TL;DR: A first-time buyer in Savannah should plan for about $25,000 to $35,000 in cash at closing on a $325,000 home with 5% down conventional financing in 2026. VA, USDA, Georgia Dream, and the City of Savannah DreamMaker program can cut that to under $10,000, and sometimes under $5,000, for eligible buyers. Choose your lender before you choose the house, because the lender decides which assistance programs you can stack and how much cash you actually need.

By Alex Rodino, US Military Veteran, licensed Georgia REALTOR®, and founder of the Alexander Rodino Collective (ARC Platform) at Keller Williams Coastal Area Partners. Last reviewed: June 30, 2026.

Most first-time-buyer articles in Savannah will tell you the down payment number. They are technically correct and practically incomplete. The down payment is not the number you actually need to plan around. It is one part of the number.

The number that catches first-time buyers off guard is the total cash needed at the closing table. For a typical $325,000 Savannah home in 2026, that often runs roughly $25,000 to $35,000, covering not just the down payment but inspection, appraisal, attorney fees, title insurance, recording fees, transfer tax, prepaid escrow for property taxes and homeowners insurance, and lender origination fees.

That matters because Redfin’s Savannah housing market data recently showed a median sale price of $329,450 in March 2026, with homes spending a median of 99 days on market. So a $325,000 planning example is realistic for today’s Savannah buyer. (Redfin)

This guide is built to give you the rest of the picture. We walk through the complete cash-to-close itemization, the real monthly payment math at 2026 mortgage rates, three different buyer scenarios, every major assistance program available to a Coastal Georgia first-time buyer, and the hidden costs that show up after you get the keys.

No salesy “now is the best time to buy” pitch. Just the math.

If you want a no-pressure conversation with a Coastal Georgia agent before any lender pitches start, ARC works with first-time buyers from the listing-search stage all the way through closing, and beyond.

What does it actually cost to buy a first home in Savannah right now?

Answer: A first-time buyer purchasing a typical $325,000 Savannah home in 2026 should plan for $25,000 to $35,000 in cash at closing using a 5% down conventional loan with no assistance program. That total includes the down payment plus closing costs, lender fees, prepaid escrow, inspection, appraisal, title insurance, and recording fees.

The fast answer: a first-time buyer purchasing a typical Savannah home in 2026 should usually plan for $25,000 to $35,000 in cash at closing if they are using a 5% down conventional loan with no assistance program.

That estimate includes the down payment, buyer closing costs, lender costs, prepaid escrow, insurance, inspection, appraisal, and other transaction costs.

It does not include moving expenses, furniture, repairs after closing, HOA dues, or emergency reserves.

The fast answer

Using a $325,000 Savannah home as the baseline:

Loan type | Down payment | Approximate down payment cash |

|---|---|---|

Conventional 5% down | 5% | $16,250 |

FHA 3.5% down | 3.5% | $11,375 |

VA 0% down | 0% | $0 |

USDA 0% down | 0% | $0, if the property and buyer qualify |

The down payment is only part of the picture. A conventional buyer putting 5% down on a $325,000 home may still need another $8,000 to $18,000 for closing costs, prepaid escrow, inspections, appraisal, insurance, and lender fees.

That is how a buyer gets from “I saved my down payment” to “I still need $25,000 to $35,000 total.”

Your actual number can be much lower if you qualify for assistance. The City of Savannah’s DreamMaker Home Purchase Assistance program lists up to $50,000 in assistance for housing developed in partnership with the City of Savannah, and up to $30,000 for other eligible housing, both structured as 2% interest, 30-year deferred-payment loans. (City of Savannah)

What changes the number?

The total amount you need depends on five things.

- Loan program

FHA can lower the down payment to 3.5%. VA and USDA can reduce the down payment to 0% for eligible buyers and eligible properties. Conventional low-down-payment options may start at 3% or 5%, depending on the lender and borrower profile. - Property location

A home in a higher-risk flood zone can add flood insurance to the monthly payment and cash-to-close. If you are considering Tybee, Wilmington Island, Isle of Hope, Skidaway, Thunderbolt, or other water-adjacent areas, read ARC’s guide to Savannah flood zones before you make an offer. - Property condition

A home with FHA-required repairs, old roof concerns, termite damage, or safety items can create repair negotiations before closing. Sometimes the seller handles them. Sometimes the buyer pays. Sometimes the lender will not close until the work is completed. - Seller concessions

A negotiated seller credit of 2% to 3% can reduce your cash needed by thousands. On a $325,000 home, a 3% seller concession equals $9,750. - Assistance programs

DreamMaker, Georgia Dream, VA, USDA, and lender-specific grants can change the cash-to-close picture dramatically. In the right case, a buyer who expected to need $30,000 may need under $10,000, or even under $5,000.

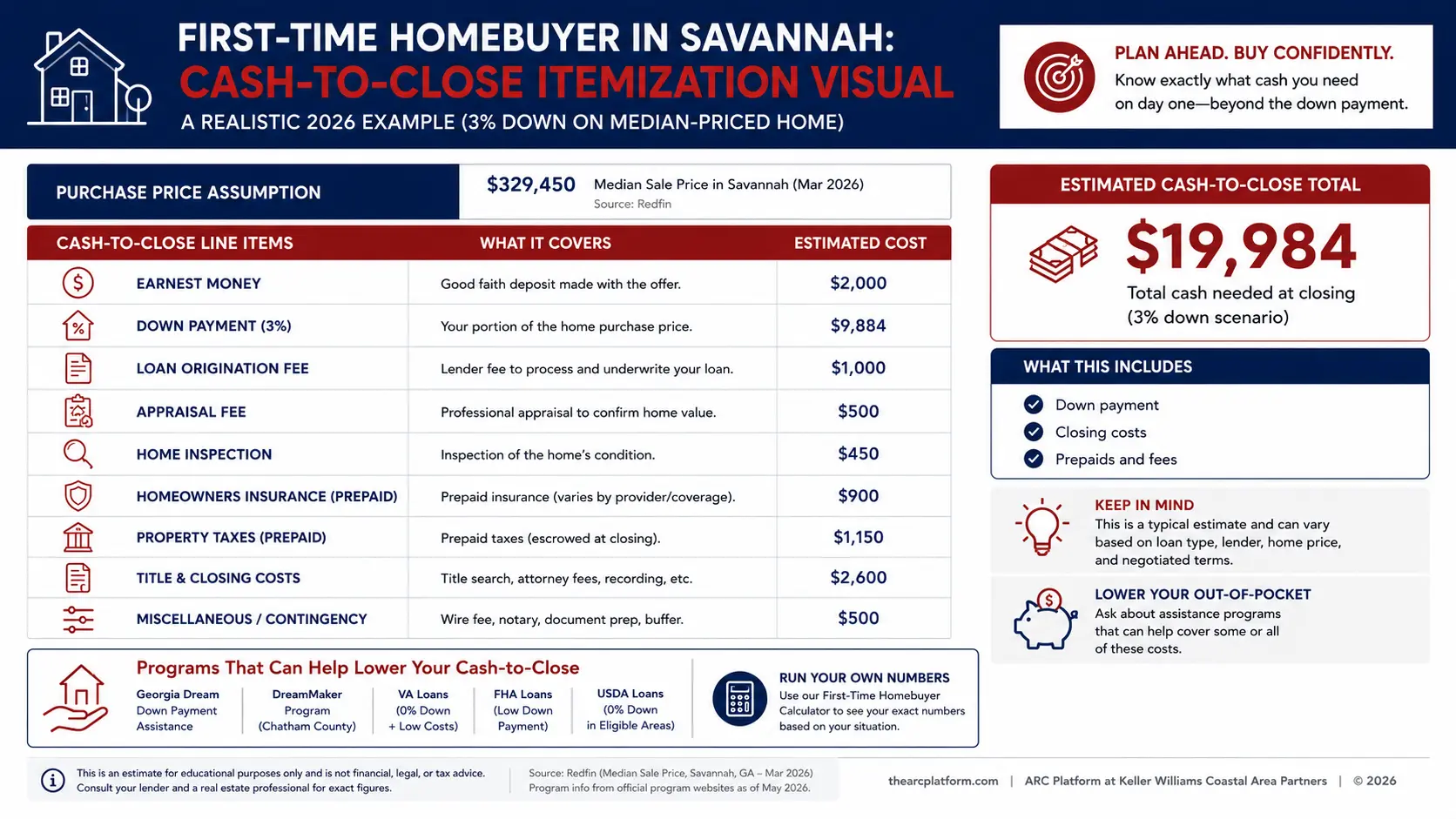

The complete cash-to-close itemization for a Savannah first-time buyer

Answer: On a $325,000 Savannah home with 5% down conventional and no assistance, expect $25,000 to $35,000 total cash at closing. The line-item breakdown below shows where every dollar goes, from earnest money and inspection to prepaid escrow and lender fees.

Here is the line-by-line version. This is the part most first-time buyers do not see until they are already emotionally attached to a house.

The example below assumes:

- $325,000 Savannah purchase price

- 5% down conventional loan

- No down-payment assistance

- No seller concessions

- No flood insurance requirement

Line item | Typical 2026 Savannah amount | Notes |

|---|---|---|

Earnest money deposit | $1,000 to $5,000 | Paid when the contract is accepted. Held in escrow and credited back to you at closing. |

Home inspection | $400 to $600 | Paid during due diligence, usually week 1 of the contract. Non-refundable. |

Appraisal | $500 to $700 | Required by the lender. Often paid before closing. |

Down payment, 5% conventional | $16,250 | 5% of $325,000. Lower with FHA. Zero down with VA or USDA if eligible. |

Loan origination fee | $1,500 to $3,000 | Lender fee, often quoted as a percentage of the loan amount. Sometimes reduced or waived. |

Owner’s title insurance | $900 to $1,400 | Optional but strongly recommended. Protects against title defects. |

Lender’s title insurance | $400 to $700 | Usually required by the lender. |

Closing attorney fee | $700 to $1,200 | Common buyer-side closing cost in Georgia transactions. |

Recording fees and transfer tax | $400 to $600 | Georgia’s real estate transfer tax is based on the sale price. The Georgia Department of Revenue describes the rate as $1 for the first $1,000 and 10 cents for each additional $100 or fraction of $100. (Department of Revenue) |

Prepaid escrow for homeowners insurance and property tax | $2,500 to $4,500 | Lender usually collects upfront reserves, plus the first year of homeowners insurance. |

Prepaid flood insurance, if applicable | $0 to $2,200+ | Only if the property requires or strongly warrants flood coverage. Zone X may be optional. AE or VE is a different conversation. |

FHA upfront mortgage insurance | $0 for conventional, or 1.75% of base loan on FHA | FHA only. Often financed into the loan rather than paid in cash. |

Total cash-to-close estimate | $25,000 to $35,000 | Planning range for a $325,000 Savannah home with 5% down conventional and no assistance. |

Your lender will give you a Loan Estimate after you apply. The Consumer Financial Protection Bureau says lenders are required to send a Loan Estimate within three business days after you submit the six key pieces of information for a mortgage application. That Loan Estimate is the document that matters. (Consumer Financial Protection Bureau)

Treat the numbers above as a planning estimate for when you start looking, not the final number you will owe at closing.

What does the monthly payment actually look like at current 2026 rates?

Answer: The estimated total monthly payment for a $325,000 Savannah home in 2026 lands between $2,480 and $2,660, including principal, interest, property taxes, homeowners insurance, and PMI or MIP. The exact number depends on loan type, credit score, and whether flood insurance applies.

The monthly payment is where the real affordability test happens.

For this section, we are using a conservative 6.5% to 7.0% mortgage-rate planning range. Freddie Mac’s Primary Mortgage Market Survey reported the average 30-year fixed-rate mortgage at 6.36% as of May 14, 2026, so the 6.5% to 7.0% range gives buyers a practical cushion for rate movement, credit-score pricing, lender differences, and program differences. (Freddie Mac)

Here is what the monthly payment may look like on a $325,000 Savannah home.

Loan type | Down payment | Loan amount | Monthly principal and interest | Plus taxes and insurance | Plus PMI / MIP | Estimated total monthly |

|---|---|---|---|---|---|---|

Conventional 5% | $16,250 | $308,750 | $1,950 to $2,055 | $425 | $155 PMI | $2,530 to $2,635 |

FHA 3.5% | $11,375 | $313,625 | $1,980 to $2,090 | $425 | $145 MIP | $2,550 to $2,660 |

VA 0% | $0 | $325,000 | $2,055 to $2,165 | $425 | $0 PMI | $2,480 to $2,590 |

These are planning numbers, not quotes. Your actual payment will depend on your credit score, rate lock, lender fees, loan type, property taxes, homeowners insurance, flood insurance, HOA dues, and whether mortgage insurance applies.

What this means for income required

A practical affordability screen is the 28% housing-cost guideline. It is not a hard approval rule, but it is useful for planning.

At a $2,600 monthly housing payment, 28% of gross monthly income points to a household income of about $111,000 to $112,000 per year.

That does not mean nobody can qualify below that. Some buyers qualify with higher debt-to-income ratios. VA and FHA underwriting may allow more flexibility. A buyer with no car payment, no credit-card debt, and strong reserves may be more comfortable than a buyer with the same income and $900 per month in other debt.

But for first-time buyers, the goal should not be “what is the maximum I can qualify for?”

The better question is: “What payment lets me own the home without being house-poor?”

Three real first-time-buyer scenarios in Coastal Georgia

Answer: Three realistic first-time buyer paths in Coastal Georgia: a single-income teacher in Pooler ($20,500 cash, $1,900–$2,050/mo), a dual-income couple at $375,000 ($28,000–$32,000 cash, $2,850–$3,050/mo), and a transitioning veteran using a VA loan ($6,500–$9,000 cash, $2,300–$2,500/mo). Each scenario below shows the math.

Every first-time buyer has a different path. The best way to make the numbers useful is to put them into real scenarios.

Scenario 1: Single-income teacher earning $58,000 per year

This buyer is looking in Pooler, Garden City, or an entry-level Savannah neighborhood for a $250,000 starter home.

A 5% down conventional loan would require a $12,500 down payment. Add roughly $8,000 for closing costs and prepaid escrow, and the buyer is around $20,500 total cash needed.

Estimated monthly payment: about $1,900 to $2,050, depending on rate, insurance, taxes, and PMI.

That is slightly tight on a $58,000 income if the buyer has other debt. But it may work if the buyer has low monthly obligations, qualifies for assistance, or receives seller concessions.

This buyer is a strong candidate for DreamMaker if buying inside Savannah city limits and meeting the program requirements. The City of Savannah says DreamMaker applicants must meet household-income limits, complete required homebuyer education, and use eligible properties. DreamMaker Home Purchase Assistance can make a major difference in the right case. (City of Savannah)

Scenario 2: Dual-income couple earning $120,000 combined

This couple is looking in Wilmington Island, Richmond Hill, Pooler, or a move-up starter area for a $375,000 home.

A 5% down conventional loan would require an $18,750 down payment. Add roughly $10,000 in closing costs and escrow, and the total cash needed lands around $28,000 to $32,000.

Estimated monthly payment: about $2,850 to $3,050, depending on rate, taxes, insurance, PMI, flood insurance, and HOA dues.

This couple is likely in better shape from a debt-to-income standpoint. They may not qualify for every local assistance program if their income exceeds the limit, but they should still ask lenders about Georgia Dream, Fannie Mae HomeReady, Freddie Mac Home Possible, lender credits, and seller concessions.

The point is not just whether they can buy. The point is whether they should keep enough cash after closing for repairs, furniture, moving, and emergency reserves.

Scenario 3: Veteran transitioning from Hunter or Fort Stewart

This buyer earns $75,000 in W-2 income and receives VA disability compensation. They are looking in Pooler, Hinesville, Richmond Hill, or nearby for a $300,000 home.

With a VA loan, the down payment may be $0. The VA explains that the VA home loan benefit does not require a down payment and does not require monthly private mortgage insurance, though lenders may still have their own credit and income requirements. VA home loan benefits are one of the strongest tools available to eligible buyers in Coastal Georgia. (VA Benefits)

Estimated cash-to-close: $6,500 to $9,000, mostly closing costs, prepaid escrow, inspection, appraisal, and reserves.

Estimated monthly payment: about $2,300 to $2,500, depending on rate, taxes, insurance, and whether the VA funding fee applies. VA notes that the funding fee helps support the program because VA loans do not require down payments or monthly mortgage insurance, and some veterans may be exempt from the fee. VA funding fee and closing costs should be reviewed before the buyer locks numbers. (Veterans Affairs)

The veteran path is one of the strongest first-time-buyer scenarios in Coastal Georgia, and one of the most underused.

If you are comparing Pooler, Garden City, Wilmington Island, Richmond Hill, Rincon, or Hinesville, ARC can help you compare the monthly cost by neighborhood, not just the list price.

First-time homebuyer assistance programs available in Coastal Georgia

Answer: Coastal Georgia first-time buyers can use five major assistance paths: DreamMaker (up to $50,000 in City of Savannah-developed housing, $30,000 elsewhere), Georgia Dream (5%–6% of price, up to $12,500), VA (0% down, no monthly PMI), USDA (0% down in eligible rural areas), and FHA (3.5% down). Eligibility depends on income, location, occupation, and lender participation.

This is the section most buyers miss. They assume they need to save the entire down payment and closing cost amount themselves. Sometimes they do. Sometimes they do not.

The right program depends on income, occupation, military status, property location, credit profile, and lender participation.

DreamMaker Home Purchase Assistance, City of Savannah

The City of Savannah’s DreamMaker Home Purchase Assistance program can provide substantial help for eligible buyers purchasing inside the city. The city lists up to $50,000 in assistance for housing developed in partnership with Savannah, and up to $30,000 for other eligible housing, both as 2% interest, 30-year deferred-payment loans. (City of Savannah)

This can be a major bridge for a first-time buyer who has the income to afford the monthly payment but not the cash to cover down payment and closing costs.

Best fit: lower- to moderate-income buyers purchasing eligible homes inside Savannah city limits.

Georgia Dream Homeownership Program

The Georgia Dream Homeownership Program is a statewide program through the Georgia Department of Community Affairs. DCA’s current program page lists down-payment loan options of 5% of the purchase price or up to $10,000 for standard eligible homebuyers, whichever is less. It also lists 6% of the purchase price or up to $12,500 for PEN buyers and CHOICE buyers, whichever is less. (Georgia Department of Community Affairs)

PEN refers to Protectors, Educators, and Nurses. That can include many teachers, healthcare workers, law enforcement workers, firefighters, military buyers, and related occupations, depending on DCA’s current eligibility rules.

Best fit: first-time buyers across Chatham, Bryan, and Effingham counties who meet income and purchase-price limits and work with a participating lender.

VA Home Loan

For eligible service members, veterans, and certain surviving spouses, the VA loan can be the strongest first-time-buyer path in Coastal Georgia.

The VA home loan benefit can offer no required down payment, no monthly PMI, competitive rates, and limited closing costs. VA home loan eligibility should be checked early, especially for buyers connected to Hunter Army Airfield, Fort Stewart, or a recent military transition.

Service members and veterans relocating to the area can also get Coastal Georgia military relocation help tailored to PCS timelines and base proximity.

Best fit: eligible military and veteran buyers who want to preserve cash and avoid monthly PMI.

USDA Rural Development Loan

The USDA loan can offer 0% down financing for eligible buyers purchasing eligible properties in rural-designated areas.

The important word is “eligible.” USDA property eligibility is address-specific. The official USDA Income and Property Eligibility site explains that household income must meet USDA guidelines and the home must be in an eligible rural area. (USDA Eligibility)

Many buyers assume USDA is only for remote farmland. That is not always true. Some areas outside the Savannah core may qualify. Before ruling it out, check the property address and income limits.

Best fit: buyers considering Bryan County, Effingham County, parts of Liberty County, and some areas outside the urban Savannah core.

FHA 203(b) standard loan

FHA is not exactly an assistance program, but it is one of the most common first-time-buyer loan paths.

The FHA 203(b) program allows low down payments for eligible buyers. A borrower with a credit score of 580 or higher may be eligible for maximum FHA financing with a 96.5% loan-to-value ratio, meaning 3.5% down. The FDIC’s affordable mortgage lending guide summarizes this FHA framework. (FDIC)

FHA can be helpful for buyers with lower down payments, more flexible credit needs, or higher debt-to-income ratios. It also allows seller concessions, which can help reduce cash needed at closing.

Best fit: first-time buyers who do not qualify for VA or USDA and need a lower down payment than a standard conventional loan.

Lender-specific first-time-buyer programs

Many lenders have their own first-time-buyer credits, grants, reduced origination fees, Federal Home Loan Bank grant access, or special low-down-payment products.

These change often. Some are available until the funding pool runs out. Some require income limits. Some require a specific census tract. Some are tied to a first-time-buyer education course.

Before choosing a lender, ask this exact question:

“What first-time-buyer, down-payment assistance, closing-cost credit, grant, or special conventional program do you participate in for Chatham, Bryan, or Effingham County?”

Then ask the next lender the same question.

Wondering which assistance programs you qualify for? ARC can walk through the options with you before you pick the wrong lender or miss a program.

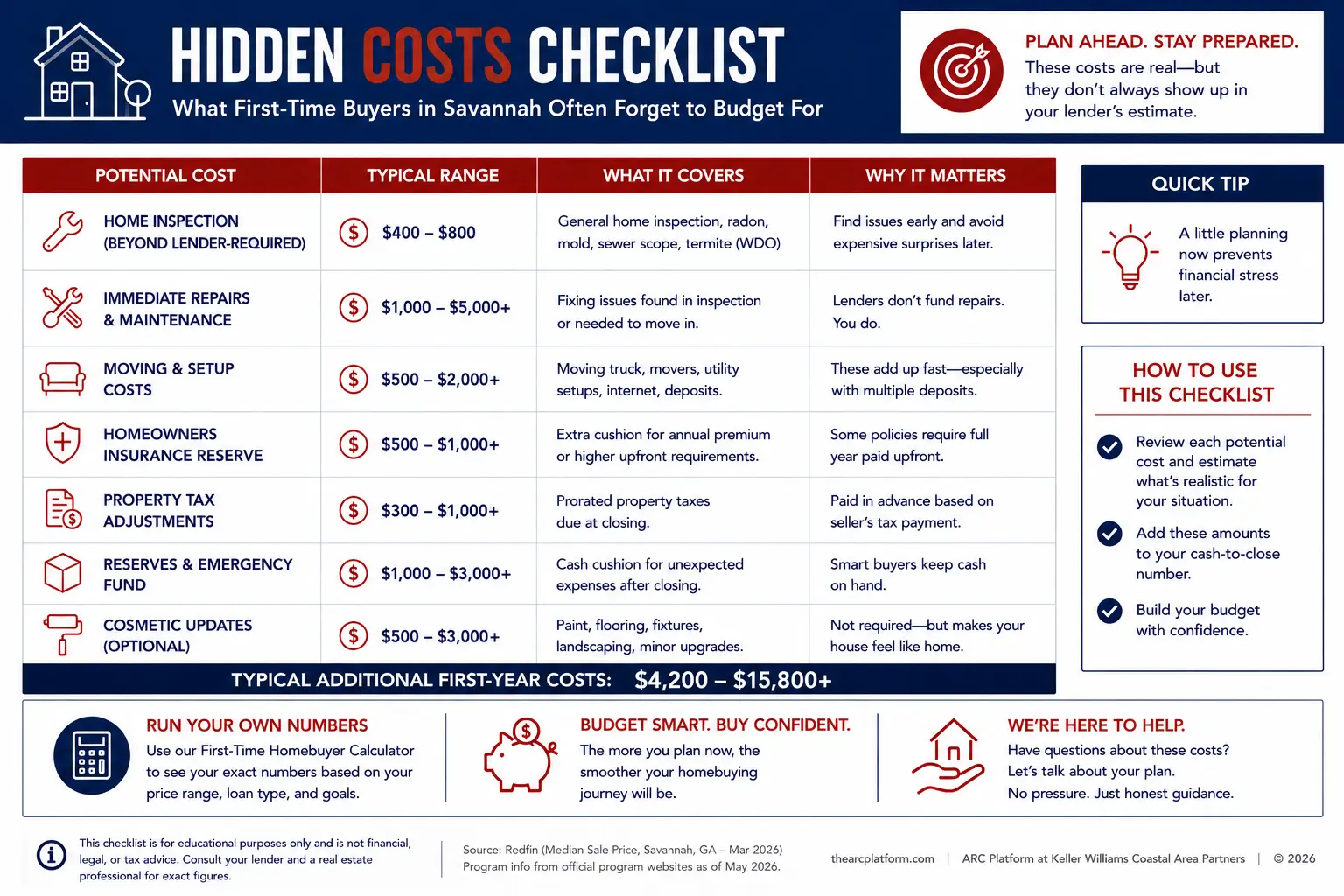

The costs first-time buyers forget about

Answer: Plan for an additional $10,000 to $20,000 in first-year costs beyond closing: moving ($800–$3,000), immediate repairs ($2,000–$5,000), new-homeowner essentials ($1,500–$3,000), HOA dues ($40–$300+/mo), property tax reassessment, insurance changes, and a $5,000–$10,000 emergency repair fund.

The closing table is not the end of the spending. It is the start of ownership.

Here are the costs buyers forget to budget for.

Moving costs: $800 to $3,000

A local DIY move may stay under $1,000. Movers, storage, packing supplies, truck rental, utility deposits, and time off work can push it higher.

Immediate repairs and replacements: $2,000 to $5,000

Even a good home usually needs something in the first 90 days. Door hardware, paint, appliances, minor plumbing, electrical fixes, pest treatment, blinds, landscaping, and cleaning add up quickly.

New homeowner essentials: $1,500 to $3,000

Lawn equipment, a basic toolkit, ladder, hoses, trash bins, window treatments, shelves, bath towels, pantry supplies, and security items are not glamorous, but they are real.

HOA dues: $40 to $300+ per month

Many Coastal Georgia subdivisions have HOA dues. Resort-style communities and gated communities can run much higher. Always ask for the HOA budget, dues, transfer fee, and rules before your due-diligence period ends.

Property tax changes in year two

Your first-year estimate may not match your second-year bill. Reassessment, exemptions, and escrow adjustments can change your payment after closing.

Insurance changes

Coastal Georgia insurance is not something to guess at. Homeowners insurance, flood insurance, wind/hail deductibles, roof age, flood zone, claims history, and carrier availability can all change the monthly number.

Emergency repair fund: $5,000 to $10,000

A first-time buyer should not spend every dollar getting into the home. HVAC failure, water leaks, roof issues, appliance replacement, and storm damage can happen in year one.

Plan for $10,000 to $20,000 in additional first-year costs beyond the closing-table number if you want to own with breathing room.

Frequently asked questions

How much do I really need to buy a house in Savannah?

For a typical $325,000 Savannah home in 2026, a first-time buyer should plan for $25,000 to $35,000 in total cash at closing using a 5% down conventional loan. That number can drop below $10,000 with a VA loan, or potentially below $5,000 with the right assistance program, seller concessions, and lender structure. Confirm with your lender’s Loan Estimate before making an offer.

What is the 3-3-3 rule in real estate?

The 3-3-3 rule is an informal planning guideline. It usually means three months of mortgage payments saved in reserve, 3% or more for a down payment, and 3% or more of the purchase price set aside for closing costs. It is not a hard lending rule. Actual loan programs may allow lower down payments, lower reserves, or assistance funds.

What is a realistic first home price in Savannah?

As of 2026, a realistic first-home price range in Savannah and nearby Coastal Georgia communities is often $225,000 to $375,000, depending on neighborhood, condition, loan type, and buyer expectations. Pooler, Garden City, Rincon, and some Southside or West Chatham areas may offer lower entry points. Wilmington Island, Richmond Hill, downtown Savannah, and historic neighborhoods usually run higher.

How much are closing costs for a buyer in Georgia?

For a typical Georgia home purchase, buyer closing costs often run 2% to 4% of the purchase price. That includes lender fees, attorney fees, title insurance, appraisal, recording fees, transfer tax, prepaid escrow for taxes and insurance, and other loan-related costs. On a $325,000 Savannah home, that usually means $6,500 to $13,000 separate from the down payment.

What is a good budget for first-time home buyers in Savannah?

A practical first-time-buyer budget for Savannah in 2026 looks like this: household income of $75,000 or more for entry-level purchases, $25,000 to $35,000 in cash for a 5% down conventional path, $5,000 to $10,000 in emergency reserves, and a monthly housing payment that does not put the household under stress. Buyers using VA, USDA, DreamMaker, Georgia Dream, or seller concessions may need less cash at closing.

Does Savannah have first-time homebuyer assistance programs?

Yes. Savannah buyers may have access to DreamMaker through the City of Savannah, Georgia Dream through the Georgia Department of Community Affairs, VA loans for eligible military and veteran buyers, USDA loans for eligible rural-area purchases, FHA low-down-payment loans, and lender-specific grants or credits. Eligibility depends on income, property location, purchase price, lender participation, and program funding.

Closing thoughts and next steps

Answer: The single biggest decision in this process is which lender, not which house. Talk to two or three lenders, get itemized Loan Estimates, compare them line by line, and confirm which assistance programs you actually qualify for before making an offer. The right combination can cut $10,000 to $20,000 off your cash-to-close.

The single biggest decision in this process is not which house. It is which lender.

The lender you choose decides which loan programs you have access to. The lender’s quoted rate decides your monthly payment. The lender’s underwriting standards decide whether you can use seller concessions, whether you can stack assistance programs, and whether you can close on the timeline the seller needs.

Most first-time buyers shop for a house first and a lender second. The math works better the other way around.

Before you make an offer, talk to two or three lenders. Get itemized Loan Estimates from each. Compare them line by line. Then look at the assistance programs you actually qualify for: Georgia Dream, DreamMaker, VA, USDA, FHA, or lender-specific grants.

The right combination can cut $10,000 to $20,000 off your cash-to-close in the right case.

When you are ready for the agent conversation, ARC works with first-time buyers from the listing-search stage all the way through closing, and beyond. We are not a lender. We do not earn fees on your mortgage. But we have walked first-time buyers through this process, and we will walk you through yours honestly and at your pace.

Join The Discussion