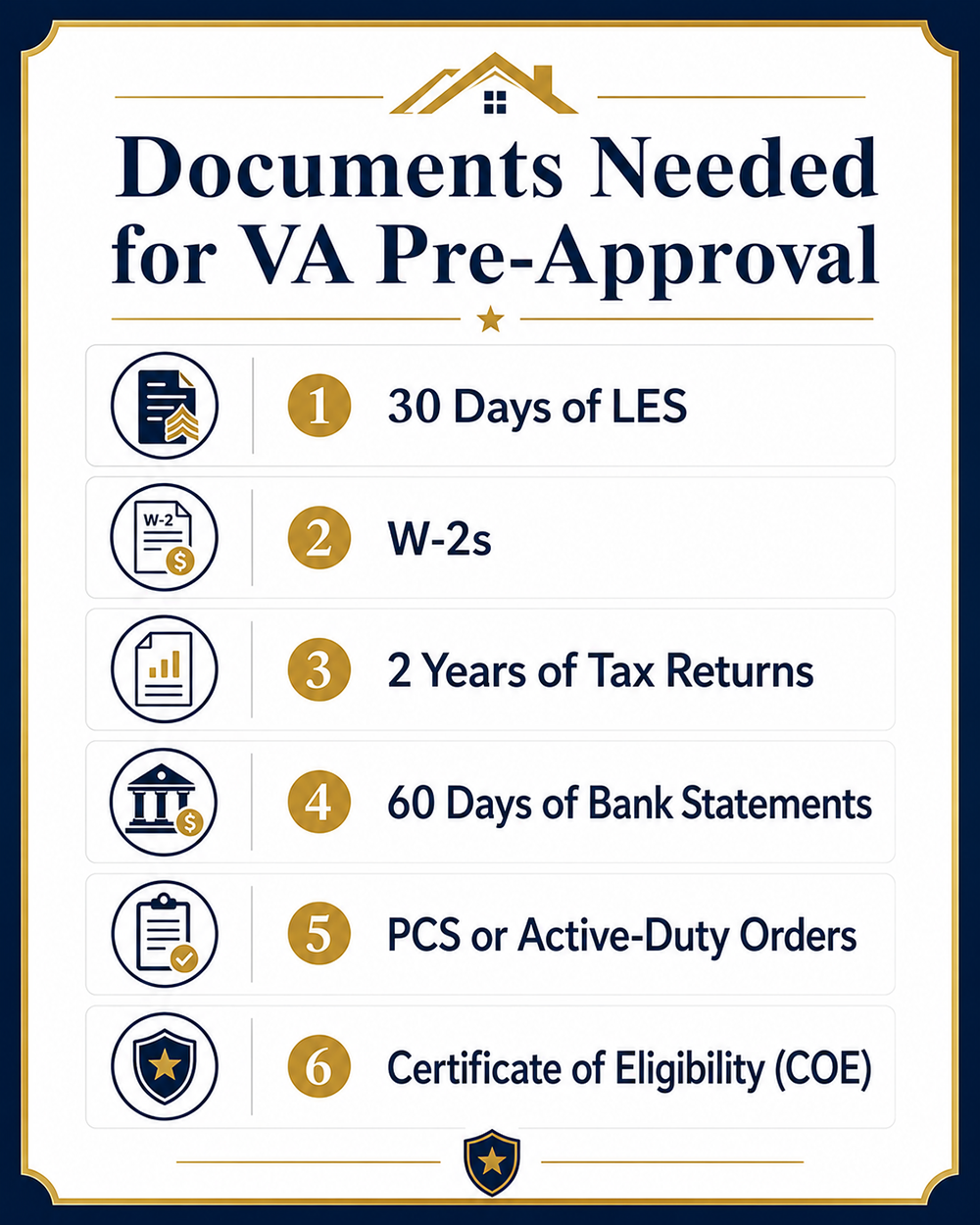

Documents you need to prep before contacting a lender

In brief: Have your LES, tax documents, bank statements, PCS orders, and COE path ready before the first lender call. The faster your file is complete, the faster the lender can issue a useful letter.

Most prepared VA buyers should gather 30 days of LES, 2 years of tax documents, and 60 days of bank statements before lender review.

The VA Buyer’s Guide says lenders commonly require loan documents such as a Certificate of Eligibility, LES, W-2 forms, income tax returns, and bank statements. Your exact lender checklist can vary, but we recommend having these items ready before you start:

Last 30 days of Leave and Earnings Statements

W-2s and tax returns from the last 2 years

Bank statements from the last 60 days

Active-duty orders if a PCS is imminent

Government ID and Social Security number for lender verification

Certificate of Eligibility, or enough service information for the lender to pull it

The COE proves to the lender that your service history supports VA loan eligibility. VA.gov states that VA Form 26-1880 is used to apply for a VA home loan Certificate of Eligibility, and VA’s online status page lets applicants upload documents and download an approved COE.

If you want the COE step explained separately, use our VA Certificate of Eligibility walkthrough before you apply.

The 4-step pre-approval workflow with timing

In brief: A complete file can often move from application to pre-approval in 7 to 14 days. The biggest delays usually come from missing documents, unresolved COE questions, or lender confusion around military income.

A realistic VA pre-approval timeline is 7 to 14 days when your paperwork is complete, with COE follow-up sometimes adding time if VA must manually review the request.

VA says its goal for contacting COE applicants is an average of 5 business days when a COE request needs review. That does not mean your full mortgage is approved in 5 days. It means a clean COE process can support a faster pre-approval file.

Alex’s note: Do not wait until you find the house to organize documents. In a PCS move, the best buyer is usually the one who can submit a strong offer quickly and calmly.

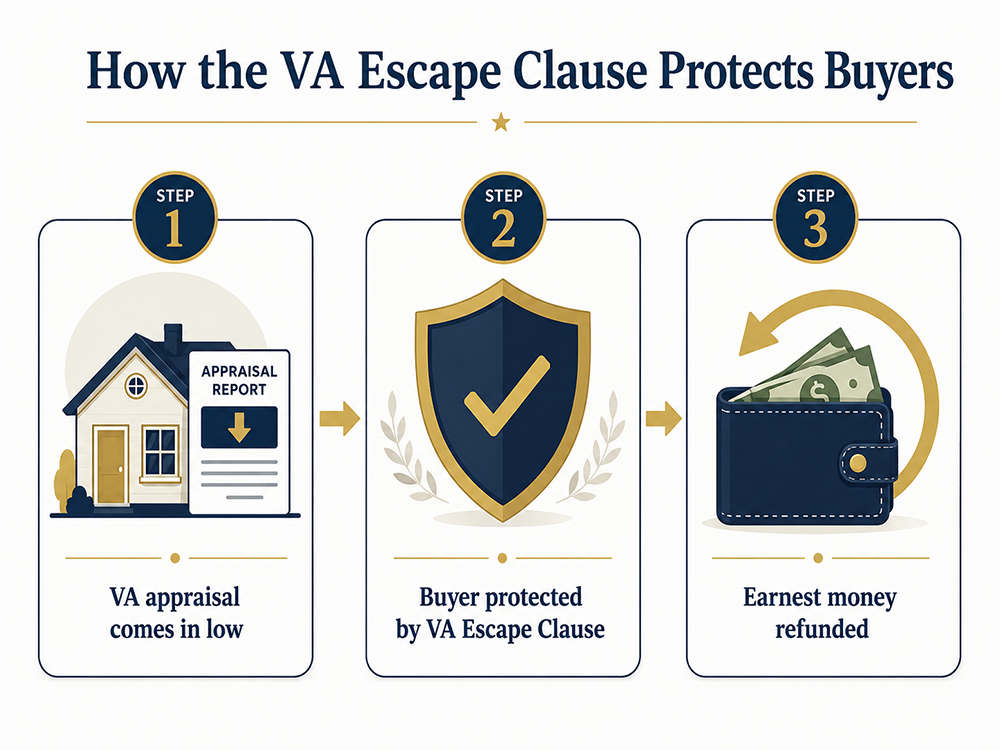

The VA Escape Clause: the most overlooked protection

In brief: The VA Escape Clause protects VA buyers if the VA appraisal comes in below the contract price. It must be in the contract for VA-guaranteed purchase loans when required.

The VA Escape Clause can protect your earnest money deposit if the VA’s reasonable value is lower than the purchase price.

This is the part too many buyers miss. The VA states that the Escape Clause must always be included in a VA home loan purchase contract, and that it gives buyers options if the contract price exceeds VA’s reasonable value.

VA-required language says:

“It is expressly agreed that, notwithstanding any other provisions of this contract, the purchaser shall not incur any penalty by forfeiture of earnest money or otherwise be obligated to complete the purchase of the property described herein, if the contract purchase price or cost exceeds the reasonable value of the property established by the Department of Veterans Affairs. The purchaser shall, however, have the privilege and option of proceeding with the consummation of this contract without regard to the amount of the reasonable value established by the Department of Veterans Affairs.”

That clause is why pre-approval and contract strategy belong together. If the appraisal is low, the VA Buyer’s Guide says the buyer may have options such as reconsideration of value, renegotiation, bringing cash to closing, or choosing not to proceed under the Escape Clause section.

In Coastal Georgia, this matters in homes where condition, concessions, and comparable sales can move quickly. Before you waive, modify, or misunderstand any protection, review how VA loan seller concessions and VA MPR issues can affect your offer.

Alex’s note: Skipping the Escape Clause is the single most expensive mistake we see VA buyers risk. The clause is not a formality. It is a real protection tied to your appraisal.

How VA-savvy lenders treat military-specific income: BAH, BAS, separation pay

In brief: Military income is not always read correctly by generic lenders. A VA-savvy lender should understand LES structure, allowances, special pay, and how income will continue after PCS.

A VA-friendly lender should know how to review BAH, BAS, base pay, and special pay without treating a military file like a standard civilian W-2 file.

The VA eligibility page says VA-backed financing requires satisfactory credit, sufficient income, a valid COE, and occupancy. For active-duty buyers, the income story is often more layered than a civilian pay stub.

A lender should understand:

Base pay shown on the LES

BAH and BAS

Special and incentive pays, such as flight pay or hardship duty pay

How PCS orders may change location-based allowances

Whether separation or transition income is stable enough for underwriting

This is where “VA-friendly Coastal Georgia lender” matters. We do not push a specific lender by name, but we do want buyers working with someone who can explain military income in plain English before the offer deadline.

PCS-specific considerations: remote pre-approval and POA

In brief: PCS buyers can complete pre-approval remotely before arriving in Coastal Georgia. The file should also account for orders, remote signing, inspection windows, and any power of attorney needs.

Many Coastal Georgia PCS buyers can complete pre-approval 60 to 90 days before reporting, then use the letter to shop remotely or during a short house-hunting window.

Remote pre-approval is normal. You can upload LES, bank statements, orders, tax documents, and COE information securely from your current duty station. The lender returns the letter electronically, and we use that letter to guide your search.

If a spouse or trusted representative may sign documents for you, discuss power of attorney early. VA’s lender sample documents note that when a POA is used, the lender must verify the veteran is alive and, for active-duty military, not missing in action.

The real estate side also needs coordination. Inspection scheduling, appraisal timing, walkthroughs, repair negotiations, and closing logistics should all support your report date. For a broader planning view, use our PCS home buying timeline.

Frequently asked questions

In brief: These are the quick answers military buyers usually need before starting lender conversations. Use them to prepare documents, understand timing, and protect your offer.

Ready to start your Coastal Georgia VA buying plan?

We offer a free 30-minute call for military buyers who want to understand VA pre-approval, PCS timing, neighborhoods, contract protections, and the right next step before writing an offer. Talk with Alex Rodino, U.S. Army Captain (veteran) and licensed Georgia Realtor®, about a practical Coastal Georgia buying plan.

Schedule a call through Coastal Georgia military relocation help or reach The ARC Platform through the contact options on the site.

The ARC Platform is affiliated with Keller Williams Realty. Alex Rodino is a licensed Georgia Realtor®, GA Real Estate License #443565. This content is for informational purposes only and is not legal, tax, lending, or financial advice. VA loan terms, eligibility, underwriting, and contract requirements should be confirmed with your lender, attorney, and appropriate professionals. Equal Housing Opportunity.

Join The Discussion