By Alex Rodino, Founder, Alexander Rodino Collective | Serving Savannah & Coastal Georgia

Last updated: June 30, 2026

Editorial disclosure: This guide is general information, not legal, financial, or tax advice. Georgia foreclosure timelines move quickly. If you have received a Notice of Sale, contact a Georgia foreclosure attorney or HUD-approved housing counselor immediately. Alex Rodino is a licensed Georgia real estate agent with Keller Williams Coastal Area Partners. This guide is written from a real estate coordination perspective, not as legal advice.

Urgent note: If your foreclosure auction is scheduled within the next 30 days, scroll to the section titled “If You Have Less Than 30 Days.”

If your foreclosure auction is scheduled within 30 days, talk to a Georgia foreclosure attorney today, and call ARC for a same-day home valuation. Time is the asset you cannot replace.

TL;DR

- Pre-foreclosure in Savannah moves fast because Georgia is a non-judicial

- foreclosure state. A lender can foreclose without filing a lawsuit when the loan documents allow power of sale.

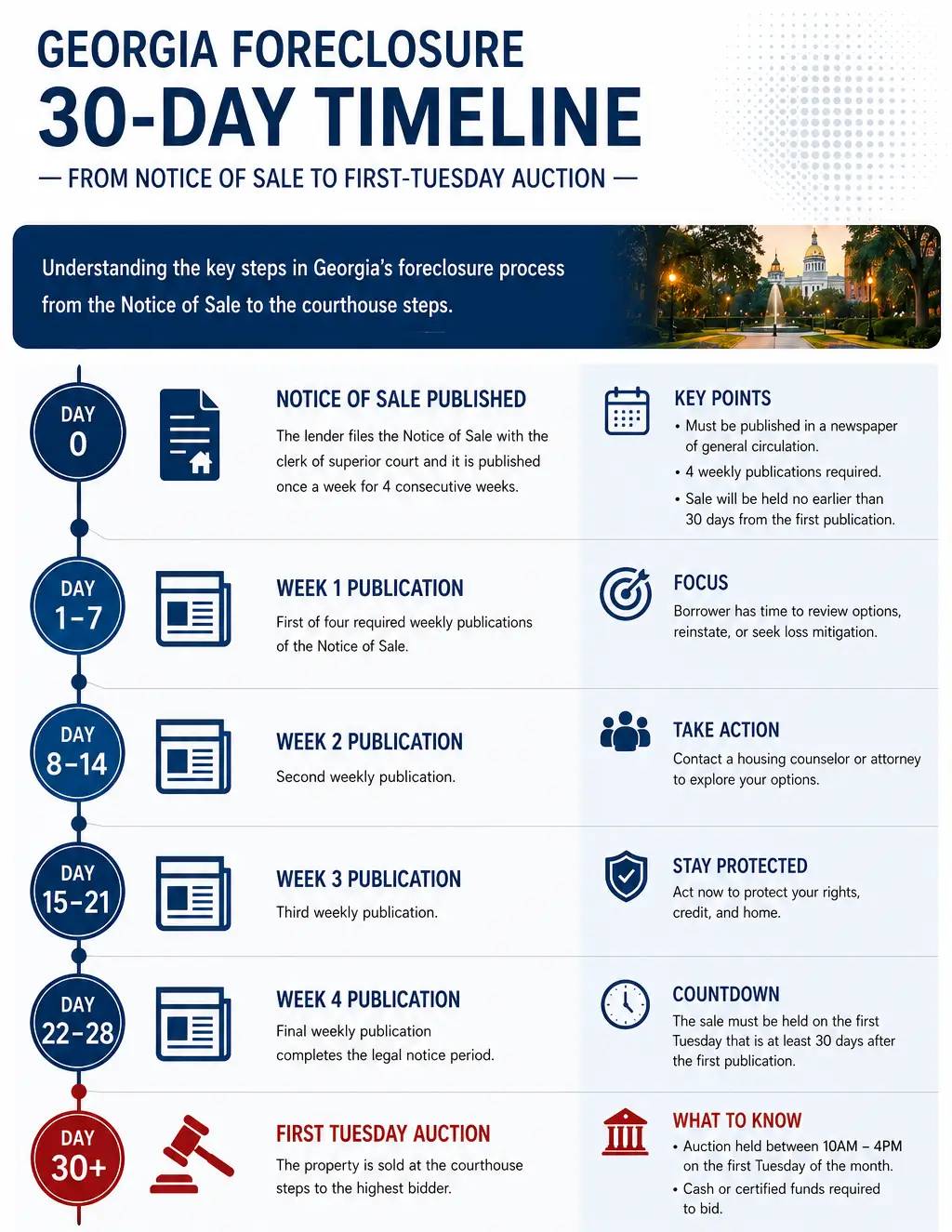

- In Georgia, the required Notice of Sale must be sent at least 30 days before the proposed foreclosure sale, and sales happen on the first Tuesday of the month.

- Your five real options are reinstatement, loan modification, traditional or fast MLS listing, short sale, or cash sale.

- The right path depends on four things: days left before auction, equity position, whether you can afford the home long term, and whether the lender will approve a workout.

- A HUD-approved housing counselor, foreclosure attorney, and neutral real estate professional can each help with a different part of the decision.

How Foreclosure Actually Works in Georgia (The 30-Day Reality)

On This Page

- How Foreclosure Actually Works in Georgia (The 30-Day Reality)

- The Five Real Options You Have (Decision Tree)

- The Decision Tree: Which Path Fits Your Situation?

- If You Have Less Than 30 Days (Read This First)

- How Your Credit Is Affected by Each Path

- Free Resources Every Savannah Pre-Foreclosure Homeowner Should Use

- 6 Common Mistakes That Cost Savannah Homeowners Their Equity

- When Bankruptcy Is Actually the Right Answer

- Frequently Asked Questions

Georgia Foreclosure At a Glance

| Foreclosure type | Non-judicial (court filing not required) |

| Minimum Notice of Sale period | 30 days before the sale |

| Auction day | First Tuesday of the month, 10:00 a.m. – 4:00 p.m. |

| Federal pre-foreclosure threshold | 120 days delinquent (CFPB rule) |

| Right of redemption after sale | Not practical for standard mortgage foreclosure |

| Governing statute family | O.C.G.A. § 44-14-162 through § 44-14-162.4 |

| County for Savannah properties | Chatham County (Bryan, Effingham nearby) |

Georgia foreclosure is fast because most residential foreclosures are handled outside court. The Georgia Attorney General explains that Georgia is a “non-judicial foreclosure” state, meaning a lender can foreclose without filing suit or appearing before a judge when the security deed allows it. Georgia Attorney General mortgage and foreclosure information (Office of the Attorney General)

Georgia is a non-judicial foreclosure state

In Georgia, the general rule is that foreclosure begins after default under the promissory note or deed to secure debt. Usually, that default is missed mortgage payments, but the Attorney General’s consumer page also notes that default can include issues such as failing to maintain insurance or pay property taxes. (Office of the Attorney General)

The key statute family is O.C.G.A. § 44-14-162 through § 44-14-162.4. For a Savannah homeowner, what this actually means is simple: once the foreclosure process is moving, the lender usually does not need to file a traditional lawsuit before setting a sale date. That is why pre foreclosure Savannah decisions have to be made in days and weeks, not months.

The 30-day Notice of Sale requirement

Georgia law requires the lender to send written notice at least 30 days before the proposed foreclosure sale. The notice must include the name, address, and phone number of someone with authority to negotiate, amend, and modify the mortgage terms. (Office of the Attorney General)

The notice also must be sent by registered mail, certified mail, or statutory overnight delivery, and it must include a copy of the foreclosure sale advertisement. The Attorney General’s page warns that refusing to accept the notice does not invalidate it. (Office of the Attorney General)

For Chatham County, legal notices commonly run through the county’s legal organ. A Chatham County Probate Court publication sheet identifies the Savannah Morning News as the county legal organ for probate notice publication, and Georgia foreclosure notices are also published in the official county newspaper for public announcements. (cms.chathamcountyga.gov)

The first-Tuesday-of-the-month auction rule

Georgia foreclosure sales take place on the courthouse steps in the county where the property is located. By law, those sales happen on the first Tuesday of the month between 10:00 a.m. and 4:00 p.m. (Office of the Attorney General)

For a Savannah property, that usually means Chatham County. For a home in Richmond Hill, Bryan County may be involved. For a Rincon home, Effingham County may be involved. The Chatham County Clerk of Superior Court’s Real Estate Recording Division handles recording, processing, and indexing real estate documents related to Chatham County property. Chatham County Superior Court Clerk real estate recording information (superiorcourtclerk.chathamcountyga.gov)

Georgia does not give you a practical post-sale do-over

After a valid foreclosure sale, the winning bidder becomes the new owner. The Georgia Attorney General’s page states that a valid foreclosure wipes out the borrower’s right to live in the house, and the new owner may pursue eviction through a dispossessory action. (Office of the Attorney General)

What this actually means for you: do not treat the auction date as a flexible deadline. In a standard Georgia non-judicial mortgage foreclosure, the safe planning assumption is that you need to resolve the loan, sell the house, obtain a legal stay, or get the sale postponed before the auction.

Federal servicing rules also matter. The CFPB says the legal foreclosure process generally cannot start until a borrower is at least 120 days behind on the mortgage, although the time from that point to sale depends on state law. (Consumer Financial Protection Bureau)

Talk to a Georgia foreclosure attorney or HUD-approved housing counselor about your specific situation.

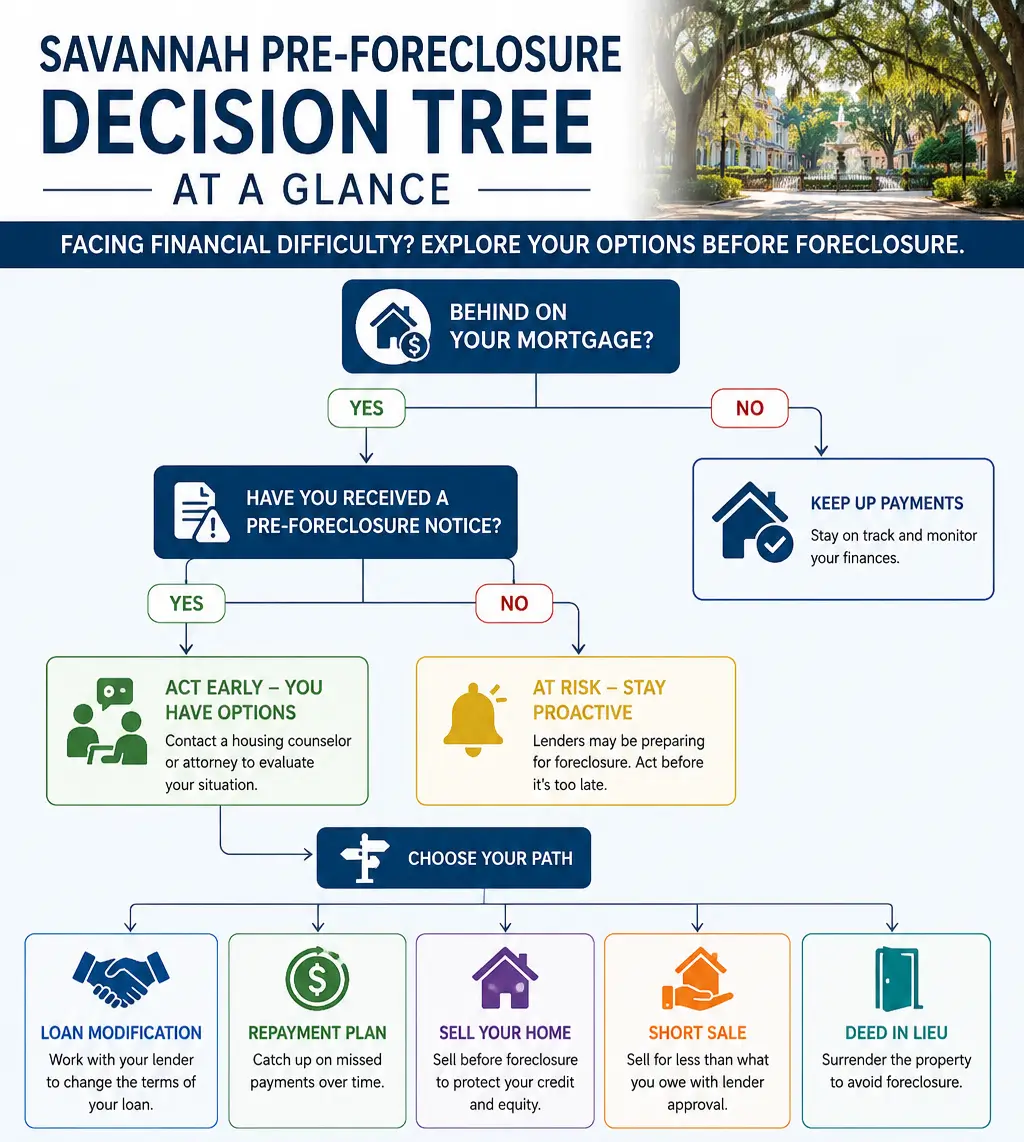

The Five Real Options You Have (Decision Tree)

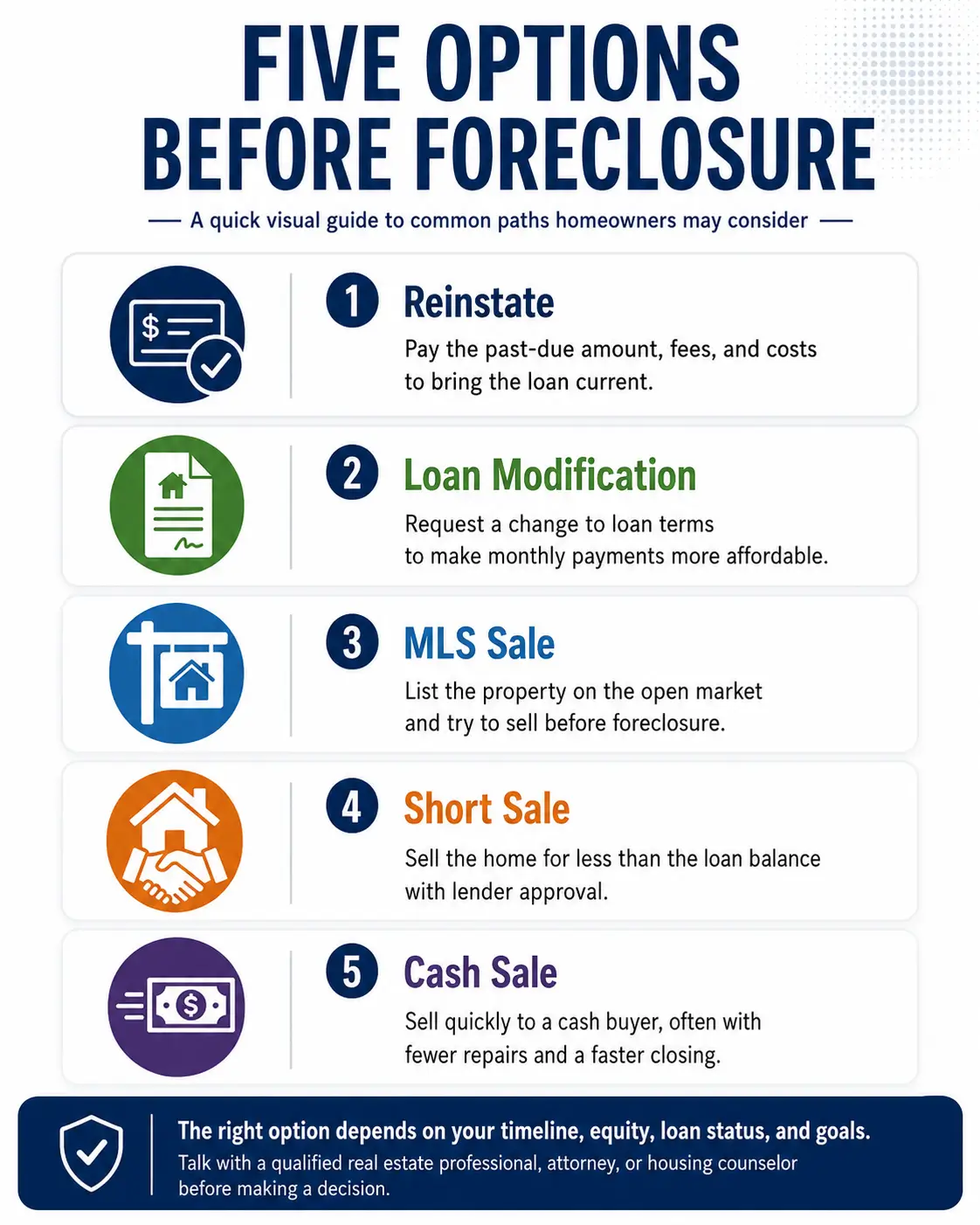

Pre foreclosure Savannah homeowners usually have five real paths: reinstate, modify, list, short sale, or sell for cash. The right path depends on whether you want to keep the home, how much time you have, and whether the home has equity.

Option 1: Reinstate the Loan (If You Can Catch Up)

Reinstatement means you pay the full past-due amount, fees, and approved costs needed to bring the mortgage current. It is usually the cleanest path if you have access to enough cash and want to keep the home.

This can make sense if you have a one-time cash source, such as a tax refund, family loan, insurance settlement, sale of another asset, or other verified funds. Ask the servicer for a written reinstatement quote. Do not rely on a verbal payoff number.

A reinstatement quote should identify the amount due, due date, payment method, and whether any fees may still change. If the foreclosure sale is close, confirm in writing that paying the quoted amount by the deadline will stop or postpone the sale.

The benefit is control. You keep the property, keep your equity, and avoid a completed foreclosure sale. The drawback is that reinstatement requires the largest immediate cash payment.

Option 2: Loan Modification (Renegotiate the Loan)

A loan modification changes the mortgage terms so the homeowner can stay in the property. Depending on the loan program and investor rules, a modification may extend the term, add arrears to the balance, adjust the rate, use a partial claim, or otherwise change the payment structure.

HUD explains that FHA home-retention options can help bring a mortgage current and may reduce the monthly payment. HUD lists repayment plans, forbearance, partial claims, loan modifications, combination options, and payment supplements as potential loss mitigation tools for FHA borrowers. HUD FHA loss mitigation program information (HUD)

A loan modification Georgia homeowner should start by requesting a loss mitigation application from the mortgage servicer. You will usually need recent paystubs, bank statements, tax documents, a hardship explanation, expense information, and any documents the servicer specifically requests.

The timeline matters. The CFPB’s Regulation X loss mitigation rule says that if a servicer receives a complete loss mitigation application more than 37 days before a foreclosure sale, the servicer generally must evaluate the borrower within 30 days. The same rule also restricts conducting a foreclosure sale in certain situations after a complete application has been received. (Consumer Financial Protection Bureau)

The word “complete” is the trap. An incomplete package may not give you the protection you think it gives you. Use a HUD-approved housing counselor if you are trying to modify the loan. HUD’s Georgia page says a HUD-approved housing counseling agency can offer advice customized to housing needs, and HUD’s foreclosure counseling is available free of charge. (HUD)

Option 3: Traditional or Fast MLS Sale (When You Have Equity and Time)

A traditional or fast MLS sale means you list the home with a real estate agent who understands the foreclosure clock. The goal is to sell before the auction, pay off the loan, and preserve as much equity as possible.

This path makes sense when you owe less than the home is worth and have enough time to close before the auction. If the auction is 60+ days away, a fast listing may still be realistic. If the auction is less than 30 days away, the margin for a financed buyer may be too thin.

The fast-listing strategy is not the same as panic pricing. The home needs a market valuation, clean showing access, strong photography, fast title coordination, and a price designed to generate serious offers quickly. In pre foreclosure Savannah situations, the cleanest offer may be better than the highest offer if the clean offer can close before the auction.

This is where ARC can serve as a neutral coordinator. We coordinate with the homeowner, servicer, closing attorney, and buyer-side parties so everyone understands the deadline. If the home is in Pooler, Ardsley Park, Midtown Savannah, Wilmington Island, or Georgetown, pricing has to reflect the property’s condition and micro-market, not just a broad online estimate.

For market context before choosing a price, read how Savannah home values are trending in 2026. FHFA also publishes the House Price Index, which measures single-family house price changes across metro areas using repeat-sales data. FHFA House Price Index methodology (FHFA.gov)

Option 4: Short Sale (When You Owe More Than the Home Is Worth)

A short sale means the lender agrees to accept less than the full mortgage balance so the home can sell. It is usually for homeowners who owe more than the property is worth and cannot reinstate or modify the loan.

The Georgia Attorney General describes a short sale as selling the home for less than the balance remaining on the mortgage. The lender must approve it in advance, and if approved, the mortgage holder agrees to accept the sale proceeds and cancel the mortgage. (Office of the Attorney General)

A short sale Savannah Georgia process typically requires a listing agreement, buyer contract, hardship letter, financial package, estimated settlement statement, and lender review. The buyer must be patient because the lender’s approval controls the timing.

A short sale can be useful when the property is underwater, the homeowner has a documented hardship, and the auction is far enough away for lender review. If the sale date is already within 30 days, a short sale may be unrealistic unless the servicer grants a postponement in writing.

Deficiency risk should also be reviewed. The Georgia Attorney General explains that after foreclosure, a mortgage holder may file suit to recover the difference between the foreclosure sale price and the remaining note balance, called a deficiency proceeding. (Office of the Attorney General) In a short sale, ask the lender in writing whether it is waiving any deficiency rights as part of approval.

Option 5: Cash Sale to an Investor (When the Clock Has Run Out)

A cash sale means selling the property to an investor or cash buyer who can close quickly. It is usually a last-resort equity preservation path when there is not enough time for a normal MLS listing, loan modification, or short sale.

This path makes sense when there are fewer than 30 days before the Savannah foreclosure auction, the home has equity, and the homeowner cannot reinstate or obtain a written postponement. Cash buyers usually price for speed, risk, repairs, and resale margin, so the net is usually lower than an open-market listing.

The key is comparison. If you accept the first investor offer, you may leave money on the table. ARC can help compare legitimate cash offers through a vetted local network so you are not relying on the first postcard, text, or online form response.

Before choosing this path, read the cash buyer comparison guide we wrote for Savannah sellers. A cash sale can be the right move when time is gone, but it should be chosen because the math supports it, not because pressure made the decision for you.

Not sure which of the five paths fits your situation? ARC offers a private, no-pressure conversation to map your specific timeline, equity position, and best next step. No listing obligation.

Talk to a Georgia foreclosure attorney or HUD-approved housing counselor about your specific situation.

The Decision Tree: Which Path Fits Your Situation?

The right foreclosure options Georgia homeowner path starts with timing. A homeowner with 120 days has options. A homeowner with 12 days has fewer options, but still may be able to act.

Start with these questions:

- Have you received a Notice of Sale with an auction date? If yes, write down the auction date first.

- Can you pay the full reinstatement amount in cash within 14 days? If yes, request a written reinstatement quote.

- Is the home your primary residence, and could you afford a modified payment? If yes, request loss mitigation and contact a HUD-approved counselor.

- Do you owe less than the home’s market value? If yes and you have 60+ days, evaluate a fast MLS listing.

- Do you owe more than the home is worth? If yes and you have 90+ days, ask about a short sale.

- Is bankruptcy potentially relevant because you want to keep the home and restructure arrears? If yes, speak with a Georgia bankruptcy attorney before the auction date.

Want to know exactly what your Savannah home would net under each of the five paths? ARC’s free Home Value + Selling Plan runs the math for your address, your timeline, and your equity position, built around the foreclosure clock.

If You Have Less Than 30 Days (Read This First)

If your auction is less than 30 days away, your job is to confirm facts, get written numbers, and choose a path immediately. A signed listing agreement or buyer contract is not enough by itself. You need the foreclosure stopped, postponed, paid off, or legally stayed before sale.

- Today: call the servicer’s loss mitigation department. Request a written reinstatement quote, written payoff information if selling, and written foreclosure status confirmation. Ask whether the sale date is active.

- Today: call a Georgia foreclosure attorney. Ask whether any legal option, bankruptcy stay, servicer error, notice issue, or emergency filing could apply. The Georgia Attorney General states that a properly filed bankruptcy petition can suspend foreclosure proceedings if filed before the property is sold, although the lender may seek permission to resume foreclosure. (Office of the Attorney General)

- Day 1-3: get a written market valuation. You need to know whether the home has equity. ARC can provide a same-day valuation for pre foreclosure Savannah homeowners who are working against an auction date.

- Day 3-5: choose between fast listing and cash sale. If the property is marketable and buyer demand supports a quick contract, a fast MLS listing may work. If not, compare investor offers.

- Day 5-7: execute the chosen path. If listing, price to attract serious offers quickly. If cash, request multiple offers and compare net, inspection terms, closing date, proof of funds, and attorney coordination.

- Day 7-25: coordinate closing with the foreclosure deadline. Your closing attorney needs enough time to obtain payoff, clear title, record the deed, and confirm funds.

- Final week: confirm in writing. Confirm payoff, postponement, bankruptcy stay, or closing status in writing. Do not assume the auction is canceled because someone said it should be.

Talk to a Georgia foreclosure attorney or HUD-approved housing counselor about your specific situation.

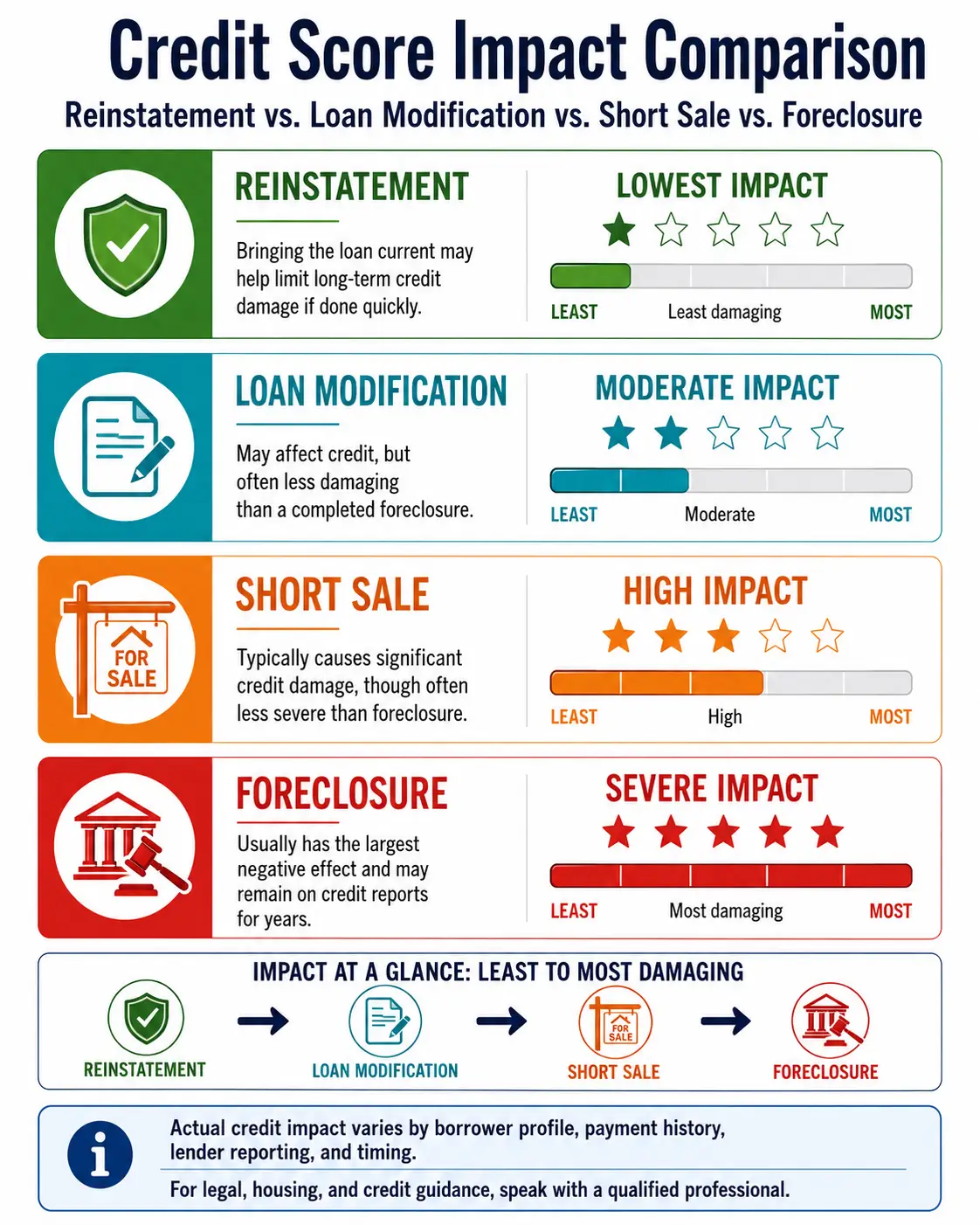

How Your Credit Is Affected by Each Path

Credit damage depends on your payment history, current score profile, how late the loan is, and whether a foreclosure sale is completed. The most reliable official baseline is timing: the CFPB says late payments and foreclosures generally remain on a credit report for seven years. (Consumer Financial Protection Bureau)

A sale before auction may still leave late payments on the credit report, but it avoids the completed foreclosure event. CFPB also notes that selling a home can make financial sense for some struggling homeowners with equity when home-retention options are unaffordable. (Consumer Financial Protection Bureau)

If your mortgage issue is connected to divorce, separation, or two-party ownership, read our guide for selling a house during divorce in Savannah before making a unilateral decision.

Free Resources Every Savannah Pre-Foreclosure Homeowner Should Use

Free help exists, and you should use it early. The right resource depends on whether your question is legal, loan-servicing, housing-counseling, or real-estate related.

Start with a HUD-approved housing counselor. HUD’s Georgia page directs homeowners to search for HUD-approved housing counselors or call (800) 569-4287, and HUD’s Georgia agency list includes Savannah-area providers such as CCCS of the Savannah Area. HUD Georgia housing resources (HUD)

Use the CFPB’s mortgage servicing resources if you are trying to understand your servicer’s obligations. CFPB says servicers must send a notice of delinquency after a borrower falls behind more than 45 days, and the notice must include information such as the amount needed to bring the loan current, foreclosure risks, and housing counseling information. CFPB mortgage servicing rules for homeowners (Consumer Financial Protection Bureau)

Use the Georgia Department of Banking and Finance if your issue involves a Georgia licensed or registered mortgage company. The department says consumers should first send a written complaint directly to the company by certified mail, and the department expects licensees under its supervision to make good faith attempts to resolve complaints within a reasonable period. Georgia Department of Banking and Finance mortgage complaint guidance (Department of Banking and Finance)

Use the Chatham County Clerk of Superior Court if you need to verify recorded real estate documents. For inherited property, estate ownership, or probate-related complications, read our guide to inherited homes in Savannah.

6 Common Mistakes That Cost Savannah Homeowners Their Equity

Ignoring servicer letters because they are stressful. Those letters often contain deadlines, document requests, sale dates, and loss mitigation instructions. Open every letter, scan it, and save it.

Listing with an agent who does not understand the foreclosure clock. A normal listing plan may be too slow. Pre foreclosure Savannah listings need a deadline-based pricing, showing, title, and closing strategy.

Accepting the first cash offer without comparing. Pre-foreclosure leads attract investors because time pressure creates discounts. If cash is the right path, compare multiple offers and focus on net proceeds, proof of funds, closing date, and inspection terms.

Submitting an incomplete loan modification package. CFPB’s Regulation X rules give stronger protections to complete loss mitigation applications. An incomplete file may not stop the sale. (Consumer Financial Protection Bureau)

Believing a signed contract automatically stops the auction. A contract is not the same as a closed sale. The servicer, attorney, and closing team must confirm payoff, postponement, or another valid stop mechanism.

Waiting too long to call a professional. At the first missed payment, you may have five options. In the last week before auction, you may have one or two.

Flood insurance, storm risk, and condition can also affect buyer confidence and closing speed in Coastal Georgia. Review the flood zones and insurance guide for Coastal Georgia if your home is in a flood-prone area or if buyer financing may require flood coverage.

When Bankruptcy Is Actually the Right Answer

Bankruptcy may be the right answer when you want to keep the home and have enough income to handle ongoing payments plus a court-approved repayment structure. It may also be relevant when foreclosure is only one part of a larger debt problem.

The Georgia Attorney General states that a valid bankruptcy filing acts as a stay of legal proceedings, including non-judicial foreclosure, if it is properly filed before the property is sold on the courthouse steps. The same page warns that the lender may ask the bankruptcy judge for permission to resume foreclosure and that filing has serious consequences. (Office of the Attorney General)

Chapter 13 may be worth discussing if you have income, want to keep the home, and need time to catch up arrears over a structured period. It may also help if credit cards, medical bills, tax issues, or business debt are part of the same financial problem.

Bankruptcy is not automatically the best answer just because the auction is close. If you have equity, a sale before foreclosure may protect more of your long-term financial position. Talk to both a Georgia bankruptcy attorney and a real estate professional before deciding.

Talk to a Georgia foreclosure attorney or HUD-approved housing counselor about your specific situation.

Frequently Asked Questions

How long does foreclosure take in Georgia?

Georgia foreclosure timing depends on your loan status, servicer actions, and the scheduled sale date. The CFPB says the legal foreclosure process generally cannot start until you are at least 120 days behind on the mortgage. After that, Georgia’s non-judicial process can move quickly because the Notice of Sale must be sent at least 30 days before the proposed sale, and auctions happen on the first Tuesday of the month. (Consumer Financial Protection Bureau)

Can I sell my house if I’m behind on mortgage payments?

Yes, you can often sell your house while behind on mortgage payments if you close before the foreclosure sale and the payoff is enough to satisfy the lender. If you have equity, a traditional or fast MLS listing may preserve more value than a cash sale. If the auction is close, your agent and closing attorney need to coordinate directly around payoff, title, and recording deadlines.

What is a Notice of Sale in Georgia?

A Notice of Sale is the written notice that the mortgage holder must send before the proposed foreclosure sale. Georgia’s Attorney General says the notice must be sent at least 30 days before the foreclosure sale and must include contact information for someone with authority to negotiate, amend, and modify the mortgage terms. It must also include a copy of the sale advertisement. (Office of the Attorney General)

Does Georgia have a right of redemption after foreclosure?

For a standard Georgia non-judicial mortgage foreclosure, do not plan on reclaiming the home after the auction. The Georgia Attorney General explains that the winning bidder becomes the new owner after the foreclosure sale and that a valid foreclosure wipes out the borrower’s right to live in the house. If you believe there are legal defects or special facts, talk to a Georgia foreclosure attorney immediately. (Office of the Attorney General)

How many missed mortgage payments before foreclosure in Georgia?

Many borrowers receive late notices after one missed payment, but federal servicing rules generally prevent the legal foreclosure process from starting until the borrower is more than 120 days delinquent. The exact timeline depends on the loan, servicer, prior loss mitigation history, and state foreclosure steps. Do not wait for the 120-day mark to act. Contact the servicer and a HUD-approved counselor as soon as you fall behind. (Consumer Financial Protection Bureau)

What is the difference between a short sale and a foreclosure?

A short sale is a lender-approved sale for less than the mortgage balance. The Georgia Attorney General says a short sale must be approved in advance by the lender. A foreclosure is the lender’s sale of the property after default under the power-of-sale process. A short sale happens before foreclosure and may give the homeowner more control over timing, buyer selection, and deficiency terms. (Office of the Attorney General)

Can I stop a foreclosure auction at the last minute?

Sometimes, but the options narrow sharply near the sale date. A last-minute stop may involve reinstatement, payoff through sale, written postponement from the servicer, complete loss mitigation protections if timing rules apply, or a valid bankruptcy stay. CFPB rules provide stronger protections for complete loss mitigation applications received more than 37 days before sale. If you are inside 30 days, call a foreclosure attorney immediately. (Consumer Financial Protection Bureau)

Will I owe money after a foreclosure in Georgia?

You might, depending on the foreclosure result and lender actions. The Georgia Attorney General explains that a mortgage holder may file suit to recover the difference between the foreclosure sale price and the remaining note balance, called a deficiency proceeding. If you are considering short sale, cash sale, deed in lieu, or bankruptcy, ask in writing how any remaining balance will be handled. (Office of the Attorney General)

Pre-foreclosure does not give you a perfect set of choices. It gives you a time-sensitive decision tree.

If you act early, you may be able to reinstate, modify, list, or short sale. If you wait until the final days before a Savannah foreclosure auction, cash sale or legal intervention may be the only realistic paths left.

Whichever path fits your situation, ARC can help you understand the home value, likely net, timeline, and next step without pressure or a listing obligation.

Join The Discussion