VA IRRRL Streamline Refinance for Coastal Georgia Veterans: 2026 Rules, Rates, and the 210/6 Seasoning Trap

The VA IRRRL is one of the simplest refinance tools available to an existing VA loan borrower in 2026, but the 210/6 seasoning rule and Net Tangible Benefit test are where many Coastal Georgia veterans get tripped up. If you already have a VA loan near Savannah, Pooler, Richmond Hill, Hinesville, Fort Stewart, or Hunter AAF, the question is not just “can I lower my rate?” The better question is whether the timing, closing costs, funding fee, and future PCS plan make the refinance worth doing. In our veteran-led ARC lane, we look at the mortgage math and the resale timeline together, because a refinance that looks good on paper can still be a poor move if you are selling soon.

If you bought during a PCS window, start with the Hunter AAF and Fort Stewart buyer’s guide, then use this IRRRL guide to decide whether a refinance helps the next chapter.

What the VA IRRRL is, and what it isn’t

In brief: A VA IRRRL is a VA-to-VA refinance designed to lower your payment or make your payment more stable. It is not a cash-out loan.

A VA Interest Rate Reduction Refinance Loan, usually shortened to VA IRRRL, is a refinance product for borrowers who already have a VA-backed home loan. It replaces the existing VA loan with a new VA loan under different terms, usually a lower payment, lower rate, or a move from an adjustable rate to a fixed rate.

VA describes an IRRRL as a streamline option to reduce monthly payments or make payments more stable. You may not receive cash from the loan proceeds.

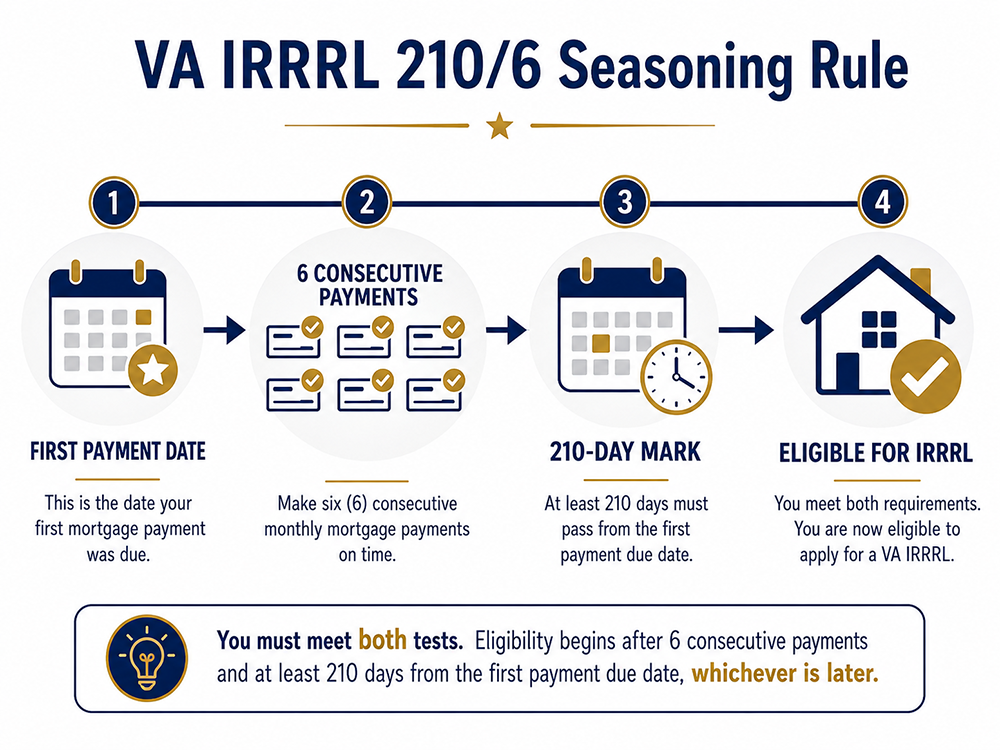

The 210/6 seasoning rule (the #1 reason IRRRLs get rejected)

In brief: You generally need six consecutive monthly payments and at least 210 days from the first payment due date before the new IRRRL can close.

The 210/6 rule is a timing test, not a rate test. VA guidance clarified that IRRRL applications taken after July 26, 2019 must be seasoned based on 210 days after the due date of the first monthly payment on the loan being refinanced.

Before you apply, pull your mortgage statement and check the first-payment due date, six-payment history, and earliest closing date that satisfies both tests.

Alex’s note: We see service members shop rates before they are eligible. Rate watching is smart. Letting a lender run a file before the seasoning math works is where frustration starts.

The Net Tangible Benefit test

In brief: The refinance must create a real borrower benefit. For fixed-to-fixed VA IRRRLs, that usually means a lower rate and a sensible recoupment period.

The Net Tangible Benefit test asks whether the new loan is actually in the borrower’s financial interest. The federal refinance rule defines net tangible benefit as a new loan that is in the borrower’s financial interest, and requires an old-loan versus new-loan comparison.

In plain English, VA does not want veterans churned into refinances that add costs without real benefit. A fixed-to-fixed loan usually needs a rate drop. An ARM-to-fixed move can still make sense if payment stability is the benefit. Our VA funding fee walkthrough can help you understand why a lower monthly payment is not always a lower lifetime cost.

2026 VA refi rates and funding fee, the actual math

In brief: On June 16, 2026, live 30-year VA refinance context showed roughly 5.625% to 6.05% depending on lender assumptions, points, credit profile, and APR treatment. The VA IRRRL funding fee is 0.5% unless you are exempt.

Rate pages move daily, but this draft’s live check showed Bankrate’s national average 30-year VA refinance interest rate at 6.05% on June 16, 2026, while Navy Federal showed a sample 30-year VA Streamline loan at 5.625% interest with listed APR assumptions.

The VA funding fee for IRRRLs is 0.5% of the loan amount, and VA says that rate does not change based on down payment or prior use. Veterans receiving qualifying service-connected disability compensation are exempt.

| Current loan balance | 0.5% IRRRL funding fee | Practical read |

| $300,000 | $1,500 | Needs a meaningful rate drop |

| $400,000 | $2,000 | Needs clear monthly savings |

| $500,000 | $2,500 | Watch total balance |

If your lender needs the entitlement record, our VA Certificate of Eligibility guide explains the VA.gov route.

What you DON’T need (no appraisal, no income verification, no NTB exception in most cases)

In brief: IRRRL documentation is intentionally lighter than a purchase loan or cash-out refinance. The point is speed and lower friction, not skipping the math.

VA’s benefits page says no appraisal or credit underwriting package is required for an IRRRL, and it also notes that lenders vary. Typically, you should not expect a new full appraisal, full income verification, or full asset review in a clean IRRRL.

A lender may still ask for more if your credit, property, occupancy, or servicing history creates risk. Use the IRRRL because it is faster and cleaner, not because it lets you ignore the break-even date.

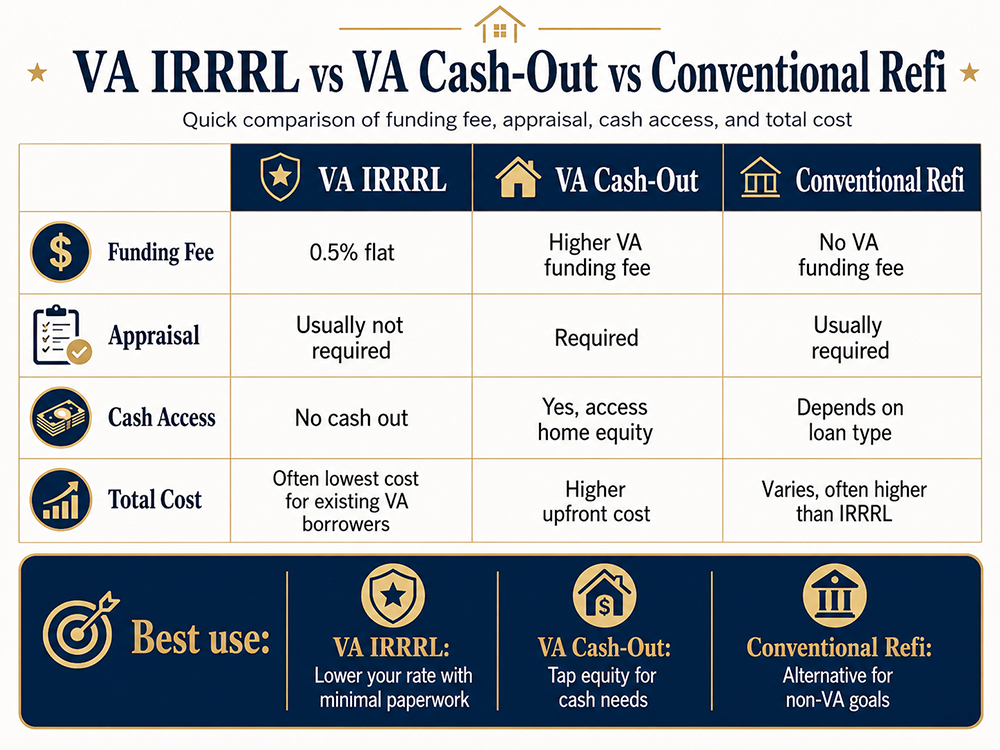

IRRRL vs cash-out refi vs conventional refi for Coastal GA veterans

In brief: IRRRL is usually the lowest-friction refinance for a homeowner who already has a VA loan and does not need cash. Cash-out and conventional refinances solve different problems.

| Refinance option | Best fit | Watch-out |

| VA IRRRL | Lowering rate or stabilizing payment on an existing VA loan | No cash out, must meet seasoning and benefit tests |

| VA cash-out refinance | Pulling equity or refinancing a non-VA loan into VA | Higher funding fee, appraisal, and full underwriting |

| Conventional refinance | Strong-equity borrowers who want to exit VA terms | PMI, credit pricing, and closing costs can erase the advantage |

If you may buy again after selling or renting the home, read our guide to second-tier VA entitlement before assuming the next purchase is blocked.

National PCS-realtor aggregators can explain VA basics at scale. ARC’s value is narrower: we connect the refinance decision to Savannah-area resale timing, Fort Stewart and Hunter AAF movement patterns, and the next PCS exit plan.

When NOT to IRRRL, three Coastal Georgia scenarios where it doesn’t pencil

In brief: A lower advertised rate does not automatically make an IRRRL a smart move. The refinance should survive the hold-period test, the closing-cost test, and the future-sale test.

A 12 to 24 month PCS or sale window can make an IRRRL fail even when the new monthly payment is lower. If the refinance takes 30 months to recoup, but you may sell in 18 months, it is probably not doing its job.

Three common no-go scenarios:

- You are already at or below current market rates, so there may be no Net Tangible Benefit.

- You expect to PCS, sell, or convert the home to a rental before the break-even date.

- You have paid the loan down substantially and the monthly savings are too small to justify resetting the clock.

This is where Coastal Georgia military relocation help belongs. We are not your lender, but we can help pressure-test the eventual exit strategy.

Alex’s note: In the Army, a plan that ignores the next movement is not a plan. A refinance is similar. The rate matters, but the next move matters too.

Frequently asked questions

In brief: Check eligibility, seasoning, benefit, funding fee status, and hold period before you chase a quoted rate.

Join The Discussion